The Bull Case For United Rentals (URI) Could Change Following 2026 Outlook And Expanded Buyback Plan

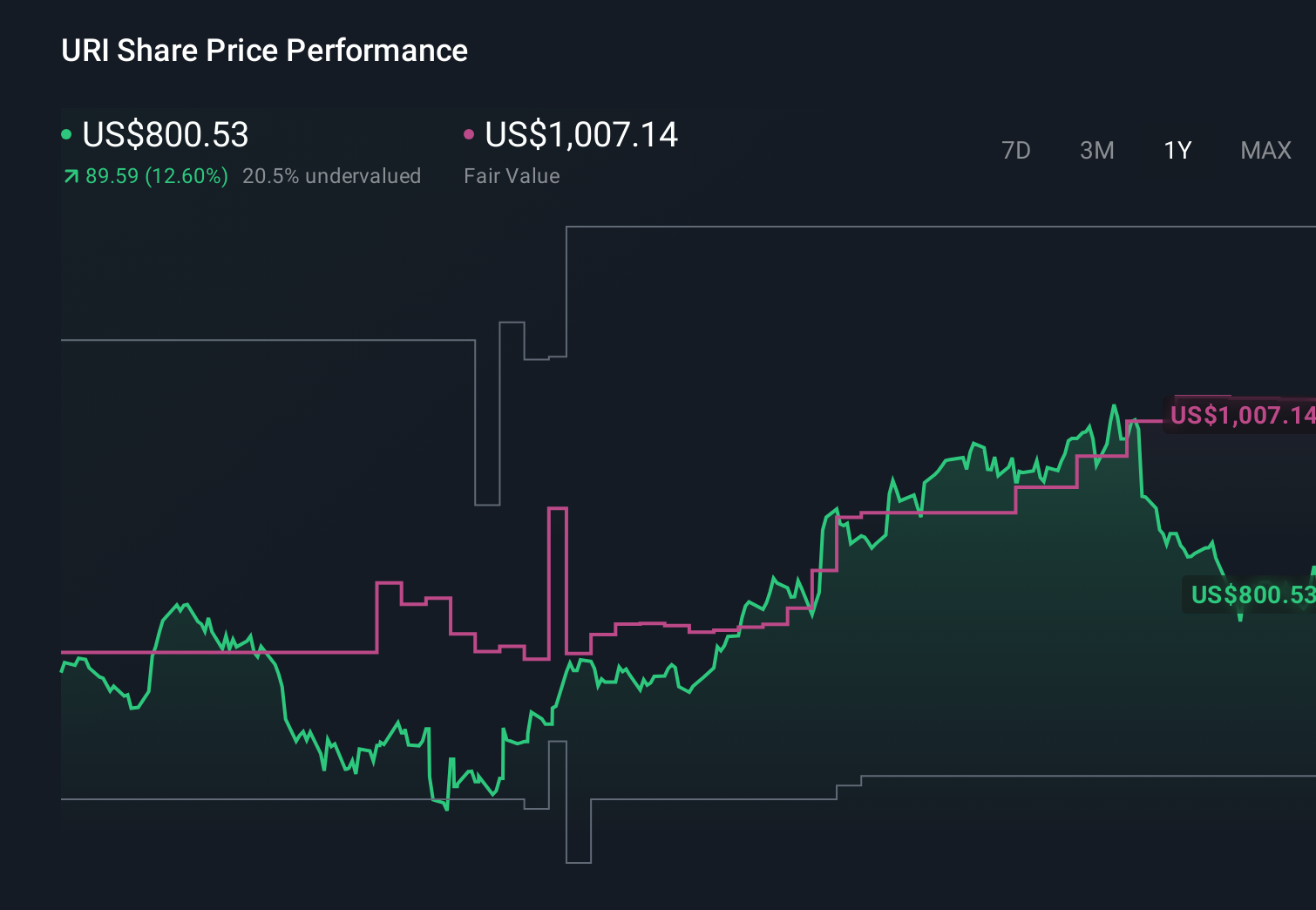

United Rentals, Inc. URI | 796.15 | +2.40% |

- United Rentals recently outlined its 2026 outlook, projecting 5.9% revenue growth and announcing a US$1.50 billion share repurchase plan alongside a 10% dividend increase, even after missing fourth-quarter 2025 earnings estimates due to higher operating and transportation costs.

- Together with new partnerships and board expansion, these capital return moves highlight management’s emphasis on reinforcing shareholder returns while contending with competitive pricing and utilization pressures in equipment rental markets.

- We’ll now explore how the expanded US$1.50 billion buyback program may reshape United Rentals’ investment narrative and risk‑reward profile.

Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

United Rentals Investment Narrative Recap

To own United Rentals, you need to believe that its scale, one stop offering and technology investments can offset cyclical swings in construction and rental demand. Right now, the key near term catalyst is execution against its 2026 revenue outlook, while the biggest risk is further margin pressure from higher operating and transportation costs. The latest guidance and capital return updates do not fundamentally change that balance, but they sharpen the focus on near term profitability.

The expanded US$1.50 billion buyback program sits at the center of this story, because it amplifies the impact of any earnings progress on per share results. Coming right after an earnings miss and renewed concerns about pricing and utilization, the program makes the timing and strength of rental demand, particularly in large projects and specialty, even more important to how the stock trades around upcoming results and guidance updates.

Yet investors should also be aware that if pricing pressure intensifies and utilization remains soft, especially while CapEx stays elevated, then...

United Rentals’ narrative projects $19.7 billion revenue and $3.4 billion earnings by 2029.

Uncover how United Rentals' forecasts yield a $985.89 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Lowest estimate analysts paint a tougher picture than consensus, assuming revenue grows to about US$17.6 billion and earnings to roughly US$2.9 billion by 2028, which contrasts sharply with concerns about rising regulatory and electrification costs that could further pressure margins.

Explore 4 other fair value estimates on United Rentals - why the stock might be worth as much as 39% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your United Rentals research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free United Rentals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Rentals' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.