The Bull Case For Moelis (MC) Could Change Following Surging EPS And Revenue Momentum – Learn Why

Moelis & Co. Class A MC | 0.00 |

- In recent months, Moelis & Co reported a sharp jump in earnings per share alongside strong revenue growth, highlighting improved operational efficiency and deal execution.

- An interesting angle for investors is how this earnings momentum, paired with analyst expectations for continued expansion, could reshape views on the firm’s long-term earnings quality.

- Building on this stronger earnings performance, we’ll now examine how it affects Moelis’ existing investment narrative around growth, margins, and expansion.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Moelis Investment Narrative Recap

To own Moelis, you need to believe it can convert its advisory franchise and Private Capital Advisory build out into reliable earnings, despite inherently cyclical deal volumes. The recent jump in EPS and revenue supports that thesis and strengthens the short term catalyst around capital returns, but it does not remove the key risk that a slower deal backdrop or rising compensation could quickly compress margins.

The new US$300,000,000 share repurchase authorization sits at the heart of this story. Combined with the earnings rebound, it amplifies the existing catalyst that disciplined capital returns and solid margins could support shareholder value, while also raising the bar for Moelis to keep earnings and cash generation healthy enough to sustain buybacks alongside its regular dividend.

Yet, against this improving backdrop, investors still need to be alert to how quickly transaction volumes and fee pressure could affect Moelis' ability to...

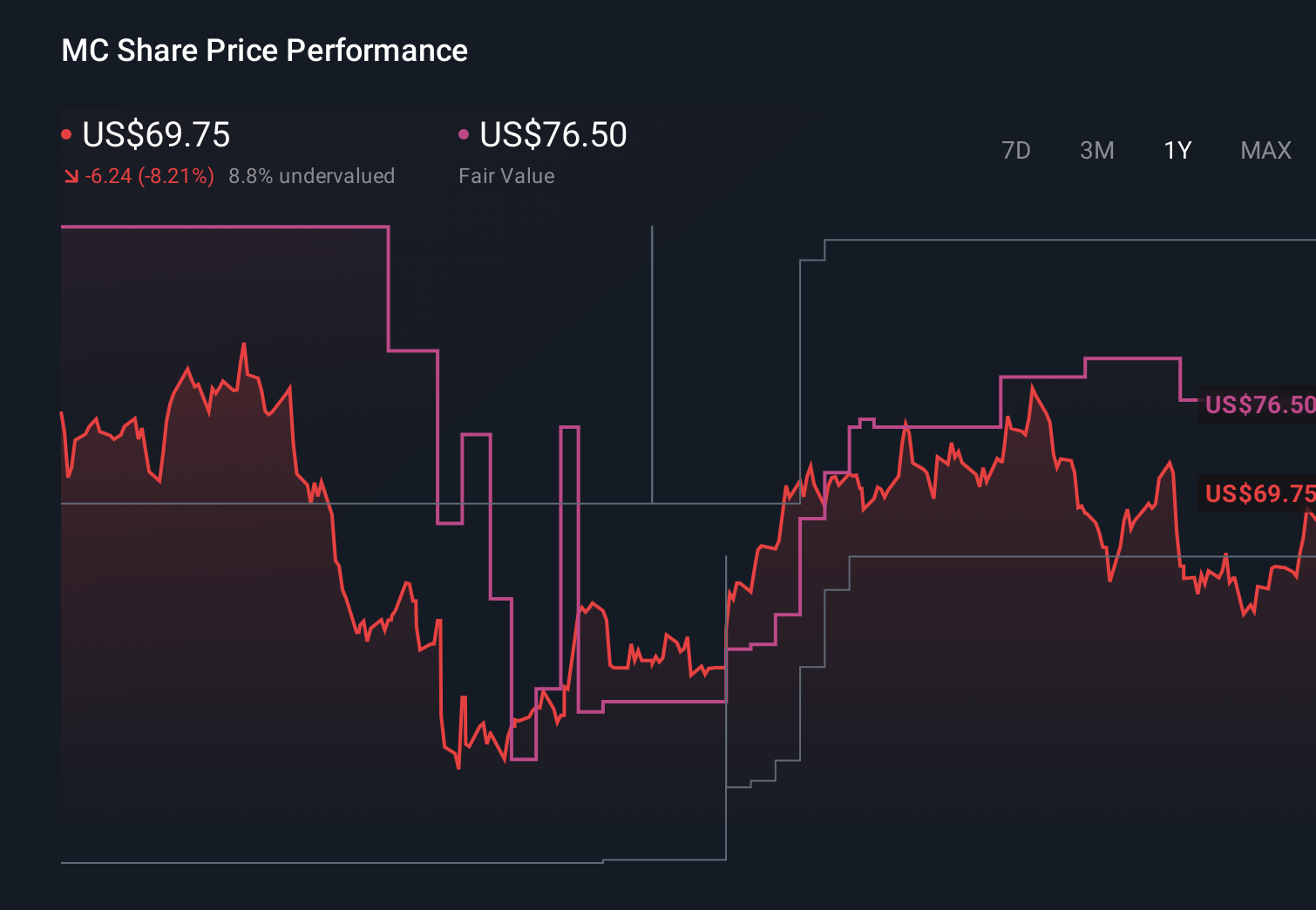

Moelis' narrative projects $2.1 billion revenue and $381.7 million earnings by 2028. This requires 15.3% yearly revenue growth and about a $183.6 million earnings increase from $198.1 million today.

Uncover how Moelis' forecasts yield a $76.50 fair value, a 36% upside to its current price.

Exploring Other Perspectives

You can see this in the lowest analyst estimates, which painted a far more cautious picture even before the latest earnings jump and technical base-building. They were working with assumptions like revenue of about US$2.3 billion and earnings of roughly US$502 million by 2029, paired with a much lower price to earnings multiple, which shows just how differently you might weigh Moelis' deal cyclicality and fee pressure risk compared with the more optimistic views.

Explore 2 other fair value estimates on Moelis - why the stock might be worth as much as 70% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Moelis research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 59 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.