Tripadvisor (TRIP) Stock Valuation Gap Explored After Recent Rebound

TripAdvisor, Inc. TRIP | 0.00 |

Tripadvisor’s recent share move in focus

Tripadvisor (TRIP) has drawn attention after a recent rebound in the stock, with a gain over the past month and past 3 months standing against weaker longer term returns and a modest market value.

For readers tracking travel and online platform stocks, Tripadvisor now sits around a share price of $12.41 and a market cap of about $1.4b, with revenue of $1,875.2m and net income of $18.6m.

The recent 31.2% 1 month share price return and 30.4% 3 month share price return suggest short term momentum is improving, although the 1 year total shareholder return declined 6.7% and 5 year total shareholder return declined 69.6%.

If this rebound has you reassessing your watchlist, it could be worth widening your search to other consumer facing platforms and travel peers via the 20 top founder-led companies

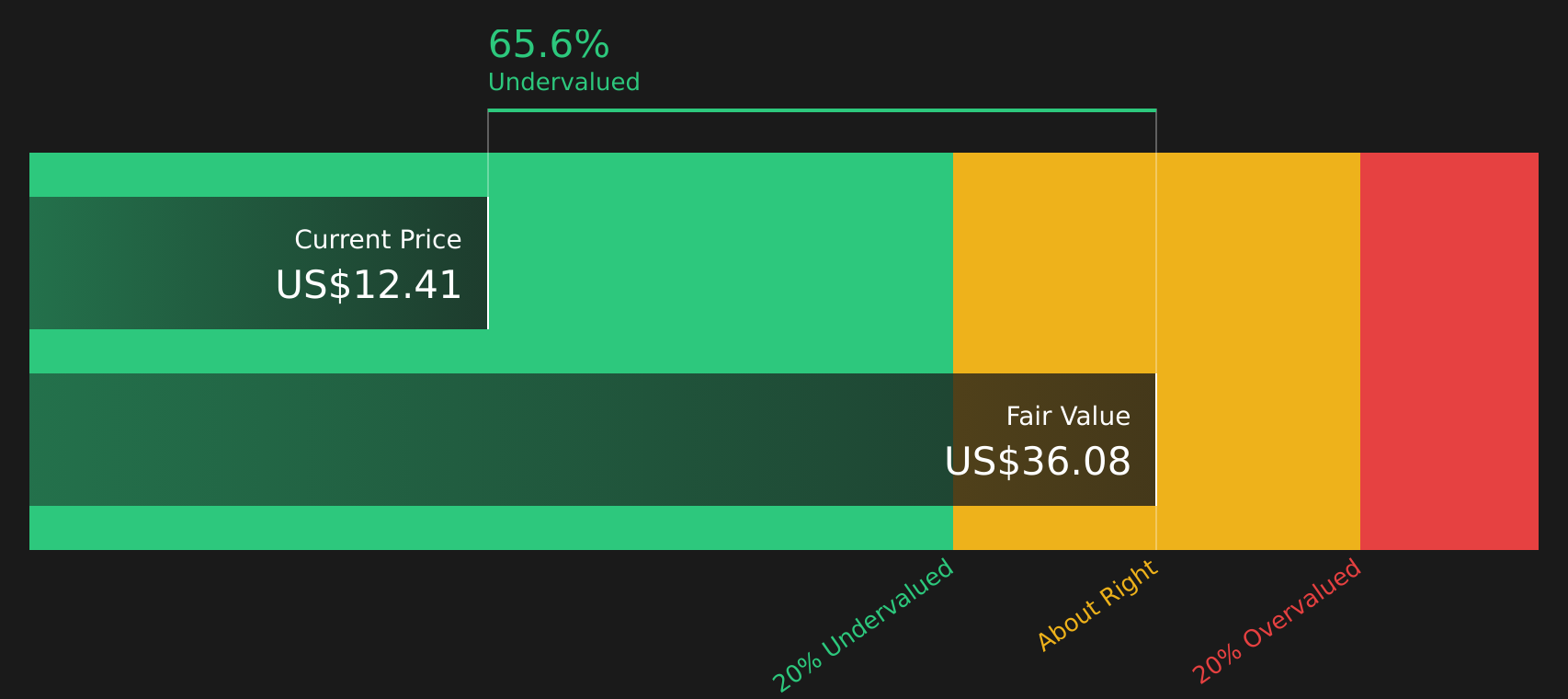

With Tripadvisor trading at $12.41, an intrinsic discount estimate of 65.6% and a modest 10.6% gap to analyst targets, the key question is whether the stock is genuinely undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 14% Undervalued

Compared to the last close at $12.41, the most widely followed narrative puts Tripadvisor’s fair value closer to $14.38, using a 10.84% discount rate to weigh future cash flows.

Diversification of revenue streams, especially with TheFork's growing B2B SaaS and subscription adoption, plus exclusive partnerships (like Mastercard), is increasing revenue resilience, expanding recurring/contractual revenue, and could drive higher and more predictable cash flows.

Tripadvisor's strong global brand, proprietary data, and trusted content position it well as online travel discovery increasingly shifts to verified, peer-driven platforms, placing the company at the forefront of long-term digital planning and booking trends, thus supporting both sustained traffic growth and higher monetization potential over time.

Curious what sits behind that fair value gap? The narrative leans heavily on faster earnings growth, thicker profit margins and a richer future earnings multiple than today suggests.

Result: Fair Value of $14.38 (UNDERVALUED)

However, this depends on Tripadvisor stabilising pressure in its legacy Hotels and Other segment and avoiding further erosion from competitors and direct supplier bookings.

Another way to look at Tripadvisor’s valuation

The SWS DCF model presents a very different perspective compared with the $14.38 fair value narrative, putting Tripadvisor’s future cash flow value closer to $36.08 per share. This is well above the current $12.41 price and is flagged as undervalued. The question for you is which set of assumptions feels more realistic.

Next Steps

With sentiment split between Tripadvisor’s risks and rewards, it makes sense to look at the charts, forecasts and fundamentals yourself and decide quickly where you stand with the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Tripadvisor has sharpened your focus, do not stop here. Broaden your watchlist with other potential opportunities before the next move catches you off guard.

- Scan for quality at a discount by checking companies highlighted in the 44 high quality undervalued stocks.

- Strengthen your portfolio’s foundations with businesses featured in the solid balance sheet and fundamentals stocks screener (48 results).

- Get ahead of the crowd by reviewing the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.