TKO Stock And 2 Media Names Worth Watching After The ITV Sky Deal

TKO Group Holdings TKO | 0.00 |

The shock £1.6b takeover of ITV’s TV business by Sky, backed by Comcast, is reshaping UK broadcasting and putting fresh attention on large media stocks with meaningful exposure to traditional TV and streaming. With control of a broadcaster reaching 21 million households and a £2.1b content spend commitment to ITV Studios from 2028 to 2032, capital is moving and business models may need to adjust. This article looks at 3 stocks from our Media & Broadcasting Sector screener that are most exposed to this news, and how the deal could help or hurt their long term appeal.

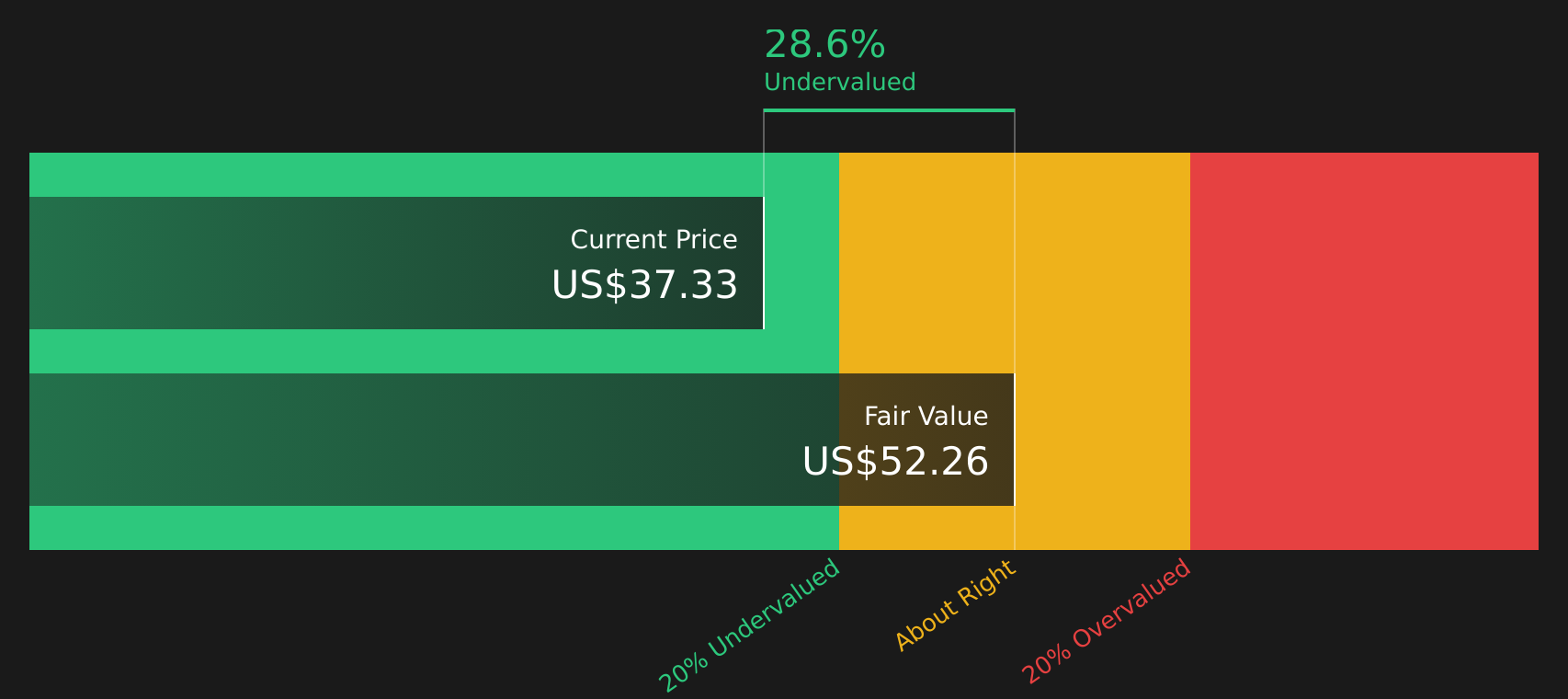

TKO Group Holdings (TKO)

Overview: TKO Group Holdings is a New York based sports and entertainment company that owns UFC, WWE and IMG, earning money from global media rights deals, live events, sponsorships and a wide range of licensed products from video games to apparel and memorabilia.

Operations: TKO generates most of its revenue from WWE at about US$1.8b, alongside UFC at about US$1.5b and IMG at about US$1.5b, with smaller contributions from corporate and other activities and eliminations between segments.

Market Cap: US$36.96b

Investors watching the ITV and Sky tie up may find TKO Group Holdings hard to ignore, because its UFC and WWE properties sit right in the sweet spot for broadcasters and streamers hungry for live, must watch content. TKO combines growth in earnings, improving margins and media rights visibility with regular sell out events, new partnerships in markets like Saudi Arabia and Azerbaijan, and a sizeable buyback and dividend program returning cash to shareholders. The flip side is a premium valuation, heavy reliance on debt funding and a relatively fresh board that still has to prove itself through a full cycle. If you want to understand how those trade offs stack up against the growth story in live sports media, you will need to look deeper into the details.

TKO’s live sports empire sits at the crossroads of premium content, leverage and a fresh leadership team, so the next move could be critical. Start with the 3 key rewards and 2 important warning signs and see what might be hiding in plain sight.

IMAX (IMAX)

Overview: IMAX is a cinema technology company that provides premium large format theater systems, remasters films for its screens, and licenses its brand and projection technology to exhibitors and content creators worldwide, including for streaming and live events.

Operations: IMAX generates most of its revenue from Technology Products and Services at about US$249.0m and Content Solutions at about US$148.4m, with only a small US$7.5m contribution from other activities.

Market Cap: US$2.19b

IMAX gives investors direct exposure to premium theatrical releases at a time when media groups are racing to differentiate content experiences, which fits neatly with the Sky and ITV focus on higher value formats. The company is seeing earnings forecasts that outpace the broader US market, a growing footprint of IMAX with Laser locations, and index inclusion that could support trading liquidity, while its shares are priced below some estimates of fair value. On the other hand, IMAX still leans heavily on blockbuster pipelines, carries a high P/E and has all its funding from external sources, which can amplify volatility. The real question is how those trade offs look once you factor in future system installs, live events and any potential corporate interest.

IMAX's premium footprint, blockbuster exposure and external funding mix could be masking a bigger story about earnings power and volatility. See how the analysis report for IMAX reshapes the risk reward picture.

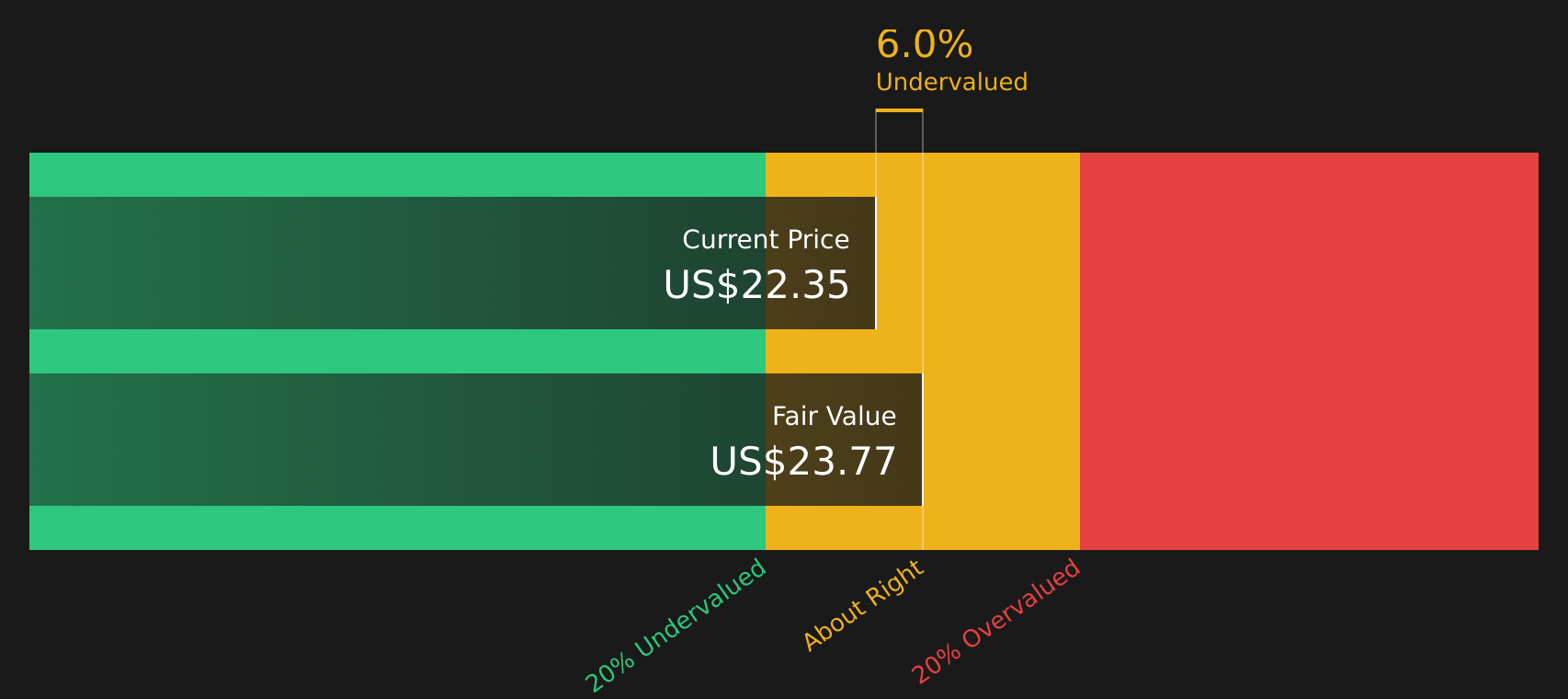

Marcus (MCS)

Overview: Marcus Corporation is a US based owner and operator of movie theatres, hotels and resorts, combining cinema brands like Marcus Theatres and Movie Tavern with a portfolio of full service lodging and hospitality management services.

Operations: Marcus generates about US$465.4m in revenue from Theatres, US$257.0m from Hotels and Resorts, and a small US$0.4m from Corporate Items, all within the United States.

Market Cap: US$712.9m

Marcus sits at the crossroads of cinema and hospitality at a time when attention is firmly back on premium media distribution after the Sky and ITV deal, providing exposure to both content exhibition and travel related demand in one stock. The company has only recently returned to profitability. It trades just below some estimates of fair value, and the P/E of 50.4x indicates that investors are already paying a relatively high price for its potential. There has also been heavy insider selling, all funding is coming from external sources, and the company has a low 3.2% ROE. This combination of factors presents both opportunity and risk, and may warrant closer inspection of whether the earnings trajectory and buyback activity justify the current price.

Marcus looks like a recovery story with a P/E of 50.4x and fresh profitability that many investors may be misreading. The real twist sits inside the analyst forecasts for Marcus and what that implies for the buyback, insider selling, and where expectations could be wrong.

The stocks covered here are just a starting point, and the full Media & Broadcasting Sector screener surfaces 5 more media companies with equally compelling narratives around scale, content exposure and evolving distribution models. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you so you can filter for the highest conviction opportunities in this sector.

Take Control of Your Investment Journey

If TKO Group Holdings or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh ideas can move quickly, and once momentum builds the best entry points can be hard to find. Scan these under the radar lists before the crowd arrives and act based on your own research and judgment.

- Review a curated 73 resilient stocks with low risk scores tailored to investors who care about staying power and capital protection to spot resilient businesses that may hold up when others are dropping.

- Use the hand picked 44 high quality undervalued stocks that focuses on quality businesses where expectations may not yet be fully priced in to find companies with strong cash generation and balance sheets.

- Check a focused 35 power grid technology and infrastructure stocks built to surface potential beneficiaries of grid upgrades while they are still under the radar to follow structural shifts in power and infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.