The Bull Case For Rush Enterprises (RUSH.A) Could Change Following Aftermarket-Driven Earnings Beat In Tough Truck Market

- Recently, Rush Enterprises reported quarterly results showing flat year-on-year revenue but a clear beat versus analysts’ expectations, including stronger-than-expected EBITDA, despite ongoing headwinds in the commercial vehicle industry such as soft freight demand, overcapacity, tariffs, and broader economic uncertainty.

- An interesting angle is that modest growth in higher-margin aftermarket activity and light-duty vehicle sales underpinned this earnings outperformance, highlighting the resilience of Rush’s parts and service operations even as core truck markets remain under pressure.

- We’ll now examine how this earnings beat, underpinned by aftermarket and light-duty strength, may reshape Rush Enterprises’ existing investment narrative.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Rush Enterprises Investment Narrative Recap

To own Rush Enterprises, you need to believe its mix of truck sales and higher-margin parts and service can support earnings through a tough commercial vehicle cycle. The latest earnings beat, driven by aftermarket and light-duty strength, slightly softens the near term risk that a prolonged freight slowdown could pressure both new vehicle demand and maintenance activity, but it does not remove that risk entirely.

Among recent announcements, the new US$150.0 million share repurchase program stands out as especially relevant, given the stock’s 17.1% move since the earnings release. This capital return plan now sits alongside the aftermarket driven earnings resilience as a key short term catalyst, particularly if investors continue to focus on how Rush balances cyclical truck exposure with more stable parts, service and buybacks.

Yet despite the resilience in parts and service, investors should still be aware of the risk that extended weak freight demand could...

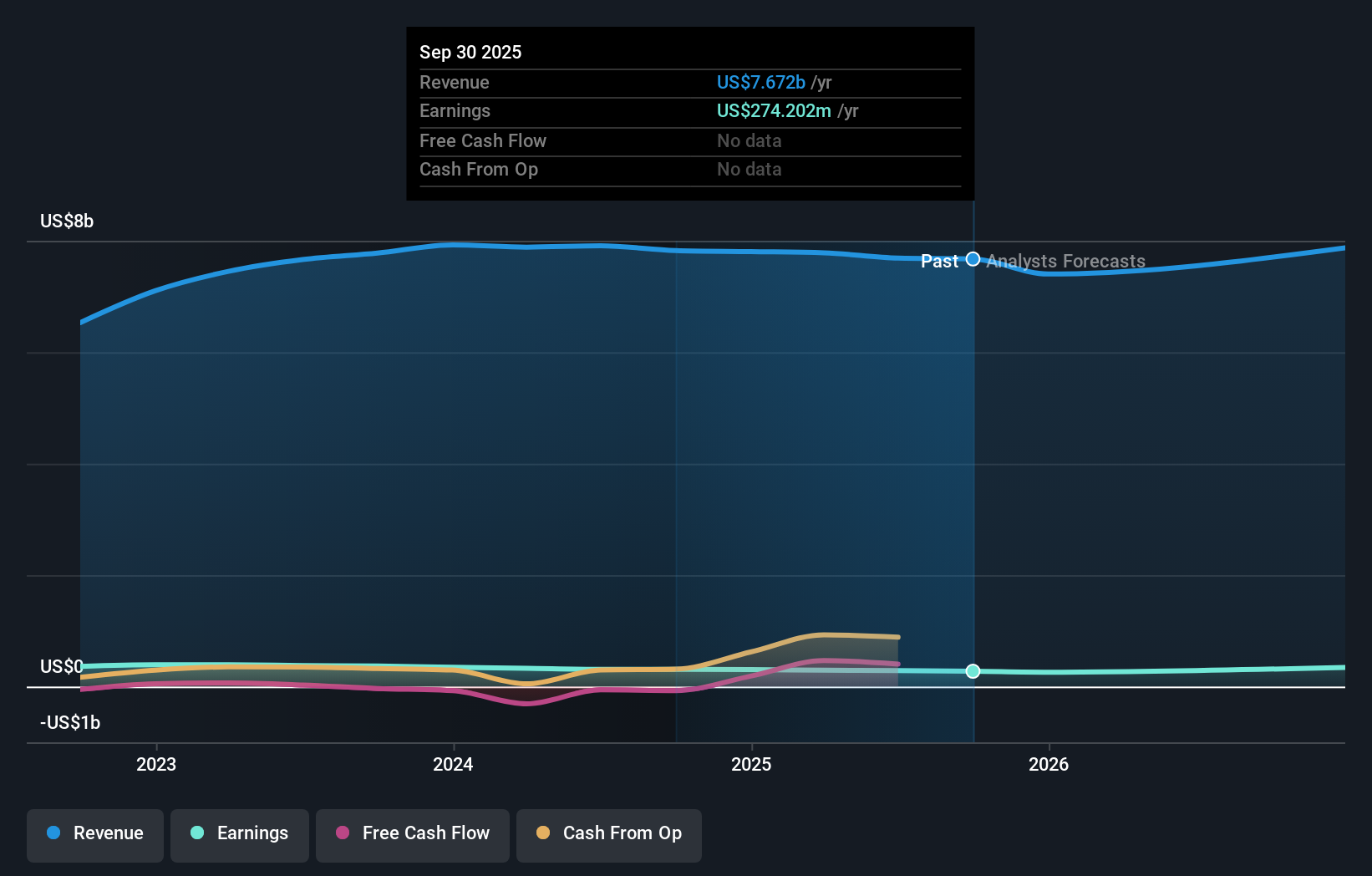

Rush Enterprises' narrative projects $7.6 billion revenue and $440.7 million earnings by 2028. This assumes revenue will decline by 0.3% per year and requires a $154.1 million earnings increase from $286.6 million today.

Uncover how Rush Enterprises' forecasts yield a $57.50 fair value, a 3% downside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s single fair value estimate of US$57.50 per share offers one clear reference point rather than a broad range of opinions. You should weigh that against the risk that persistent freight market weakness could still limit both new truck sales and aftermarket momentum, with important implications for how Rush’s recent earnings surprise might translate into longer term performance.

Explore another fair value estimate on Rush Enterprises - why the stock might be worth just $57.50!

Build Your Own Rush Enterprises Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Rush Enterprises research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Rush Enterprises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rush Enterprises' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are the new gold rush. Find out which 38 stocks are leading the charge.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.