Ventas (VTR) Names New Property Chief, Is It Still Below Fair Value?

Ventas, Inc. VTR | 0.00 |

Ventas (VTR) has drawn attention after appointing Andrew L. Wattula as Executive Vice President, Outpatient Medical & Research, and CEO of Lillibridge Healthcare Services, effective August 2026, following the retirement of Peter J. Bulgarelli.

The executive changes around Ventas come as the stock trades at $85.37, with a 1-day share price return of 2.81% and year to date share price return of 10.40%. The 1-year total shareholder return of 38.46% and 3-year total shareholder return of 100.34% point to stronger longer term momentum, despite a softer 30-day share price return of 3.19%.

If this boardroom reshuffle has you thinking about where capital could work next, it may be worth scanning 34 power grid technology and infrastructure stocks

With Ventas trading at $85.37 and flagged as carrying an intrinsic discount alongside a value score of 3, the question is simple: is this still a reasonable entry point, or are investors already paying up for future growth?

Most Popular Narrative: 11.8% Undervalued

The most followed narrative on Ventas pegs fair value at $96.80, above the current $85.37 share price. This sets up a valuation gap investors may want to understand.

Ventas is positioned to benefit from a rapidly growing aging population driving sustained demand for senior housing and healthcare facilities, combined with historically low new construction, supporting multi-year occupancy gains and net operating income (NOI) growth as occupancy rates rise from the low 80% toward the 90%+ level. This is likely to drive substantial operating leverage and margin expansion.

Curious what sits behind that fair value number? The narrative focuses on faster earnings growth, rising margins and a rich future profit multiple. Want to see how those assumptions compare across the full model and time horizon? The detailed breakdown shows exactly which revenue and profit paths are contributing most to that $96.80 figure.

Result: Fair Value of $96.80 (UNDERVALUED)

However, the Ventas story could look very different if competition for senior housing assets pushes acquisition yields lower or if higher labor costs squeeze operating margins.

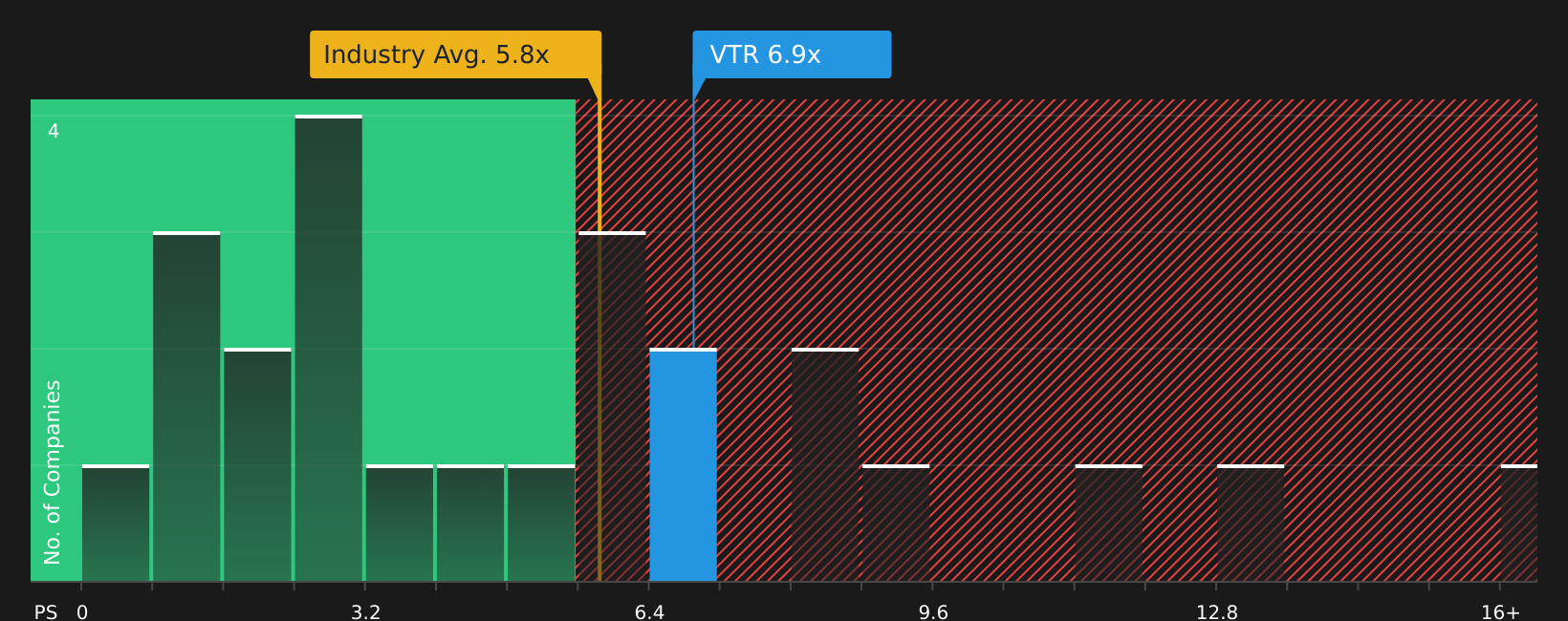

Another View On Ventas: What The Ratios Say

While the SWS DCF model suggests Ventas is trading at a discount to future cash flows, its P/S ratio of 6.8x tells a different story. That is higher than the North American Health Care REITs industry at 5.4x and above the fair ratio of 5.5x, which points to some valuation risk if sentiment cools.

For a closer look at how this stacks up against peers and where the ratio could move, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Ventas attracting both concern and optimism, this is a moment to move quickly, review the full picture, and weigh the trade off yourself with 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Ventas?

If the Ventas narrative has sharpened your focus, now is the moment to widen your watchlist and let high quality stock ideas come to you instead.

- Spot potential turnaround stories early by reviewing 24 elite penny stocks with strong financials that already pair small market caps with stronger financial profiles.

- Target value driven opportunities by scanning 44 high quality undervalued stocks that combine solid cash flows with balance sheet strength.

- Prioritise resilience and sleep better at night by filtering for 67 resilient stocks with low risk scores backed by more stable financial metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.