شركة يونيون بروبرتيز وجوهرتان أخريان غير مكتشفتين تتمتعان بأسس قوية

السيف غاليري 4192.SA | 0.00 |

مع ازدهار أسواق الخليج مدفوعةً بأرباح الشركات القوية والتفاؤل المحيط باتفاق سلام محتمل بين الولايات المتحدة وإيران، يتجه المستثمرون بشكل متزايد نحو فرص الاستثمار في أسهم الشركات الصغيرة والمتوسطة في المنطقة. وفي ظل هذه البيئة الديناميكية، يصبح تحديد الأسهم ذات الأساسيات القوية أمراً بالغ الأهمية لمن يسعى للاستفادة من المشهد السوقي المتطور في الشرق الأوسط.

أفضل 10 جواهر غير مكتشفة ذات أسس قوية في الشرق الأوسط

| اسم | نسبة الدين إلى حقوق الملكية | نمو الإيرادات | نمو الأرباح | التقييم الصحي |

|---|---|---|---|---|

| شركة الوثبة الوطنية للتأمين ش.م.ع | 10.35% | 8.65% | -7.40% | ★★★★★★ |

| محلل في شركة IMS لخدمات إدارة الاستثمار | غير متوفر | 33.12% | 45.12% | ★★★★★★ |

| منتجات نوفوث الغذائية | غير متوفر | 20.62% | 23.75% | ★★★★★★ |

| Tureks Turizm Tasimacilik Anonim Sirketi | 5.61% | 45.04% | 46.56% | ★★★★★★ |

| صناعة الهواتف المحمولة | 7.46% | 5.89% | 17.98% | ★★★★★★ |

| شركة السعودية القابضة للكيميائيات | 47.39% | 17.85% | 39.66% | ★★★★★☆ |

| Gür-Sel Turizm Tasimacilik ve Servis Ticaret | 4.54% | 30.75% | 51.95% | ★★★★★☆ |

| Kirac Galvaniz Telekominikasyon Metal Machine Insaat Elektrik Sanayi ve Ticaret Anonim Sirketi | 21.92% | 19.33% | 42.01% | ★★★★★☆ |

| زهرة الواحة للتجارة | 56.06% | -0.88% | -37.72% | ★★★★☆☆ |

| Mobiltel Iletisim Hizmetleri Sanayi ve Ticaret | 22.16% | 9.01% | -17.85% | ★★★★☆☆ |

سنقوم بفحص مجموعة مختارة من نتائج الفحص الأولي.

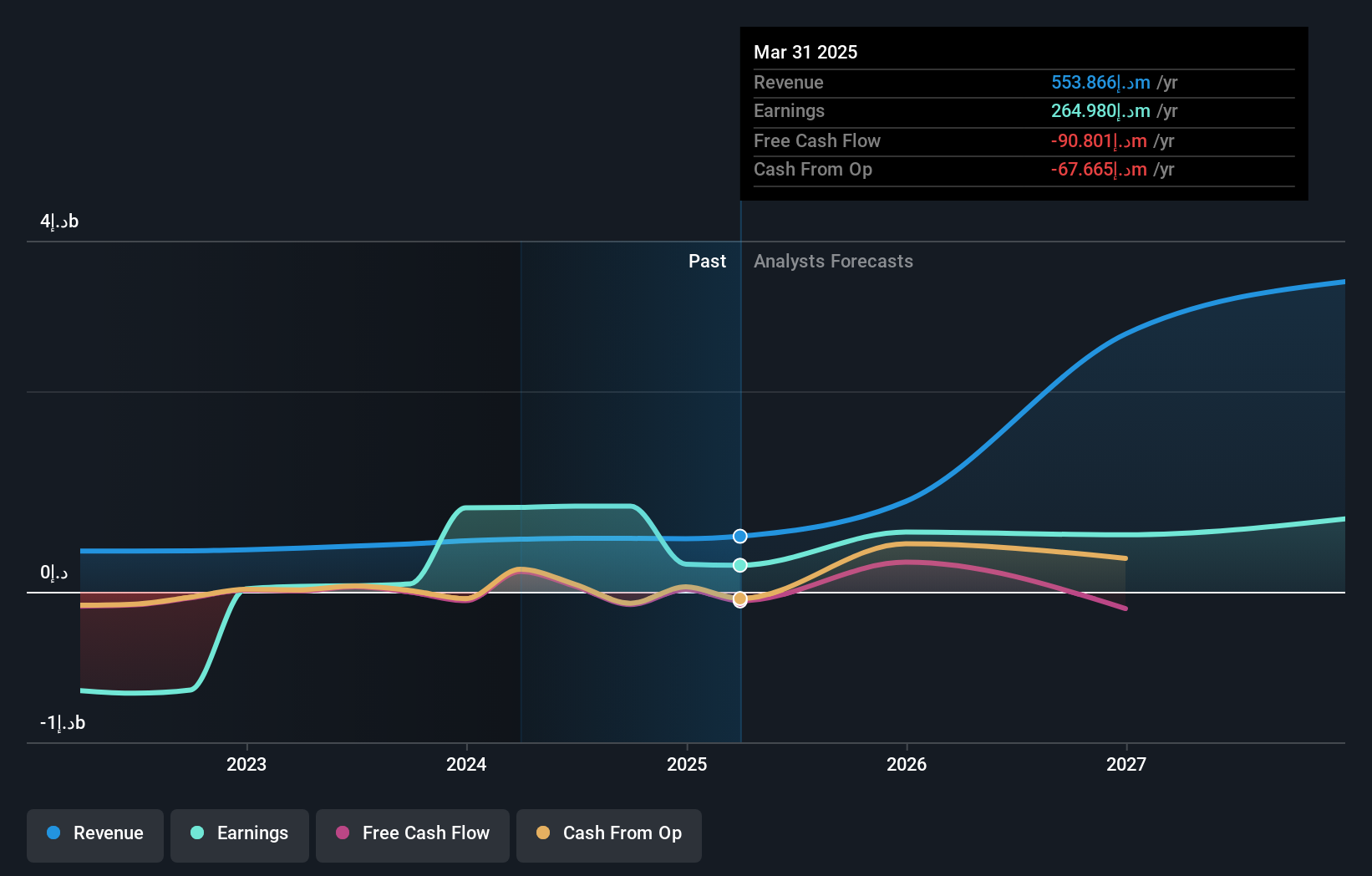

شركة يونيون بروبرتيز (DFM:UPP)

تقييم Simply Wall St للقيمة: ★★★★★☆

نظرة عامة: تعمل شركة يونيون بروبرتيز المساهمة العامة في مجال الاستثمار والتطوير العقاري، برأسمال سوقي قدره 3.20 مليار درهم إماراتي.

العمليات: تحقق شركة يونيون بروبرتيز إيراداتها بشكل أساسي من السلع والخدمات (491.13 مليون درهم إماراتي)، وخدمات التدبير المنزلي (95.61 مليون درهم إماراتي)، والمقاولات (69.12 مليون درهم إماراتي)، والأنشطة العقارية (81.02 مليون درهم إماراتي).

حققت شركة يونيون بروبرتيز، وهي شركة أصغر حجماً في سوق الشرق الأوسط، نمواً مالياً ملحوظاً، حيث ارتفعت أرباحها بنسبة 67.8% العام الماضي، متجاوزةً بذلك متوسط القطاع البالغ 5.7%. وانخفضت نسبة الدين إلى حقوق الملكية للشركة بشكل ملحوظ من 57.2% إلى 8.9% على مدى خمس سنوات، مما يشير إلى تحسن وضعها المالي. وعلى الرغم من تأثير مكسب استثنائي كبير بقيمة 574 مليون درهم إماراتي على النتائج الأخيرة، إلا أن يونيون بروبرتيز لا تزال تحقق أرباحاً مع تدفق نقدي حر إيجابي، ويتم تداول أسهمها بخصم طفيف قدره 3.1% عن قيمتها العادلة المقدرة. ومن المتوقع أن تنمو الإيرادات المستقبلية بنحو 39%، مما يشير إلى إمكانية استمرار التوسع في السنوات القادمة.

رونيسانس جايريمينكول ياتريم (IBSE:RGYAS)

تقييم سيمبلي وول ستريت: ★★★★☆☆

نظرة عامة: شركة رونيسانس غايريمينكول ياتيريم إيه إس هي شركة تطوير واستثمار عقاري تجاري في تركيا، برأسمال سوقي قدره 63.06 مليار ليرة تركية.

العمليات: تُحقق شركة رونيسانس غايريمينكول ياتيريم المساهمة إيراداتها بشكل أساسي من مراكز التسوق والمكاتب التابعة لها، حيث يُساهم مركز هيلتاون كارسياكا للتسوق ومركز هيلتاون للتسوق والمكاتب بمبلغ 2.18 مليار ليرة تركية و1.85 مليار ليرة تركية على التوالي. ويعكس هامش الربح الصافي للشركة أداءها المالي في هذا القطاع.

أظهرت شركة رونيسانس غايريمينكول ياتيريم، وهي شركة صغيرة في قطاع العقارات، وضعًا ماليًا متميزًا خلال السنوات الأخيرة. فقد تحسنت نسبة الدين إلى حقوق الملكية للشركة بشكل ملحوظ من 144.8% إلى 26.9%، مما يعكس إدارة مالية قوية. ومع ارتفاع أرباحها بنسبة 165.8% العام الماضي، تفوقت رونيسانس غايريمينكول ياتيريم على معدل نمو القطاع الأوسع الذي بلغ 59%. وعلى الرغم من وجود مكسب استثنائي ملحوظ بقيمة 6.1 مليار ليرة تركية أثر على نتائجها الأخيرة، إلا أن نسبة سعر السهم إلى الأرباح منخفضة بشكل جذاب عند 3.9 ضعف مقارنة بمتوسط السوق التركي البالغ 20.6 ضعف، مما يشير إلى احتمال انخفاض قيمة السهم عن قيمته الحقيقية، ويوفر فرصًا واعدة للمستثمرين الباحثين عن فرص استثمارية قيّمة في الأسواق الناشئة مثل تركيا.

متاجر السيف للتنمية والاستثمار (SASE:4192)

تقييم Simply Wall St للقيمة: ★★★★★★

نظرة عامة: تعمل شركة متاجر السيف للتطوير والاستثمار في قطاعي البيع بالجملة والتجزئة، وتركز على الأدوات المنزلية والأجهزة الكهربائية ومستلزمات التنظيف في المملكة العربية السعودية، برأسمال سوقي قدره 2.45 مليار ريال سعودي.

العمليات: يأتي مصدر الإيرادات الرئيسي لمتاجر السيف من بيع واستيراد الأدوات المنزلية والأجهزة الكهربائية، محققاً 758.85 مليون ريال سعودي. ويُعد هامش الربح الإجمالي للشركة مؤشراً مالياً رئيسياً يجب مراعاته عند تحليل ربحيتها.

أظهرت شركة السيف للمتاجر للتنمية والاستثمار، وهي شركة رائدة في قطاع التجزئة بالشرق الأوسط، وضعاً مالياً متميزاً، حيث حققت نمواً في الأرباح بنسبة 54.6% خلال العام الماضي، متجاوزةً بذلك متوسط القطاع البالغ 16.8%. وتتميز الشركة بخلوها من الديون، مما يعزز استقرارها المالي ويقلل من المخاطر. وتشير النتائج الأخيرة إلى ارتفاع صافي الدخل إلى 58 مليون ريال سعودي مقارنةً بـ 37.54 مليون ريال سعودي في العام الماضي، مدعوماً بمبيعات بلغت 758.85 مليون ريال سعودي. وعلى الرغم من توقعات نمو الإيرادات المتواضعة بنحو 4%، فإن جودة أرباحها العالية وتوزيعات الأرباح الاستراتيجية تشير إلى كفاءة تشغيلية قوية وإمكانية تحقيق ربحية مستدامة في المستقبل.

إلى أين الآن؟

- اكتشف المزيد من الفرص الاستثمارية الواعدة! كشف برنامجنا لفحص الشركات الواعدة في الشرق الأوسط، والتي تتمتع بأسس قوية، عن 223 شركة إضافية يمكنك استكشافها. انقر هنا للاطلاع على قائمتنا المختارة بعناية والتي تضم 226 شركة واعدة في الشرق الأوسط تتمتع بأسس قوية .

- هل قمت بتنويع استثماراتك في هذه الشركات؟ استفد من قوة محفظة Simply Wall St لمتابعة تحركات السوق التي تؤثر على استثماراتك عن كثب.

- عزز قدراتك الاستثمارية باستخدام تطبيق Simply Wall St واستمتع بالوصول المجاني إلى معلومات السوق الأساسية التي تغطي جميع القارات.

هل تفكر في استراتيجيات أخرى؟

- استكشف الشركات الصغيرة ذات الأداء العالي التي لم تحظَ بعد باهتمام كبير من المحللين.

- قم بتعزيز محفظتك الاستثمارية بالشركات التي تُظهر إمكانات نمو قوية، مدعومة بتوقعات متفائلة من المحللين والإدارة على حد سواء .

- ابحث عن شركات ذات إمكانات تدفق نقدي واعدة ولكنها تتداول بأقل من قيمتها العادلة .

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.