US Market's Undiscovered Gems Featuring 3 Promising Small Caps

Daktronics, Inc. DAKT | 0.00 |

The United States market has shown robust performance, climbing 1.4% in the last week and rising 19% over the past year, with earnings projected to grow by a similar margin annually. In this thriving environment, identifying promising small-cap stocks that may not yet be on every investor's radar can offer unique opportunities for growth and diversification.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Century Aluminum | 42.50% | 2.68% | 57.56% | ★★★★★★ |

| Imperial Petroleum | NA | 29.81% | 34.96% | ★★★★★★ |

| Daktronics | 3.58% | 9.04% | 26.79% | ★★★★★★ |

| Waterdrop | 5.26% | 2.09% | 66.26% | ★★★★★☆ |

| CF Bankshares | 63.11% | -6.95% | -10.61% | ★★★★★☆ |

| Fortress Biotech | 19.46% | 0.53% | 26.21% | ★★★★★☆ |

| Alto Ingredients | 29.24% | -3.75% | -29.59% | ★★★★★☆ |

| TOYO | 57.03% | 225.22% | 49.41% | ★★★★☆☆ |

| Betterware de MéxicoP.I. de | 273.07% | 9.15% | -7.33% | ★★★☆☆☆ |

| GDEV | NA | 3.52% | 49.82% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

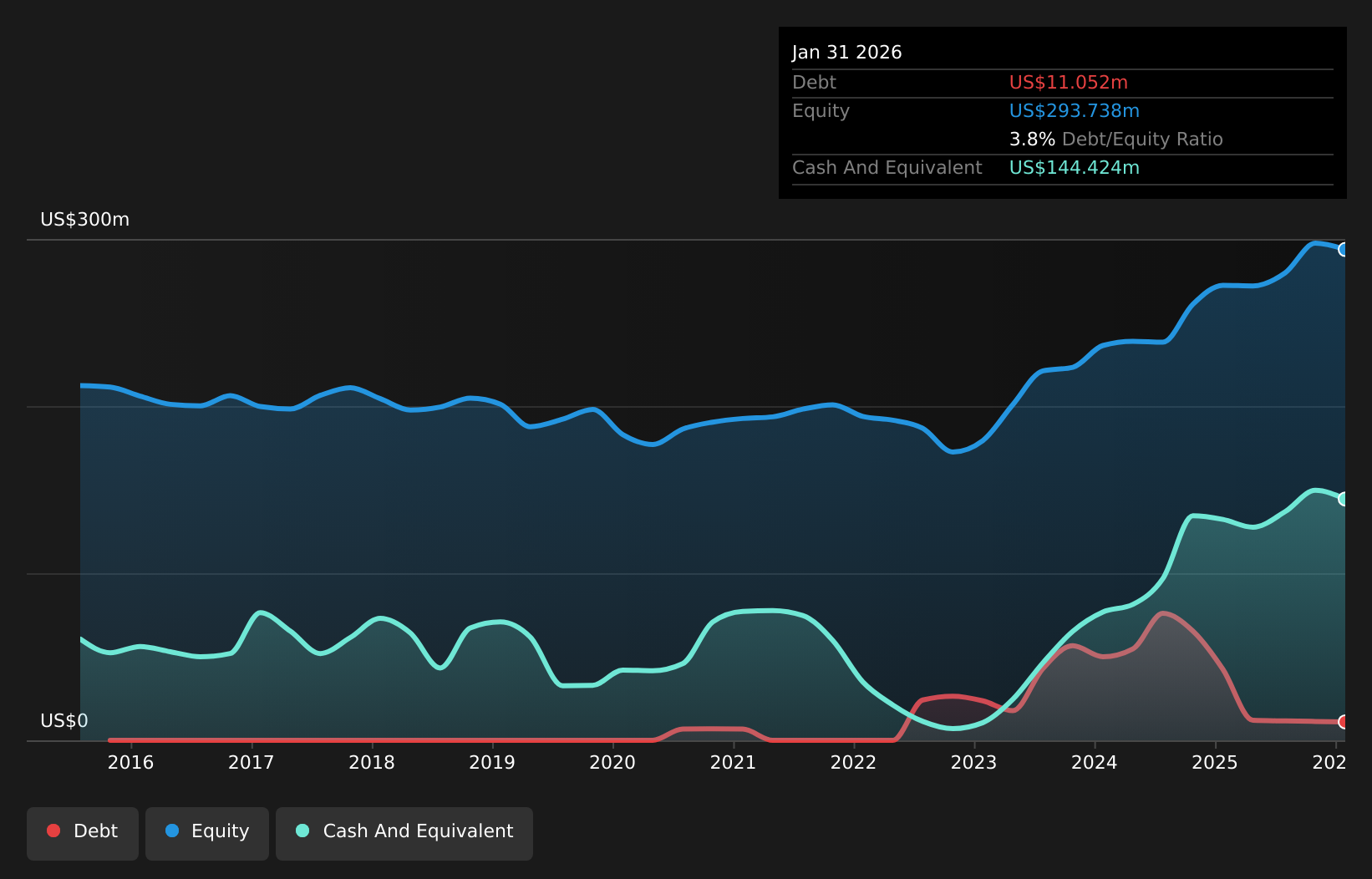

Daktronics (DAKT)

Simply Wall St Value Rating: ★★★★★★

Overview: Daktronics, Inc. specializes in designing, manufacturing, and selling electronic display systems for sports, commercial, and transportation applications worldwide with a market capitalization of approximately $960.87 million.

Operations: The company generates revenue from five primary segments: Commercial ($180.77 million), Live Events ($321.05 million), International ($76.93 million), Transportation ($76.70 million), and High School Park and Recreation ($183.25 million).

Daktronics, a company with a market cap that doesn't quite hit the big leagues, has shown significant financial improvement over recent years. Five years ago, it had negative shareholder equity but now boasts positive figures. This year marked its transition to profitability with net income reaching US$45.38 million compared to last year's loss of US$10.12 million and earnings per share climbing to US$0.93 from a previous loss of US$0.21 per share. The firm also reported robust sales growth for the full year at US$838.71 million, up from US$756.48 million previously, while maintaining more cash than total debt and trading 5% below estimated fair value despite recent index exclusions like Russell 2000 Value Benchmark drops due to strategic shifts towards growth-defensive indices amidst expanding digital display demand in smart city projects and recreational markets driving future prospects forward albeit with cyclical risks present too!

Betterware de MéxicoP.I. de (BWMX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Betterware de México, S.A.P.I. de C.V. is a direct-to-consumer selling company operating in the United States and Mexico with a market cap of $663.31 million.

Operations: BWMX generates revenue primarily through direct-to-consumer sales in the United States and Mexico. The company's financial performance includes a notable net profit margin trend, which has varied over recent periods.

Betterware de México's recent performance paints an intriguing picture, with net income for Q1 2026 at MX$281 million, a notable increase from MX$151 million the previous year. The company is trading at nearly half its estimated fair value, suggesting potential upside. Despite a high net debt to equity ratio of 252%, interest payments are well-covered by EBIT at 5.1 times coverage. Earnings growth over the past year was impressive at 106%, outpacing industry averages significantly. However, challenges remain with its high debt levels and reliance on aggressive pricing strategies in competitive markets.

Waterdrop (WDH)

Simply Wall St Value Rating: ★★★★★☆

Overview: Waterdrop Inc. operates as an online insurance brokerage, connecting users with insurance products in China, and has a market cap of approximately $416.79 million.

Operations: The company generates revenue primarily from its insurance segment, totaling CN¥4.06 billion, followed by crowd funding at CN¥255.23 million.

Waterdrop, a nimble player in the insurance sector, has shown robust earnings growth of 41.5% over the past year, outpacing its industry peers. Despite a slight uptick in its debt-to-equity ratio to 5.3% over five years, it remains comfortably positioned with more cash than total debt and positive free cash flow. The company recently completed a share buyback of 1.46%, spending US$9.54 million, signaling confidence in its valuation which trades at 37.6% below fair value estimates. With new leadership on board and projected annual earnings growth of 12%, Waterdrop seems poised for continued strength.

Summing It All Up

- Gain an insight into the universe of 15 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.