Vale Stock And 2 Steel Names Facing Fresh Tariff Pressure

Nucor Corporation NUE | 0.00 |

Trade tensions between the US, EU, and Brazil over steel and pig iron are reshaping parts of the global metals supply chain in real time, and that kind of disruption can quickly spill over into stock prices. With US tariffs on Brazilian pig iron set as high as 37.5% and tight EU quotas on Brazilian steel, some companies face higher costs, squeezed margins, or restricted market access. This article breaks down three stocks directly exposed to these new trade barriers, all on the risk side of the ledger, to help you evaluate whether they belong on your watchlist or your avoid list.

Vale (BOVESPA:VALE3)

Overview: Vale is a Brazilian mining group that produces and sells iron ore, pellets, nickel, copper and other metals worldwide, while also operating its own railways, ports, shipping and power assets to move and process what it digs out of the ground. Alongside iron ore, the company is building exposure to low carbon and critical minerals that feed electric vehicles and renewable energy supply chains.

Operations: Vale generates most of its revenue from Iron Ore Solutions at about R$166.5b, with a smaller but meaningful contribution of roughly R$48.4b from its base metals business.

Market Cap: R$333.7b

Investors watching steel trade tensions may find Vale hard to ignore, but the story currently leans more cautionary than compelling. The stock is heavily dependent on iron ore, just as new US and EU tariffs on Brazilian steel related products threaten export volumes and add uncertainty around pricing and demand. Earnings have been under pressure, margins have compressed from prior levels, and a large one off loss of R$26.6b in the last 12 months, combined with high debt, underlines how sensitive the business is to shocks. At the same time, a relatively rich P/E and dividends that are not well covered by earnings or free cash flow raise the bar for the upside case investors need to believe in.

Vale’s rich P/E, high debt and that R$26.6b loss hint that trade shocks might be masking deeper issues, so it could be worth reading the 1 key reward and 4 important warning signs (1 is major!)

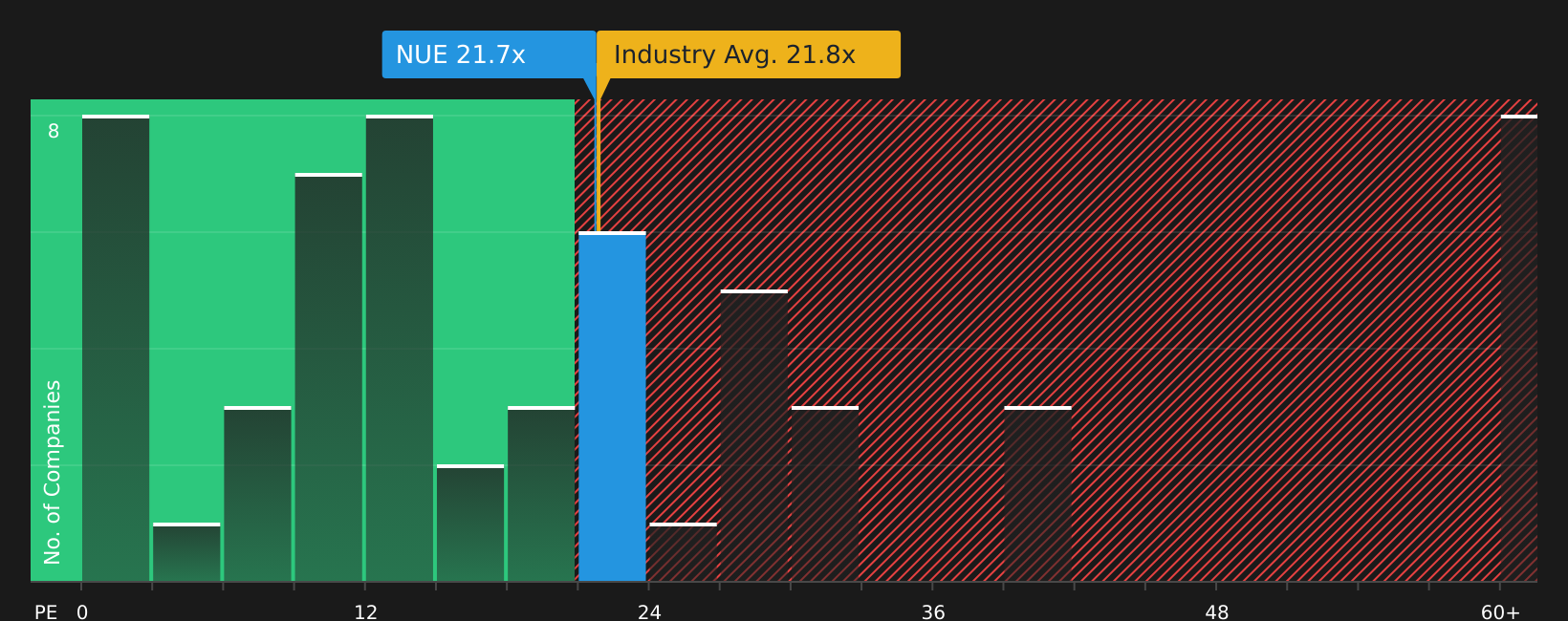

Nucor (NUE)

Overview: Nucor is a US based steel producer that makes a wide range of sheet, plate, bar and structural steel, as well as finished steel products used in construction, manufacturing, energy and infrastructure projects across North America.

Operations: Nucor generates most of its revenue from its Steel Mills segment at about US$26.6b, with Raw Materials contributing around US$13.3b and Steel Products about US$11.4b, partly offset by US$17.1b of corporate and intersegment eliminations.

Market Cap: US$49.9b

Nucor may look appealing with forecasts of solid earnings growth, a long dividend track record and analysts seeing the stock below their estimated value. However, the new US tariffs on Brazilian pig iron affect a key raw material. Management highlights its flexibility in switching to alternatives such as DRI and low copper scrap. Even so, margin pressure, a relatively low current ROE of 11.9% and a balance sheet funded entirely by higher risk borrowing provide less room for error if steel prices or demand soften. In addition, recent insider selling and a relatively new management team may make the bullish story appear more fragile than headline upgrades suggest.

Nucor’s earnings story looks solid on the surface, but an 11.9% ROE, full reliance on higher risk borrowing and new pig iron tariffs suggest a tighter margin for error than many investors realise, so it may be worth reading the 2 key rewards and 1 important warning sign

Gerdau (BOVESPA:GGBR4)

Overview: Gerdau is a Brazilian steel producer that makes long and flat steel products such as rebars, wire rods, structural profiles and special steels for construction, automotive, energy, industrial and mining customers across the Americas, supported by its own iron ore operations in Brazil.

Operations: Gerdau generates most of its revenue from North America at about R$36.4b, followed by Brazil at roughly R$28.5b and South America at around R$5.6b, partly offset by R$1.2b of eliminations.

Market Cap: R$39.4b

Gerdau sits right in the crosshairs of the new US and EU measures on Brazilian steel, with exports now facing higher tariffs and tighter quotas. This comes at a time when its Brazilian business is already under pressure from cheap imports, weak margins and a low current ROE of about 3.2%. The stock also trades on a rich P/E versus local peers and has recently absorbed a R$2.0b one off loss. In addition, it relies entirely on higher risk borrowing to fund its liabilities. Investors also have to weigh insider selling and a relatively new management team against buybacks, dividends and analyst optimism. Overall, Gerdau is a stock that may merit closer scrutiny rather than blind confidence.

Gerdau’s rich P/E multiple, relatively weak 3.2% ROE and reliance on higher risk borrowing could signal additional pressure ahead as tariffs and cheap imports take effect, so it may be worth reviewing the 2 key rewards and 3 important warning signs

Take Control of Your Investment Journey

If Gerdau or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Window Closes?

Fresh ideas can move fast, and the best breakout opportunities often fly under the radar for now. Before momentum is caught by the crowd, consider acting sooner rather than later.

- Spot turnaround potential early by scanning a curated set of smaller companies using the 216 elite penny stocks with strong financials while prices still reflect past doubts, not potential future progress.

- Stay informed on the next infrastructure wave by reviewing hand picked utilities and grid suppliers in the 35 power grid technology and infrastructure stocks while the broader narrative is still developing.

- Follow long term technology shifts by checking companies in the 26 quantum computing stocks before quantum computing headlines begin to attract more widespread trading attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.