Undervalued Small Caps With Insider Action To Consider In June 2026

Midland States Bancorp, Inc. MSBI | 0.00 |

Over the last 7 days, the United States market has experienced a 4.1% drop, yet it remains up by 21% over the past year with earnings forecasted to grow by 18% annually. In such dynamic conditions, identifying small-cap stocks that are perceived as undervalued and have notable insider activity can offer intriguing opportunities for investors seeking potential growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.2x | 0.8x | 42.88% | ★★★★★★ |

| Financial Institutions | 9.6x | 3.1x | 27.18% | ★★★★★☆ |

| Union Bankshares | 9.3x | 1.9x | 21.14% | ★★★★☆☆ |

| Angel Oak Mortgage REIT | 13.2x | 5.9x | 24.97% | ★★★★☆☆ |

| Similarweb | NA | 1.3x | 33.42% | ★★★★☆☆ |

| Alkami Technology | NA | 3.4x | 49.36% | ★★★★☆☆ |

| German American Bancorp | 12.7x | 4.6x | 41.82% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.8x | 33.58% | ★★★☆☆☆ |

| Shore Bancshares | 11.8x | 3.3x | 48.22% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.0x | 2.3x | 19.97% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

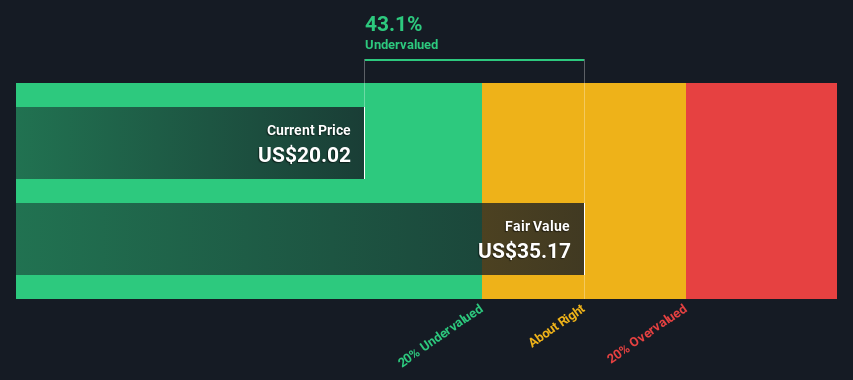

Midland States Bancorp (MSBI)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Midland States Bancorp is a financial holding company primarily engaged in banking and wealth management services, with a market cap of approximately $0.47 billion.

Operations: The primary revenue stream is from the Banking segment, contributing $254.68 million, while Wealth Management adds $31.84 million. The Corporate segment shows a negative contribution of -$12.05 million to overall revenue. Operating expenses are a significant cost factor, with General & Administrative Expenses being the largest component at $160.37 million in the latest period available. Over recent periods, net income margin has varied significantly, showing both positive and negative figures across different quarters.

PE: 24.0x

Midland States Bancorp presents an intriguing opportunity in the small-cap sector, highlighted by insider confidence through Travis Franklin's purchase of 9,400 shares for US$248,988. Recent executive changes with Claire A. Stack becoming CFO add depth to its leadership. The company's Q1 2026 net income of US$18.46 million marks a significant turnaround from last year's loss, complemented by strategic share repurchases totaling 822,729 shares for US$17.43 million. With earnings projected to grow annually by 42%, prospects appear promising amidst ongoing financial improvements and dividend payouts.

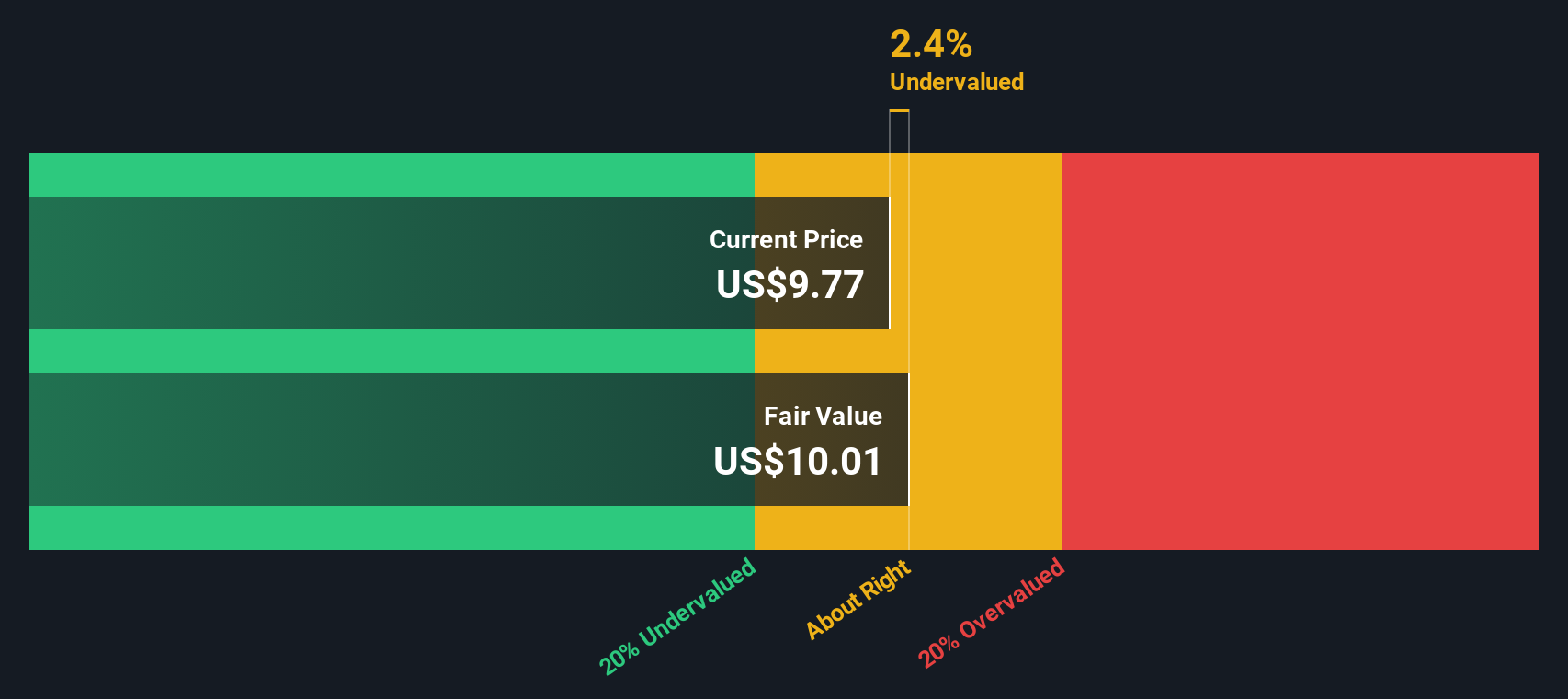

Pebblebrook Hotel Trust (PEB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Pebblebrook Hotel Trust is a real estate investment trust focusing on investments in hotel and motel properties, with a market capitalization of approximately $2.16 billion.

Operations: The company generates revenue primarily from its hotels and motels segment, which recently reached $1.50 billion. Cost of goods sold (COGS) is a significant expense, amounting to approximately $1.12 billion in the latest period. The gross profit margin has shown variability, with a recent figure of 25.16%. Operating expenses and non-operating expenses also contribute notably to the financial structure, affecting net income outcomes over time.

PE: -21.3x

Pebblebrook Hotel Trust, a smaller player in the hospitality sector, has recently shown insider confidence with share purchases. Despite facing challenges like revised earnings guidance for 2026 and a net loss of US$19.27 million in Q1 2026, the company reported increased revenue of US$345.66 million compared to last year. Recent amendments to bylaws enhance shareholder rights, potentially boosting investor sentiment. While profitability remains elusive, strategic buybacks totaling 405,821 shares reflect management's commitment to enhancing shareholder value amidst ongoing industry recovery efforts.

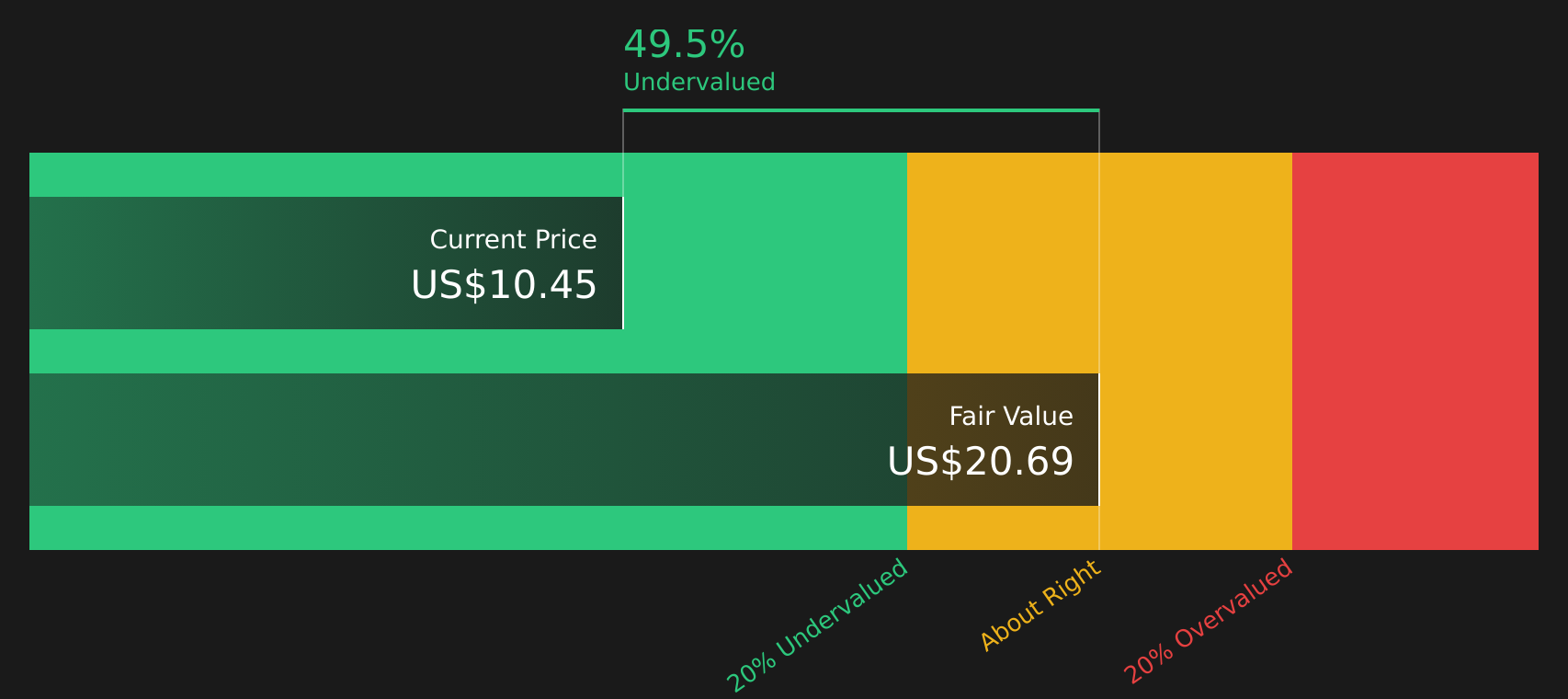

TETRA Technologies (TTI)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: TETRA Technologies operates in the energy sector, focusing on water and flowback services as well as completion fluids and products, with a market cap of $0.53 billion.

Operations: The company generates revenue primarily from two segments: Water & Flowback Services and Completion Fluids & Products. Analyzing recent financial data, the gross profit margin showed an upward trend, reaching 31.23% in the quarter ending June 2025. Operating expenses are a significant cost component, with General & Administrative Expenses consistently forming a substantial part of these costs.

PE: 165.6x

TETRA Technologies, a smaller player in the U.S. market, is capturing attention with its strategic initiatives and insider confidence. Recently, insiders have shown faith by purchasing shares over the past few months. The company is advancing its Evergreen Project to become a vertically integrated bromine producer, aiming for production start-up by early 2028. Despite recent profit margin challenges—down to 1.3% from last year's 19.3%—earnings are projected to grow significantly at 55.66% annually, suggesting potential value for investors seeking growth opportunities amidst financial restructuring efforts like their recent US$100 million equity offering completed on June 2nd, 2026.

Make It Happen

- Click through to start exploring the rest of the 71 Undervalued US Small Caps With Insider Buying now.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.