Undervalued Small Caps With Insider Buying In July 2026

Kronos Worldwide, Inc. KRO | 0.00 |

Over the last 7 days, the United States market has risen 1.9%, contributing to a significant annual climb of 20%, with earnings forecasted to grow by 19% annually. In this environment, identifying small-cap stocks that are perceived as undervalued and exhibit insider buying can be an intriguing strategy for investors seeking opportunities aligned with current market trends.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.0x | 0.8x | 44.05% | ★★★★★★ |

| AVITA Medical | NA | 1.8x | 48.23% | ★★★★★☆ |

| Industrial Logistics Properties Trust | NA | 1.3x | 34.55% | ★★★★★☆ |

| German American Bancorp | 13.2x | 4.8x | 39.49% | ★★★☆☆☆ |

| First Bancorp | 10.8x | 4.1x | 17.51% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 12.5x | 29.64% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.6x | 2.3x | 17.10% | ★★★☆☆☆ |

| Patria Investments | 24.5x | 4.4x | 9.44% | ★★★☆☆☆ |

| Shore Bancshares | 12.2x | 3.4x | 1.93% | ★★★☆☆☆ |

| Via Transportation | NA | 3.2x | 49.81% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

Centerspace (CSR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Centerspace is a real estate company focused on owning, operating, and developing multifamily apartment communities with a market cap of approximately $0.99 billion.

Operations: Centerspace generates revenue primarily from its multifamily segment, contributing $252.93 million, with the remainder from other sources totaling $18.71 million. The company's gross profit margin has shown variability, reaching 58.89% in recent periods. Operating expenses are significant and include costs such as depreciation and general administrative expenses, which impact profitability trends over time.

PE: 118.8x

Centerspace, a smaller company in the U.S. market, is navigating challenges with strategic initiatives aimed at strengthening its balance sheet and optimizing its portfolio. Despite a first-quarter net loss of US$12.83 million, insider confidence appears strong with recent share purchases signaling potential value recognition. The company's plan to sell assets worth approximately US$240-245 million by the end of 2026 could enhance financial flexibility and focus on higher-quality markets, positioning it for future growth as multifamily fundamentals improve.

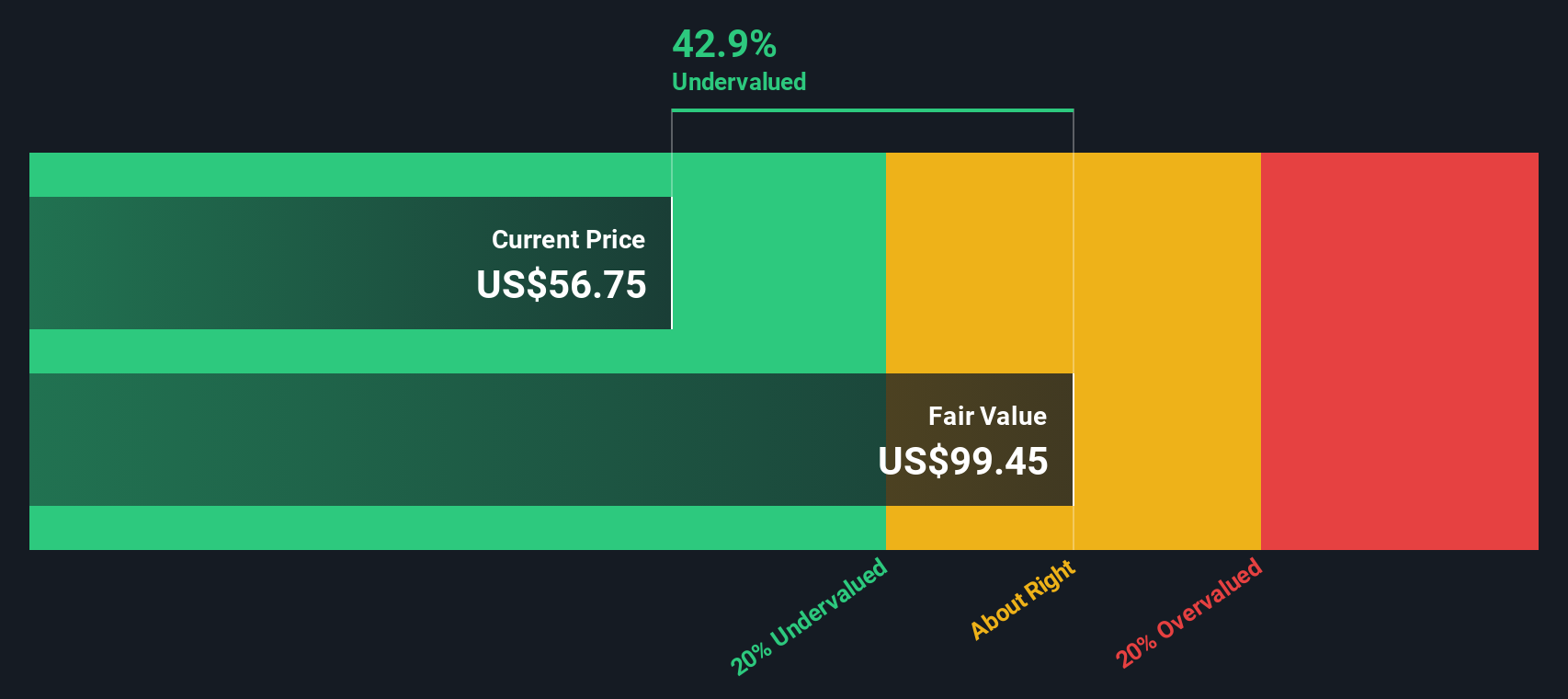

Kronos Worldwide (KRO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Kronos Worldwide is a company engaged in the production and sale of titanium dioxide pigments, with a market capitalization of approximately $1.41 billion.

Operations: The primary revenue stream comes from the production and sale of titanium dioxide pigments, totaling $1.88 billion. The gross profit margin has shown variability, recently recorded at 10.29%. Operating expenses have consistently been a significant component of costs, with recent figures at $262.1 million.

PE: -5.4x

Kronos Worldwide, a smaller player in the market, has recently faced challenges with its removal from the Russell 2000 Defensive and Value-Defensive Indexes on June 27, 2026. Despite reporting a net loss of US$4.8 million for Q1 2026 compared to a net income of US$18.1 million the previous year, insider confidence remains evident as Bart Reichert purchased 20,000 shares for US$99,200. The company declared a regular quarterly dividend of $0.05 per share in May 2026 but has not repurchased any shares this year despite completing prior buybacks worth $10.21 million since December 2010. While earnings have declined over the past five years by an average annual rate of nearly 40%, Kronos's reliance on external borrowing poses risks yet offers potential growth opportunities if managed effectively.

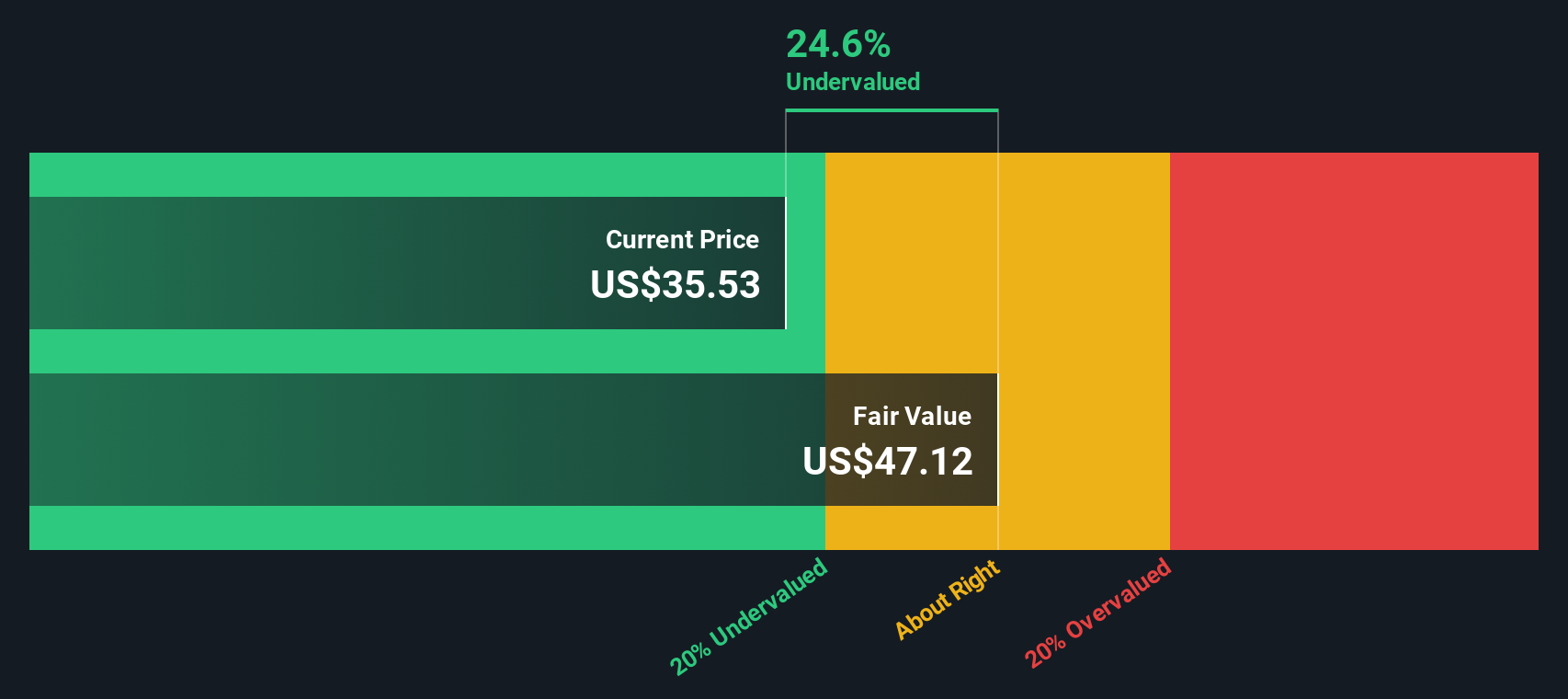

Via Transportation (VIA)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Via Transportation is a technology company specializing in providing software solutions for on-demand and dynamic public transportation systems, with a market cap of approximately $3.5 billion.

Operations: Via Transportation's revenue has shown growth from $248.85 million to $463.13 million over the reported periods, while its cost of goods sold (COGS) increased correspondingly from $149.45 million to $281.08 million, impacting profitability. The company's gross profit margin fluctuated slightly but remained around 39%, indicating a stable relationship between revenue and COGS despite rising operating expenses, which include significant investments in research and development and sales and marketing efforts.

PE: -14.7x

Via Transportation, a company with significant insider confidence, recently saw Nechemia Peres purchase 25,000 shares for US$367,500. Despite being currently unprofitable and reliant on higher-risk external borrowing, its revenue is growing. The launch of their AI-driven Scheduling and Supply Studio aims to optimize transit operations for agencies under budget constraints. First-quarter sales rose to US$127 million from US$99 million last year. Future projections suggest platform revenues could reach up to US$550 million in 2026.

Summing It All Up

- Access the full spectrum of 64 Undervalued US Small Caps With Insider Buying by clicking on this link.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.