The Bull Case For Philip Morris International (PM) Could Change Following 2026 EPS Cut And RBH Impairment

Philip Morris International Inc. PM | 0.00 |

- Earlier this week, Philip Morris International cut its 2026 full-year reported diluted EPS guidance to US$7.18–US$7.33, citing currency pressures and an expected US$500.00 million non-cash impairment related to Canadian affiliate Rothmans, Benson & Hedges.

- While this impairment weighs on reported earnings, management continues to highlight smoke-free products like IQOS and ZYN as the primary drivers of the company’s underlying performance.

- We’ll now examine how the RBH impairment and updated EPS guidance reshape Philip Morris International’s investment narrative around smoke-free growth.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to believe its shift toward smoke free products can more than offset structural cigarette declines and regulatory pressure. The RBH impairment and lower 2026 EPS guidance mostly highlight existing currency and regulatory risks, while the key near term catalyst remains execution in IQOS and ZYN. The biggest current risk is that smoke free growth could slow just as combustible volumes keep shrinking, leaving less room for earnings resilience.

The most relevant recent update is PMI’s confirmation that smoke free products, led by IQOS and ZYN, generated 43% of net revenues in Q1 2026. That mix shift sits at the heart of the “smoke free future” story and is central to management’s claim that underlying growth remains intact despite the non cash RBH impairment and currency headwinds. For investors, the question is how durable that momentum is if regulatory or competitive pressures intensify.

But even with this smoke free momentum, investors should be aware that rising illicit trade in key markets could still...

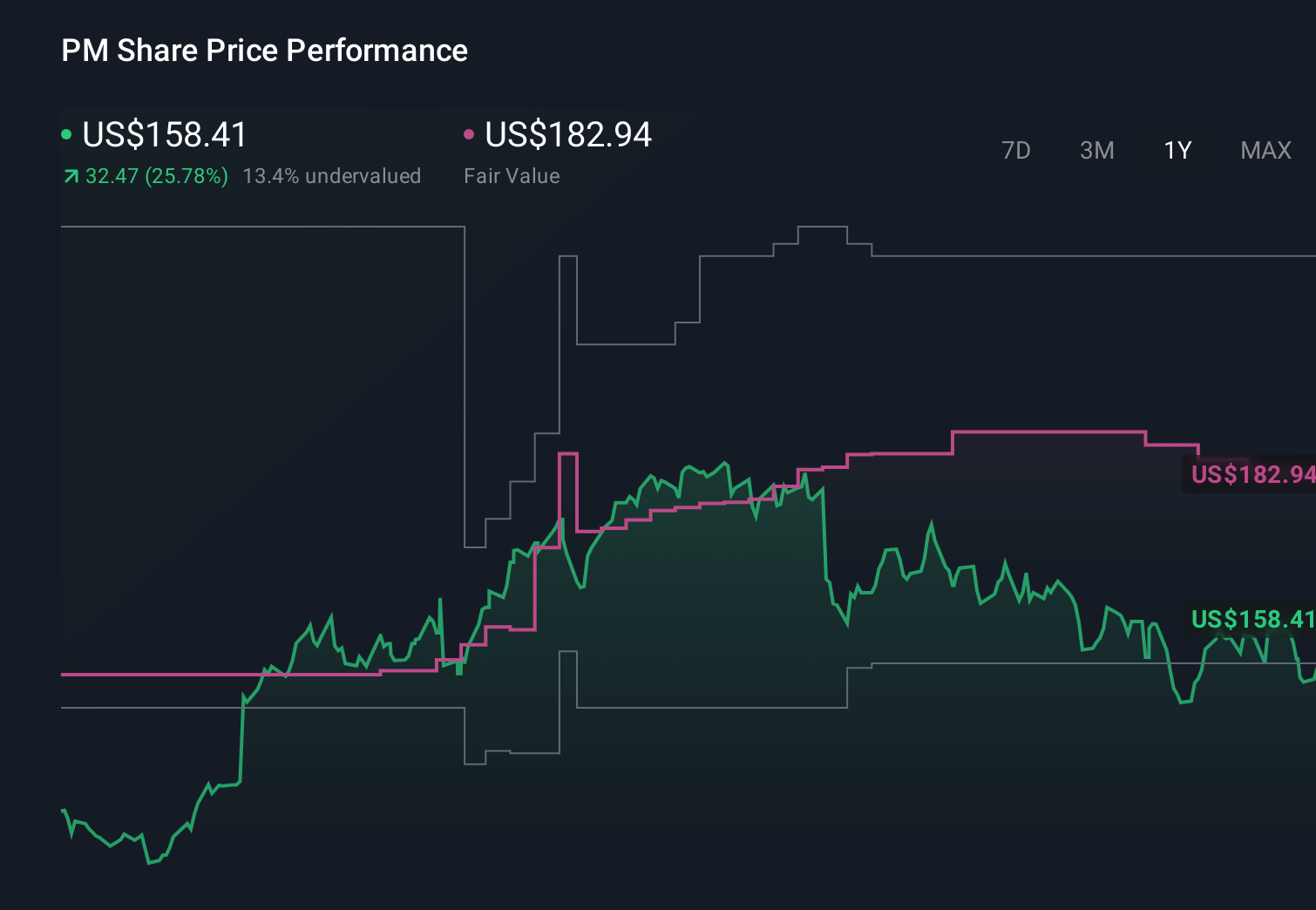

Philip Morris International's narrative projects $49.6 billion revenue and $15.3 billion earnings by 2029. This requires 6.1% yearly revenue growth and about a $4.2 billion earnings increase from $11.1 billion today.

Uncover how Philip Morris International's forecasts yield a $193.14 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the most optimistic analysts were assuming PMI could lift earnings to about US$15.7 billion by 2029, yet the RBH impairment and regulatory risks to smoke free growth highlight how quickly those expectations might be reconsidered, reminding you that reasonable people can read the same numbers and reach very different conclusions.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth as much as 18% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Philip Morris International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.