UniFirst (UNF) After Recent Share Gains Looks Close To Fair Value

UniFirst Corporation UNF | 0.00 |

UniFirst (UNF) is back on investors’ radar after recent share price moves drew attention to its longer term record, with the stock showing gains over the past year and over the past 3 months.

Recent trading in UniFirst shares follows a longer period of gains, including a strong year to date share price return and multi year total shareholder returns that suggest investors may be reassessing both its growth prospects and its risk profile.

If you are reassessing your own watchlist in light of UniFirst’s move, this could be a useful moment to widen the search and check out 20 top founder-led companies

With UniFirst shares up strongly over the past year and trading only slightly below analyst price targets, the key question is whether the stock still offers value or if markets are already pricing in future growth.

Most Popular Narrative: 5% Undervalued

UniFirst's most followed valuation story pegs fair value at about $279 per share, a touch above the latest close around $266, which puts the current price under the microscope.

UniFirst is seeing improvements in operational execution and margin enhancement, with notable margin improvements in Core Laundry Operations, which is expected to positively impact net margins and earnings.

Significant investments in technology, specifically an ERP system, are anticipated to enhance efficiency, leading to improved profitability and reduced operational costs once fully implemented, which should impact net margins positively in the long run.

Curious how a uniform rental business supports this valuation gap? The narrative leans on steadier margins, measured growth, and a rich future earnings multiple. The exact mix of growth, profitability and discount rate assumptions is where the story really gets interesting.

Result: Fair Value of $279 (UNDERVALUED)

However, UniFirst’s story still depends on customer demand remaining stable and health care costs staying manageable, both of which could pressure margins if they move in an unfavorable direction.

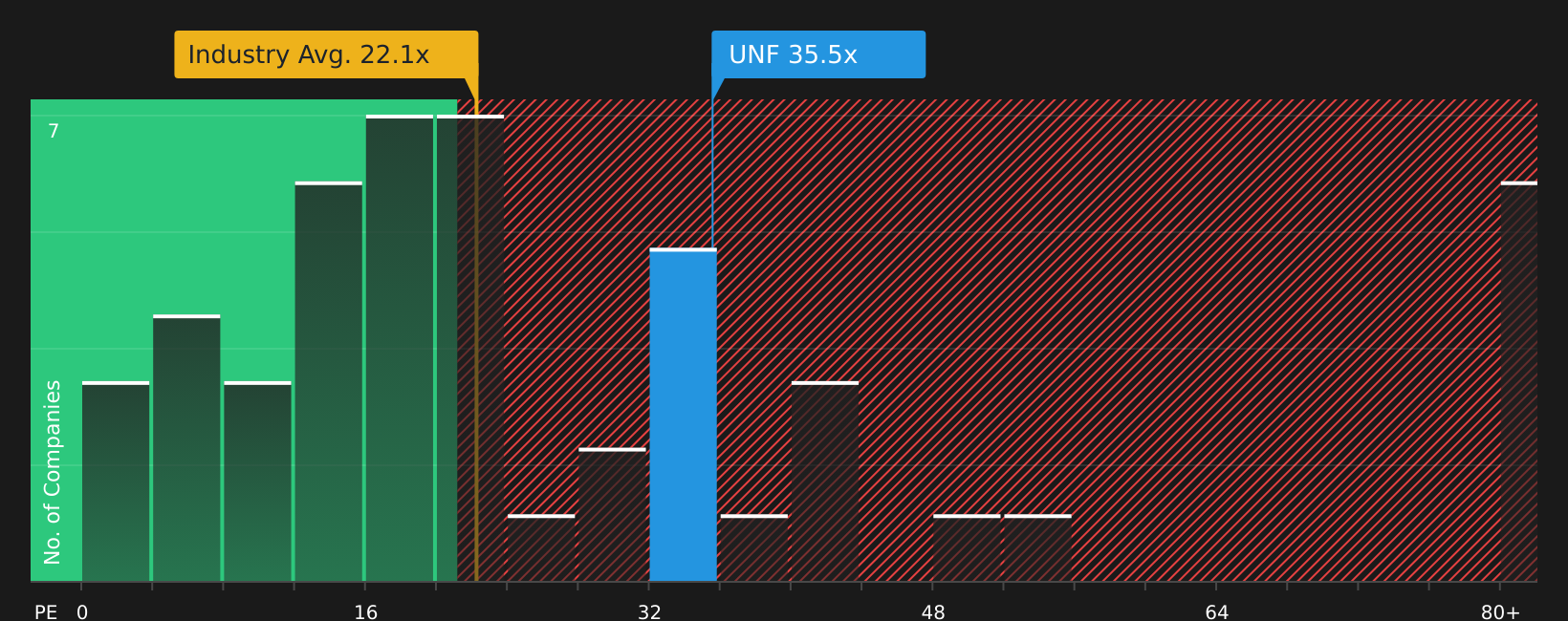

Another View: UniFirst Through Its P/E Ratio

While the popular UniFirst story focuses on a fair value of $279 per share, the current P/E ratio of 35.5x tells a tougher tale. It stands above the Commercial Services industry at 22.1x and a fair ratio estimate of 18x, which points to valuation risk if sentiment cools.

For a closer look at how this pricing compares across peers and what the gap could mean if the market moves back toward the fair ratio, take a look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of optimism and valuation questions around UniFirst, this is a good time to look at the numbers yourself and then move quickly to form your own view, starting with the 1 key reward.

Looking for more investment ideas beyond UniFirst?

If UniFirst has you rethinking your portfolio, do not stop here. These other ideas could be where your next strong opportunity comes from.

- Target stability by reviewing companies screened for resilience in volatile conditions through the 71 resilient stocks with low risk scores.

- Hunt for potential mispricing and compare UniFirst with stocks identified as attractively valued using the 44 high quality undervalued stocks.

- Strengthen your income focus by checking out companies with robust payouts and balance sheets via the 8 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.