uniQure (QURE) Closed A Major Funding Round, Is The Pipeline Already Priced In?

uniQure N.V. QURE | 0.00 |

uniQure (NasdaqGS:QURE) is back in focus after closing an upsized public offering that raised roughly US$259 million, following fresh clinical updates in Huntington’s disease and epilepsy that have sharpened attention on its gene therapy pipeline.

That funding news comes after a sharp re-rating in uniQure’s share price, which has risen strongly in recent months, with a 30 day share price return of 66.53% and a 1 year total shareholder return of 242.78%. This suggests momentum has been building as investors reassess both pipeline progress and perceived financing risk.

If recent gene therapy headlines have caught your attention, this could be a good moment to widen your watchlist with other healthcare opportunities using the 39 healthcare AI stocks

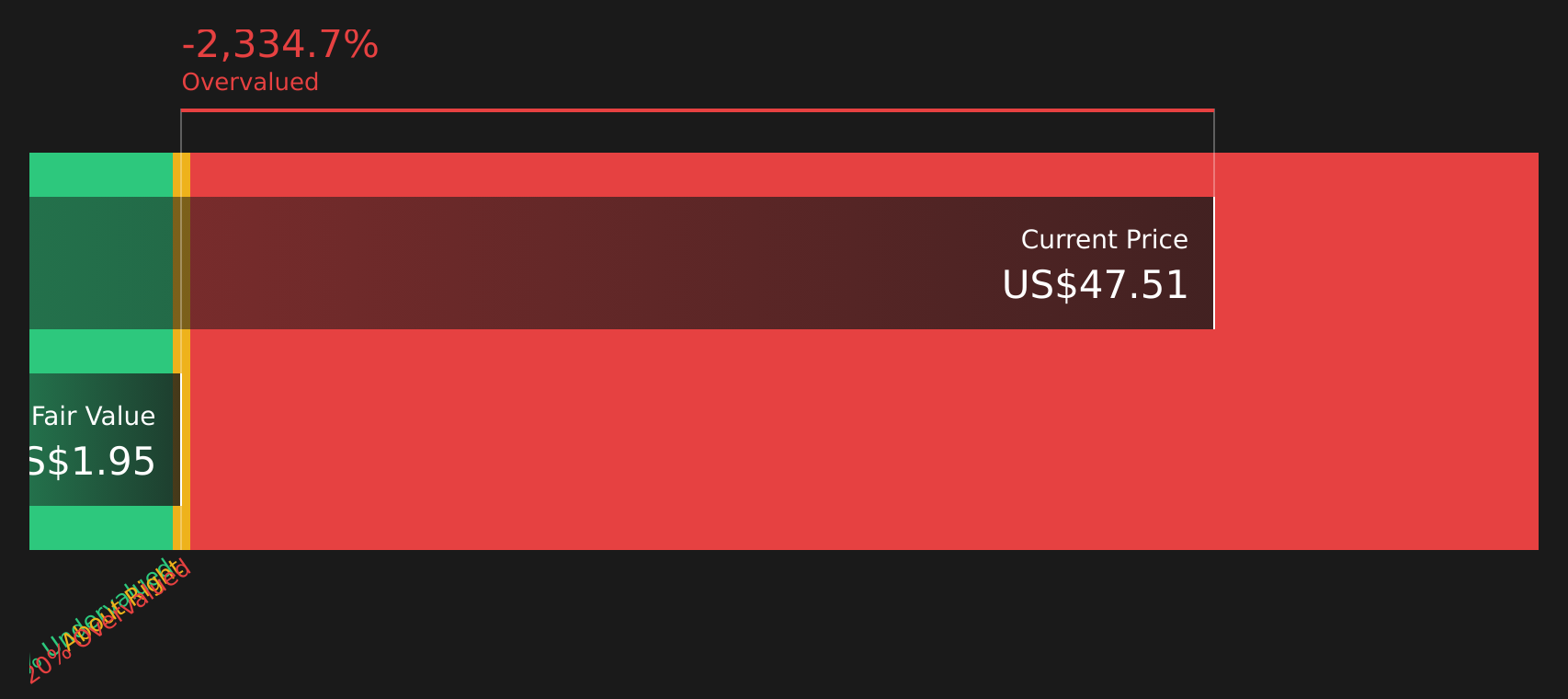

After a run like this and fresh capital in the bank, the key question is whether uniQure at about US$47.51 is still trading below what its future pipeline could justify, or if the market has already priced in that growth.

Most Popular Narrative: 10% Undervalued

With uniQure trading at about $47.51 against a narrative fair value of roughly $52.56, the current share price sits below what this widely followed framework implies.

The analysts have a consensus price target of $52.56 for uniQure based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $93.29, and the most bearish reporting a price target of just $24.54.

Analysts are incorporating expectations of rapid revenue expansion, a significant change in margins, and a high future earnings multiple. This raises the question of which assumptions are most important for that fair value.

Result: Fair Value of $52.56 (UNDERVALUED)

However, the uniQure story still hinges heavily on AMT-130’s regulatory path and on clinical and manufacturing risks that, if they break the wrong way, could quickly challenge this view of undervaluation.

Another View: SWS DCF Model Flags a Very Different Picture

While the analyst narrative implies uniQure might still be around 10% undervalued at $47.51, the Simply Wall St DCF model points the other way. On that framework, the stock trades far above an estimated future cash flow value of about $1.95, which screens as overvalued. That kind of gap often reflects how sensitive early stage biotech valuations are to small changes in long term assumptions. Which framework do you trust more for a loss making, trial heavy story like this?

For a closer look at how this cash flow based view is built and what would need to change to support today’s share price, take a few minutes to walk through the Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out uniQure for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing both enthusiasm and caution around uniQure, it makes sense to review the full picture yourself and move quickly to form your own view using the 1 key reward and 4 important warning signs.

Looking for more ideas beyond uniQure?

If uniQure has sharpened your interest in focused stock picking, do not stop here, broaden your watchlist now and pressure test your next ideas properly.

- Target potential value opportunities early by scanning the 44 high quality undervalued stocks and see which stocks might currently trade below what their fundamentals suggest.

- Prioritise resilience by checking the solid balance sheet and fundamentals stocks screener (48 results) to find companies that pair financial strength with disciplined fundamentals.

- Stay ahead of the crowd by using the screener containing 19 high quality undiscovered gems before these under followed ideas attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.