The Bull Case For General Electric (GE) Could Change Following Cautious Guidance Amid Strong Aerospace Results

GE Aerospace GE | 0.00 |

- Earlier in May 2026, GE Aerospace’s shareholders rejected a proposal for a report on defense-related products, while the company simultaneously reported strong earnings, rising orders, and cautious full-year guidance reflecting Middle East disruptions and softer aircraft departure growth expectations.

- Amid this mix of robust operational performance, expanding defense work such as the new GE426 engine program, and AI-driven R&D advances, investors are weighing how geopolitical risks and margin pressure could influence GE Aerospace’s future cash generation profile.

- We’ll now examine how GE Aerospace’s lowered aircraft departure growth outlook and cautious guidance may influence the existing investment narrative.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

General Electric Investment Narrative Recap

To own GE Aerospace today, you need to believe its large installed engine base and high-margin services can offset cycles in aircraft production and travel demand. The key near term catalyst is how quickly services revenue converts to cash, while the biggest risk is margin pressure from inflation and supply chain strain. The latest cautious guidance around Middle East disruptions and lower aircraft departure growth does not appear to fundamentally change that core thesis, but it has sharpened focus on execution.

The most relevant recent development here is GE Aerospace’s revised outlook alongside strong Q1 2026 results, where earnings and orders were solid but margins slipped and full year aircraft departure growth was trimmed. That mix of strength and caution connects directly to the main catalyst of services driven cash generation and the risk that higher costs or geopolitical shocks could compress profitability even as demand and the US$170 billion services backlog support long term activity.

Yet beneath the strong backlog and cash story, investors should be aware of how sustained supply chain and cost inflation could quietly reshape GE Aerospace’s margin profile and...

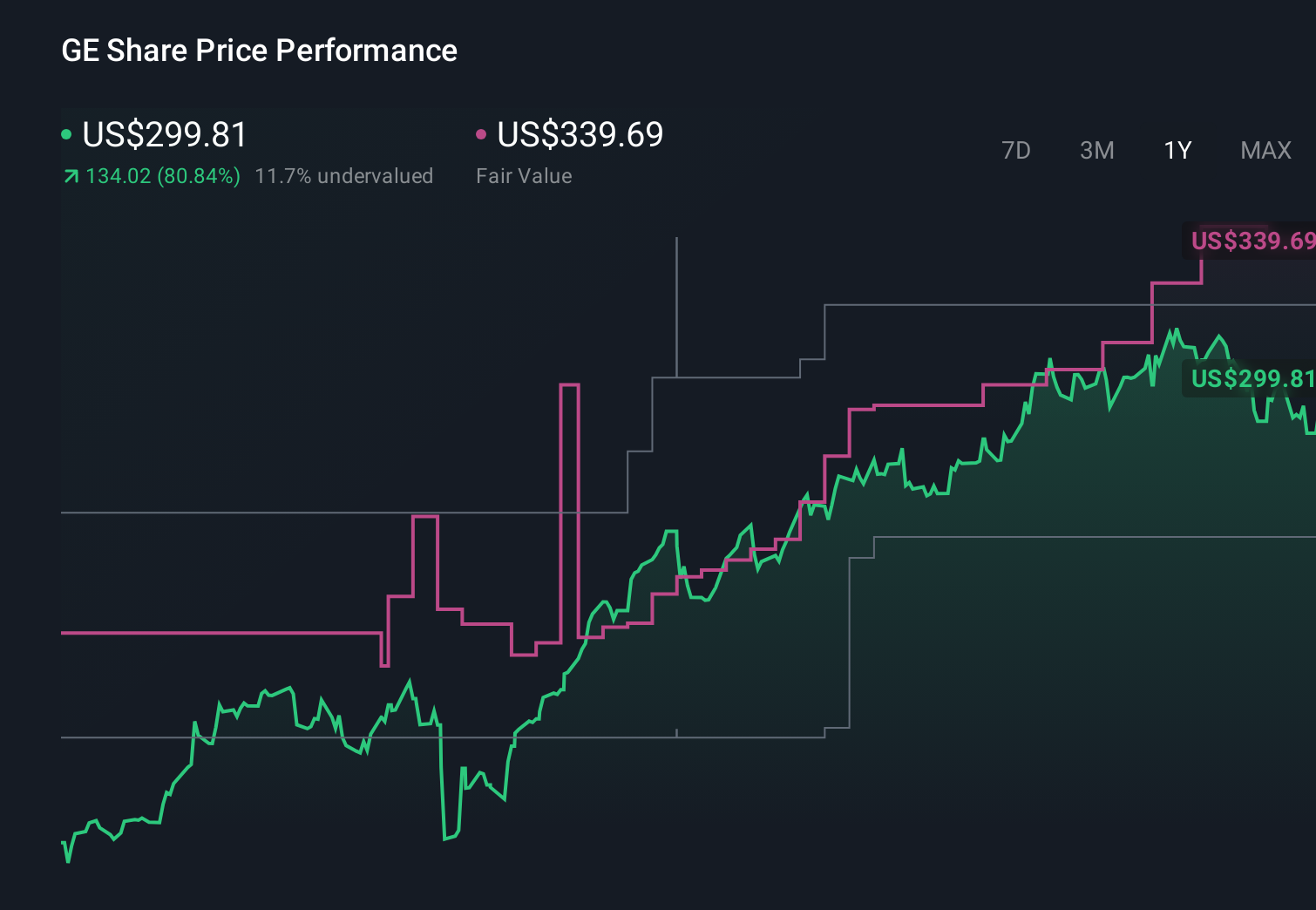

General Electric's narrative projects $59.2 billion revenue and $10.8 billion earnings by 2029.

Uncover how General Electric's forecasts yield a $350.45 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts saw GE reaching about US$62.1 billion in revenue and US$12.1 billion in earnings by 2029, which is far more upbeat than concerns about geopolitical strain and cost pressure implied by the latest guidance, reminding you that views on GE’s risk and reward can differ widely and may need to be revisited after this news.

Explore 10 other fair value estimates on General Electric - why the stock might be worth 13% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Electric research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 43 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.