Undiscovered Gems In The US Market With Strong Potential

Betterware de Mexico, S.A.P.I. de C.V. BWMX | 0.00 |

Over the last 7 days, the United States market has remained flat, yet it is up 26% over the past year with earnings expected to grow by 17% per annum in the coming years. In this environment, identifying stocks with strong fundamentals and growth potential can be key to uncovering undiscovered gems that align well with these promising market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| West Bancorporation | 142.32% | -3.52% | -12.71% | ★★★★★★ |

| Imperial Petroleum | NA | 29.81% | 34.96% | ★★★★★★ |

| Northeast Bank | 126.85% | 12.54% | 9.06% | ★★★★★★ |

| Brady | 2.00% | 6.15% | 10.01% | ★★★★★☆ |

| CF Bankshares | 63.11% | -6.95% | -10.61% | ★★★★★☆ |

| Alto Ingredients | 29.24% | -3.75% | -29.59% | ★★★★★☆ |

| TOYO | 57.03% | 225.22% | 49.41% | ★★★★☆☆ |

| Kingstone Companies | 3.60% | 7.12% | 57.97% | ★★★★☆☆ |

| Meridian | 86.20% | -9.29% | -18.08% | ★★★★☆☆ |

| GDEV | NA | 3.52% | 49.82% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

Belden (BDC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Belden Inc. offers connection solutions to align data infrastructure and has a market cap of $4.26 billion.

Operations: Belden generates revenue primarily through its connection solutions aimed at enhancing data infrastructure.

Belden, a notable player in the electronic industry, is making strides with its focus on digital transformation and automation. The company reported first-quarter sales of US$696 million, up from US$625 million last year, while net income slightly dipped to US$51 million from US$52 million. With earnings per share rising to US$1.31 from US$1.29, Belden's strategic investments in software and integration seem promising for future growth. Its debt-to-equity ratio has improved significantly over five years, dropping from 180% to 98%, indicating better financial health despite a high current net debt level of 77%.

Brady (BRC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Brady Corporation specializes in manufacturing and supplying identification solutions and workplace safety products across various regions, with a market cap of approximately $4.12 billion.

Operations: Revenue is primarily generated from two segments: the Americas & Asia, contributing $1.07 billion, and Europe & Australia with $550.60 million.

Brady, a company with a focus on automation and compliance solutions, has been actively enhancing its market position through strategic acquisitions and R&D investments. Its recent earnings report for the third quarter showed an increase in sales to US$435 million from US$383 million the previous year, while net income rose to US$57.8 million from US$52.3 million. Despite these gains, Brady adjusted its annual earnings guidance slightly downward to between $4.66 and $4.76 per share due to anticipated margin pressures as profit margins are expected to dip from 12.9% to 10.1%. The firm completed a significant share buyback program, repurchasing over 4 million shares for approximately US$227 million since May 2022, reflecting confidence in its valuation amidst ongoing global expansion efforts despite challenges like trade barriers and slow growth in mature markets such as Europe and Australia.

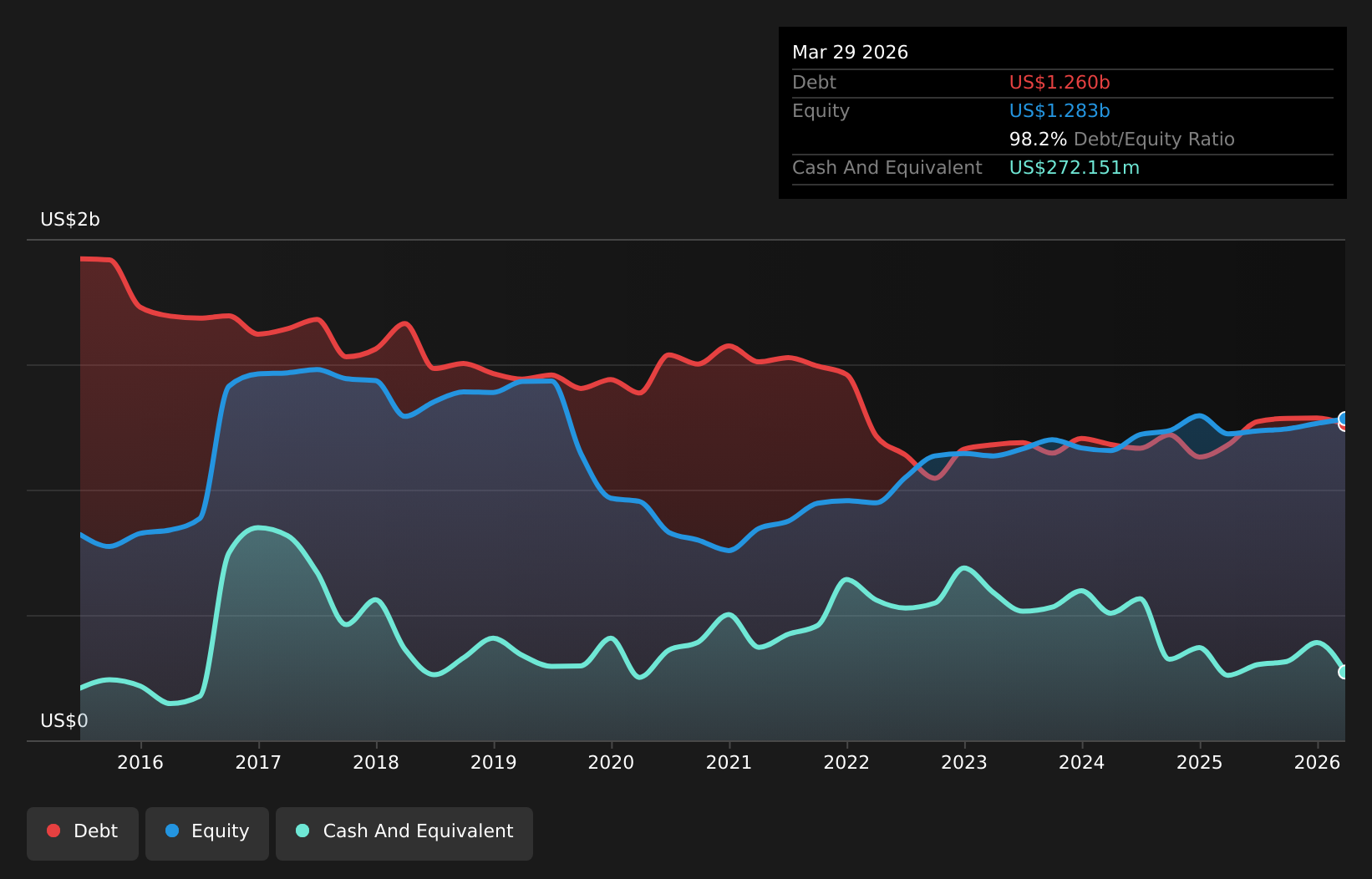

Betterware de MéxicoP.I. de (BWMX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Betterware de México, S.A.P.I. de C.V. operates as a direct-to-consumer selling company in the United States and Mexico, with a market cap of $702.05 million.

Operations: Revenue is primarily generated through direct-to-consumer sales in the United States and Mexico. The company focuses on optimizing its cost structure to enhance profitability, with attention to managing expenses effectively. Notably, the net profit margin has shown variability over recent periods.

Betterware de México is making strides with its expansion into Latin American markets, boosting earnings by 106.5% last year, outpacing the specialty retail industry. Despite a high net debt to equity ratio of 252.1%, interest payments are well-covered at 5.1 times by EBIT, indicating financial resilience. The company trades at a good value, estimated to be 42% below fair value while maintaining high-quality earnings and positive free cash flow of US$2.62 billion as of June 2026. However, challenges like aggressive pricing strategies and regulatory pressures could impact future growth potential despite promising market expansions and digital transitions enhancing revenue streams.

Turning Ideas Into Actions

- Gain an insight into the universe of 20 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.