Undervalued Small Caps With Insider Actions To Watch In June 2026

Kingstone Companies Incorporated KINS | 0.00 |

Over the last 7 days, the United States market has remained flat, although it has seen a significant rise of 20% over the past year, with earnings expected to grow by 19% annually in the coming years. In this environment, identifying small-cap stocks that are potentially undervalued and have notable insider actions can offer intriguing opportunities for investors seeking to capitalize on future growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.1x | 0.8x | 43.64% | ★★★★★★ |

| Similarweb | NA | 1.9x | 20.37% | ★★★★★☆ |

| AVITA Medical | NA | 1.8x | 46.45% | ★★★★★☆ |

| Shore Bancshares | 12.3x | 3.4x | 46.14% | ★★★★☆☆ |

| Peoples Bancorp | 12.3x | 3.2x | 41.09% | ★★★★☆☆ |

| Bank of the James Financial Group | 10.2x | 2.2x | 19.78% | ★★★☆☆☆ |

| Patria Investments | 24.0x | 4.3x | 11.54% | ★★★☆☆☆ |

| Union Bankshares | 9.6x | 2.0x | 19.00% | ★★★☆☆☆ |

| NameSilo Technologies | 412.2x | 1.9x | 42.77% | ★★★☆☆☆ |

| Onterris | 166.7x | 0.9x | 16.33% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

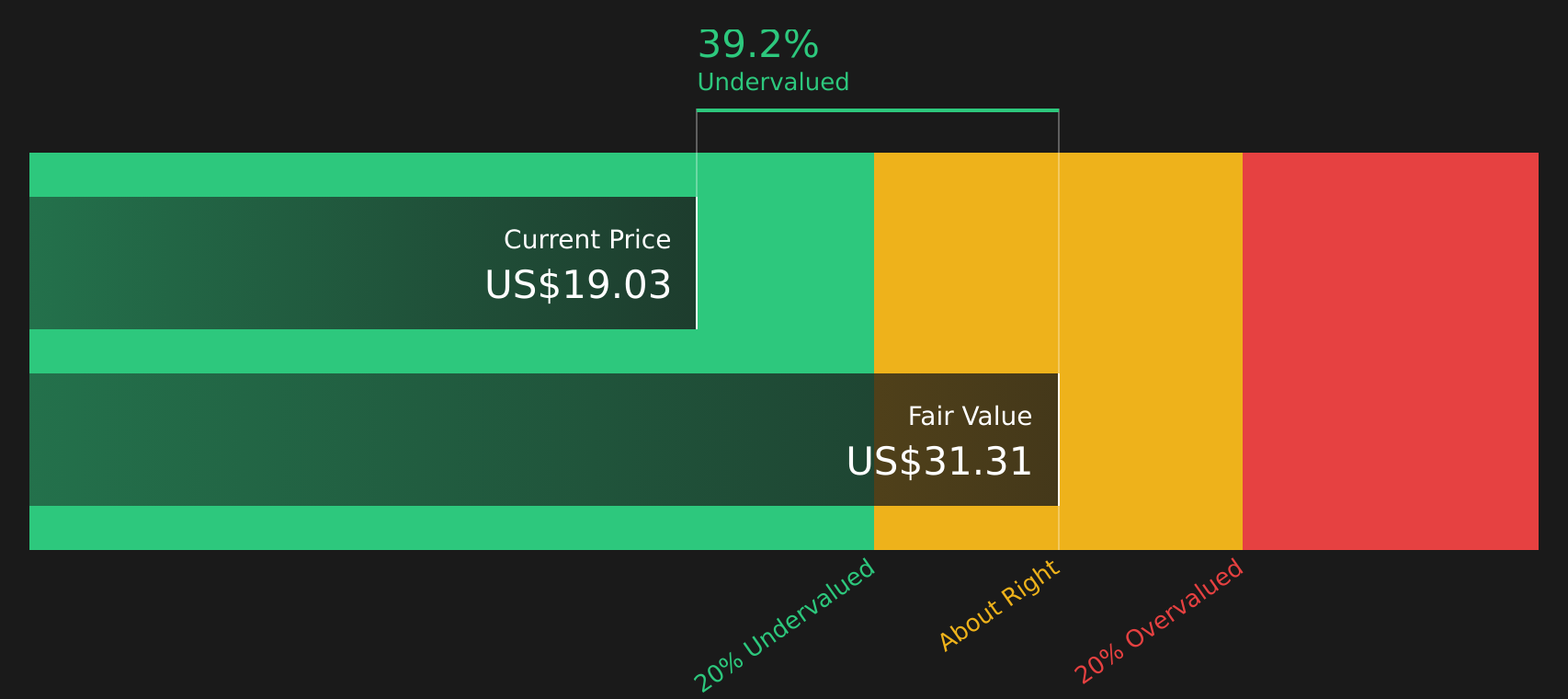

Kingstone Companies (KINS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Kingstone Companies operates in the property and casualty insurance sector with a focus on providing personal and commercial lines of coverage, and it has a market capitalization of $8.46 million.

Operations: The company primarily generates revenue from its property and casualty insurance segment, with the latest reported revenue at $224.14 million. Over recent periods, the gross profit margin has shown variability, reaching 26.41% in late 2025 before adjusting to 21.08% by mid-2026. Operating expenses are a significant component of costs, consistently impacting net income outcomes across various quarters.

PE: 9.0x

Kingstone Companies, a smaller player in the insurance sector, recently experienced a significant shift in its index affiliations. On June 27, 2026, it was dropped from several growth benchmarks but added to the Russell 2000 Value-Defensive Index. This move aligns with insider confidence shown by Gregory Fortunoff's purchase of over 53,000 shares valued at approximately US$843K. Despite reporting a net loss of US$5.81 million for Q1 2026 and relying on higher-risk external funding sources, Kingstone anticipates earnings growth of over 20% annually and has initiated a share repurchase program targeting up to one million shares within two years.

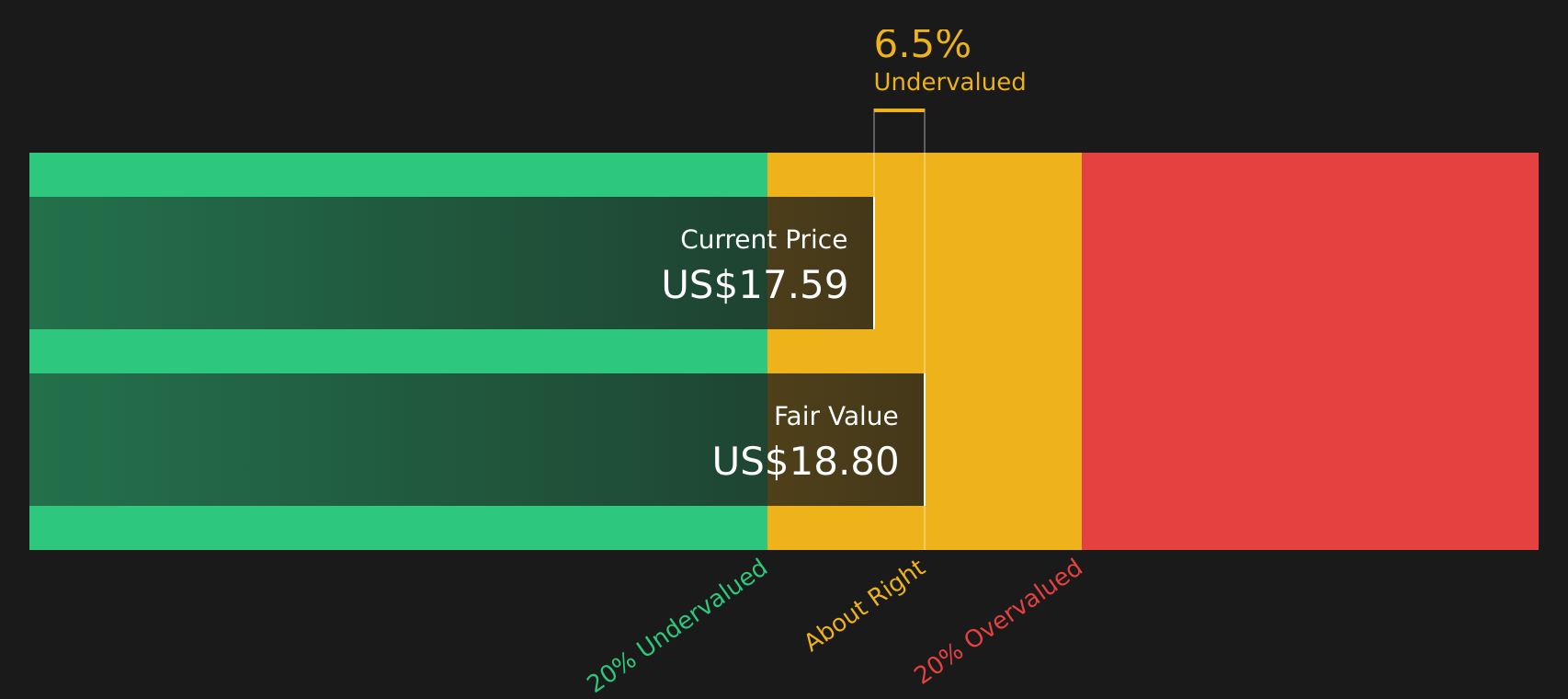

LCNB (LCNB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: LCNB is a financial institution primarily engaged in banking operations with a market cap of approximately $0.17 billion.

Operations: LCNB generates revenue primarily through its banking operations, with a recent quarterly revenue of $89.94 million. The company has consistently achieved a gross profit margin of 100% over several periods, indicating that it incurs no cost of goods sold in its financial reporting. Operating expenses are significant, with general and administrative expenses being the largest component.

PE: 11.1x

LCNB, a smaller player in the U.S. market, has shown insider confidence with recent share purchases, indicating potential value recognition by those close to the company. Despite net charge-offs rising to US$2.73 million in Q1 2026 from US$39,000 a year earlier, net interest income increased to US$18.85 million from US$16.3 million over the same period. The company also declared a quarterly dividend of $0.22 per share for June 2026 and forecasts earnings growth of 6.52% annually, suggesting cautious optimism for future performance despite recent challenges.

Black Rock Coffee Bar (BRCB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Black Rock Coffee Bar operates a chain of coffee shops and has a market capitalization of $1.5 billion.

Operations: The company generates revenue primarily from its restaurant segment, with a recent figure of $210.96 million. Over the observed periods, the gross profit margin has shown an upward trend, reaching 43.68% by March 2026. Operating expenses are significant and have been increasing, with general and administrative expenses being a major component at $78.84 million in the latest period.

PE: 552.9x

Black Rock Coffee Bar, a boutique coffee company, is expanding rapidly with new stores in Austin and Colorado. Despite recent index exclusions, the brand's growth continues as they open their eleventh Austin location and nineteenth in Colorado. However, a class action lawsuit alleges misleading statements about store expansion impacts. Their stock has dropped significantly since its IPO at US$20 per share to US$7.23 recently. Earnings guidance remains positive for 2026 despite these challenges.

Summing It All Up

- Unlock more gems! Our Undervalued US Small Caps With Insider Buying screener has unearthed 62 more companies for you to explore.Click here to unveil our expertly curated list of 65 Undervalued US Small Caps With Insider Buying.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.