Ultra Clean Holdings (UCTT) Stock Could Be 18% Overvalued After Its Sharp Rally

Ultra Clean Holdings, Inc. UCTT | 0.00 |

Ultra Clean Holdings (UCTT) has attracted fresh attention after a strong month, with the stock up 46.6% over that period and 88.7% in the past 3 months. This performance has sharpened focus on its fundamentals.

At a share price of $123.14, Ultra Clean Holdings has seen strong momentum build, with a 30 day share price return of 46.6% and an 88.7% gain over 90 days. The 1 year total shareholder return is very large relative to these shorter timeframes.

If you are tracking this kind of momentum in semiconductor related stocks, it can be useful to see what else is moving by scanning 49 AI infrastructure stocks

The surge in Ultra Clean Holdings has arrived alongside revenue growth, strong net income growth, and a recent loss of $194.1 million. This raises a key question for investors: is there still a buying opportunity here, or is the market already pricing in potential future growth?

Most Popular Narrative: 18% Overvalued

Ultra Clean Holdings last closed at $123.14, while the most followed narrative anchors fair value at $104.40, creating a clear gap that hinges on future execution.

A surge in AI-driven capital investment and strong expectations for new fab buildouts in 2026 support solid long-term demand for Ultra Clean's advanced process subsystems, reinforcing the company's exposure to the ongoing expansion of digital infrastructure and complex chip manufacturing (supports long-term revenue trajectory).

Ongoing organizational flattening, cost reduction initiatives, and factory/site consolidation are producing tangible decreases in OpEx, with further improvements expected by Q4, providing sustainable margin enhancement as industry volumes recover (impacts net margins and overall profitability).

Curious how Ultra Clean Holdings gets to that fair value with a higher discount rate, rising revenue assumptions, and a reset profit margin profile? The narrative leans heavily on a multi year earnings ramp, a different future P/E than today, and a specific path to stronger returns on equity, but the full set of assumptions sits beneath the surface.

Result: Fair Value of $104.40 (OVERVALUED)

However, Ultra Clean Holdings still faces meaningful risks, including heavy reliance on a few large customers and ongoing tariff related costs that could pressure revenue stability and margins.

Another View On Ultra Clean Holdings Using Sales Multiples

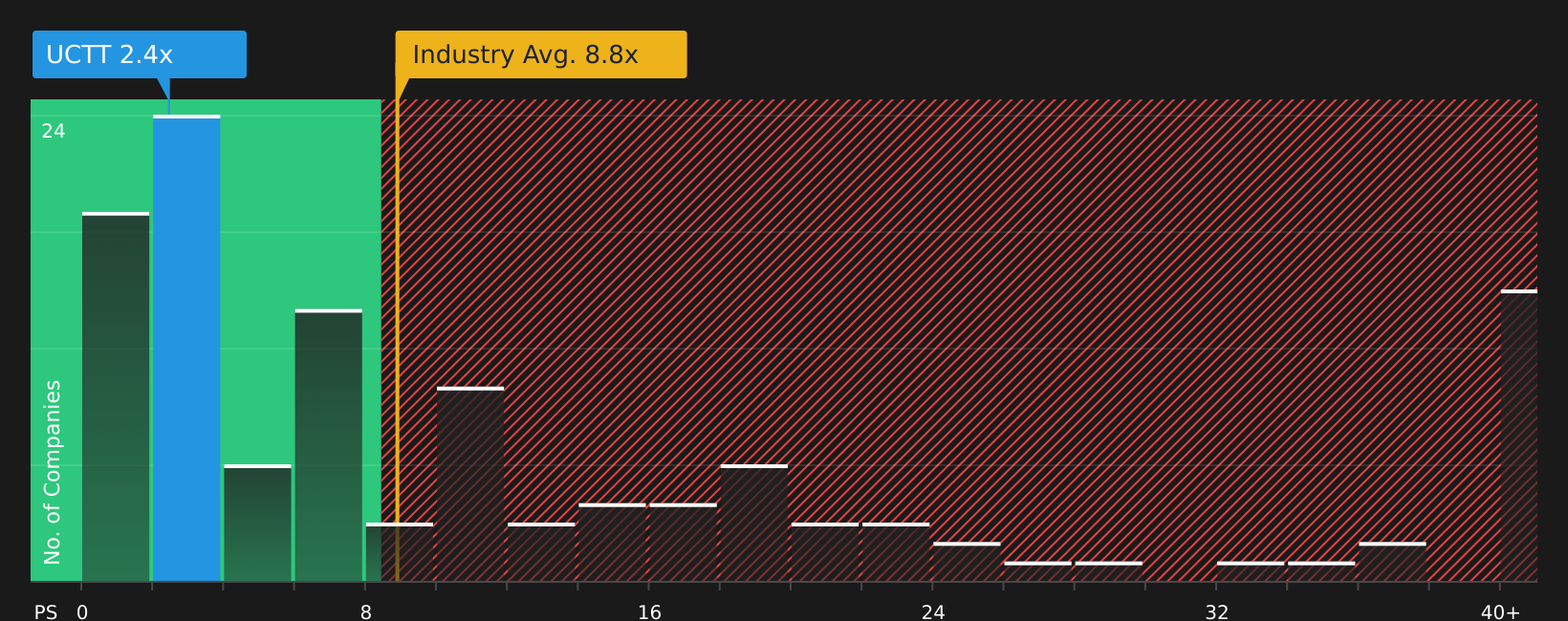

The fair value narrative for Ultra Clean Holdings rests on discounted future earnings, but the market is also sending a different signal through the current P/S ratio of 2.7x. That level is far below both peers at 21x and the broader US semiconductor industry at 9.3x, and even below the 3.7x fair ratio estimate.

In practice, that gap means investors are paying less per dollar of Ultra Clean Holdings revenue than for many peers, despite the recent share price run. This lowers the margin for disappointment on near term numbers, but also raises the question of whether the valuation is already conservative if revenue forecasts prove accurate.

Next Steps

With Ultra Clean Holdings showing both strong momentum and mixed signals, it makes sense to move quickly and check the data behind the headlines yourself. To weigh the upside against the concerns and form your own view, start by reviewing the 2 key rewards and 2 important warning signs

Looking For More Investment Ideas Beyond Ultra Clean Holdings?

If Ultra Clean Holdings has sharpened your interest in new opportunities, do not stop here. Use focused stock lists to spot other ideas before the crowd does.

- Target quality at a discount by reviewing companies identified in the 44 high quality undervalued stocks that combine solid fundamentals with appealing prices.

- Strengthen your income stream by scanning the 7 dividend fortresses that highlight companies offering higher yielding payouts.

- Dial down risk by checking the 66 resilient stocks with low risk scores focused on companies with more resilient financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.