Undervalued Small Caps With Insider Activity In October 2025

In a landscape where major U.S. stock indices are experiencing mixed outcomes amidst ongoing economic uncertainties, small-cap stocks often present unique opportunities for investors seeking growth potential in less saturated markets. With the Federal Reserve's recent interest rate cut and continued discussions on future monetary policy, understanding the dynamics of small-cap companies becomes crucial as they can be more sensitive to economic shifts and insider activities may provide insights into their perceived value.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Limbach Holdings | 31.4x | 2.0x | 38.58% | ★★★★★★ |

| PCB Bancorp | 8.7x | 2.8x | 33.41% | ★★★★★☆ |

| Peoples Bancorp | 9.9x | 1.8x | 47.49% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 0.8x | 29.22% | ★★★★★☆ |

| Farmland Partners | 6.6x | 8.1x | -37.83% | ★★★★☆☆ |

| First Northern Community Bancorp | 10.0x | 2.8x | 46.26% | ★★★★☆☆ |

| Thryv Holdings | NA | 0.7x | 34.50% | ★★★★☆☆ |

| Shore Bancshares | 9.2x | 2.5x | -2.74% | ★★★☆☆☆ |

| Arrow Financial | 14.2x | 3.1x | 22.71% | ★★★☆☆☆ |

| Citizens Community Bancorp | 12.0x | 2.6x | 43.72% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

NB Bancorp (NBBK)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: NB Bancorp operates as a thrift and savings and loan institution, focusing on providing financial services with a market capitalization of $1.25 billion.

Operations: NBBK generates its revenue primarily from Thrift/Savings and Loan Institutions, with recent figures indicating $189.48 million in this segment. The company has consistently achieved a gross profit margin of 100%, while the net income margin has shown fluctuations, reaching 30.72% in the latest period. Operating expenses are a significant component of costs, with general and administrative expenses being the largest portion, amounting to $105.24 million recently.

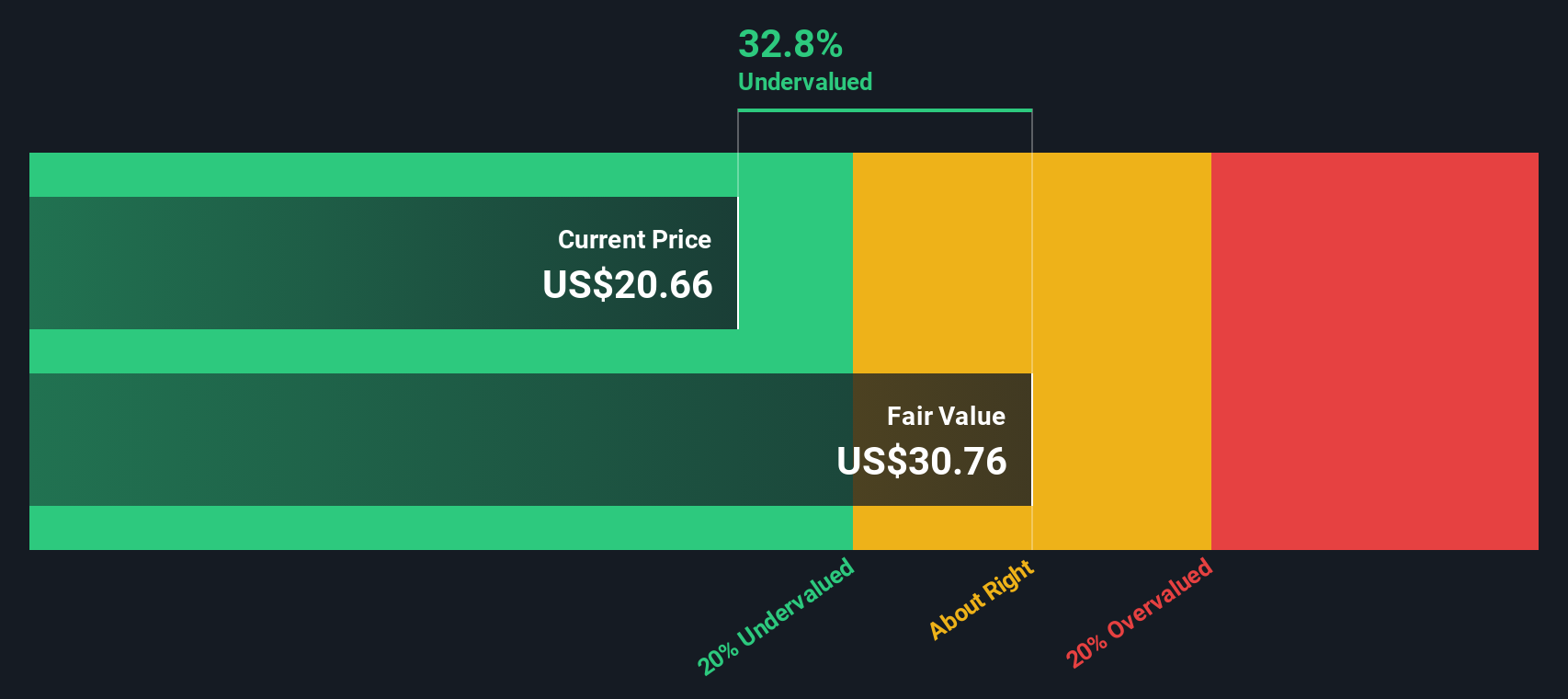

PE: 10.9x

NB Bancorp's recent financial performance highlights its potential as an undervalued investment. For the third quarter ending September 30, 2025, net interest income rose to US$48.18 million from US$41.32 million year-over-year, while net income nearly doubled to US$15.36 million. Insider confidence is evident with share purchases between July 1 and July 16, 2025, totaling 921,934 shares for US$17.5 million. Earnings are projected to grow annually by over 12%, suggesting promising future growth prospects in the banking sector despite recent charge-offs of $590,000 compared to $5.25 million a year ago.

Capital Southwest (CSWC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Capital Southwest is a business development company that primarily focuses on providing capital to middle-market companies, with a market capitalization of approximately $0.56 billion.

Operations: The company generates revenue primarily through its investment activities, with a recent figure of $209.03 million. Operating expenses have been observed at $29.38 million, impacting net income levels. Notably, the gross profit margin consistently stands at 100%, indicating that all reported revenues contribute directly to gross profit without any cost of goods sold deductions.

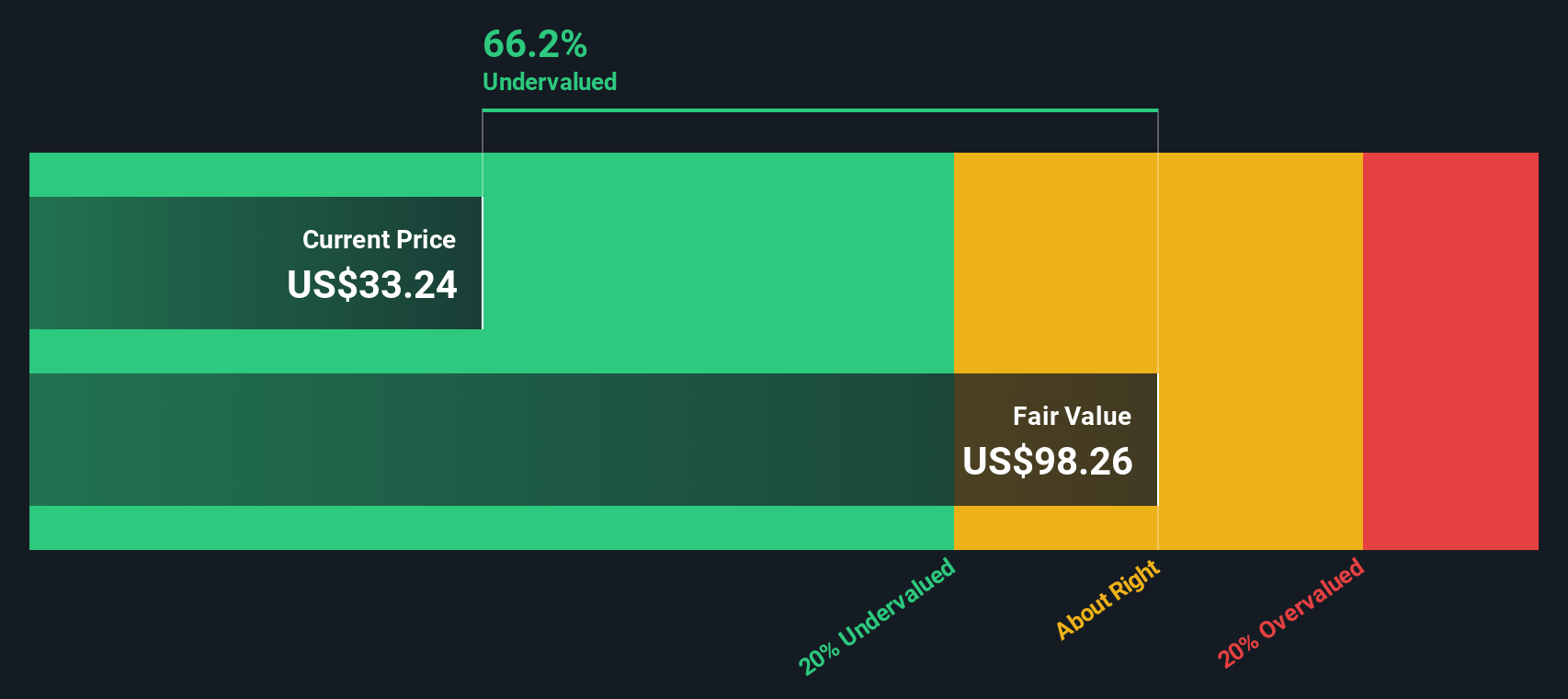

PE: 13.8x

Capital Southwest, a smaller U.S. company, recently completed a $347.71 million fixed-income offering with 5.95% senior notes due in 2030, showcasing their strategic capital management amidst external borrowing reliance. Their financial health is underscored by Q1 2025 earnings of US$27 million, up from US$14.04 million the previous year, reflecting strong growth potential despite past shareholder dilution. Insider confidence has been evident through recent share purchases, suggesting optimism about future performance and dividend stability with regular and supplemental payouts scheduled for late 2025.

GCI Liberty (GLIB.A)

Simply Wall St Value Rating: ★★★★☆☆

Overview: GCI Liberty operates in the communications services sector with a focus on providing telecommunications services, and it has a market capitalization of approximately $3.16 billion.

Operations: The company generates revenue primarily from its communications services segment, with recent figures showing $1.05 billion in revenue. Operating expenses and cost of goods sold are significant components of the company's cost structure. The gross profit margin has shown a notable trend, reaching 37.36% as of June 30, 2025, indicating changes in profitability over time.

PE: 10.5x

GCI Liberty, a player in the telecom sector, has seen insider confidence with recent purchases indicating potential belief in its growth. Despite high debt levels due to external borrowing, which poses risks, the company's financials show promise. Sales for Q2 2025 hit US$261 million, up from US$246 million last year; net income doubled to US$27 million. Inclusion in the S&P Telecom Select Industry Index suggests market recognition and could enhance visibility and investor interest moving forward.

Next Steps

- Navigate through the entire inventory of 64 Undervalued US Small Caps With Insider Buying here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.