Ventas (VTR) Stock After Recent Run Does The Price Still Leave Enough Upside

Ventas, Inc. VTR | 0.00 |

- If you are wondering whether Ventas stock still offers value after its recent run, this article focuses squarely on what the current price might be implying about the company.

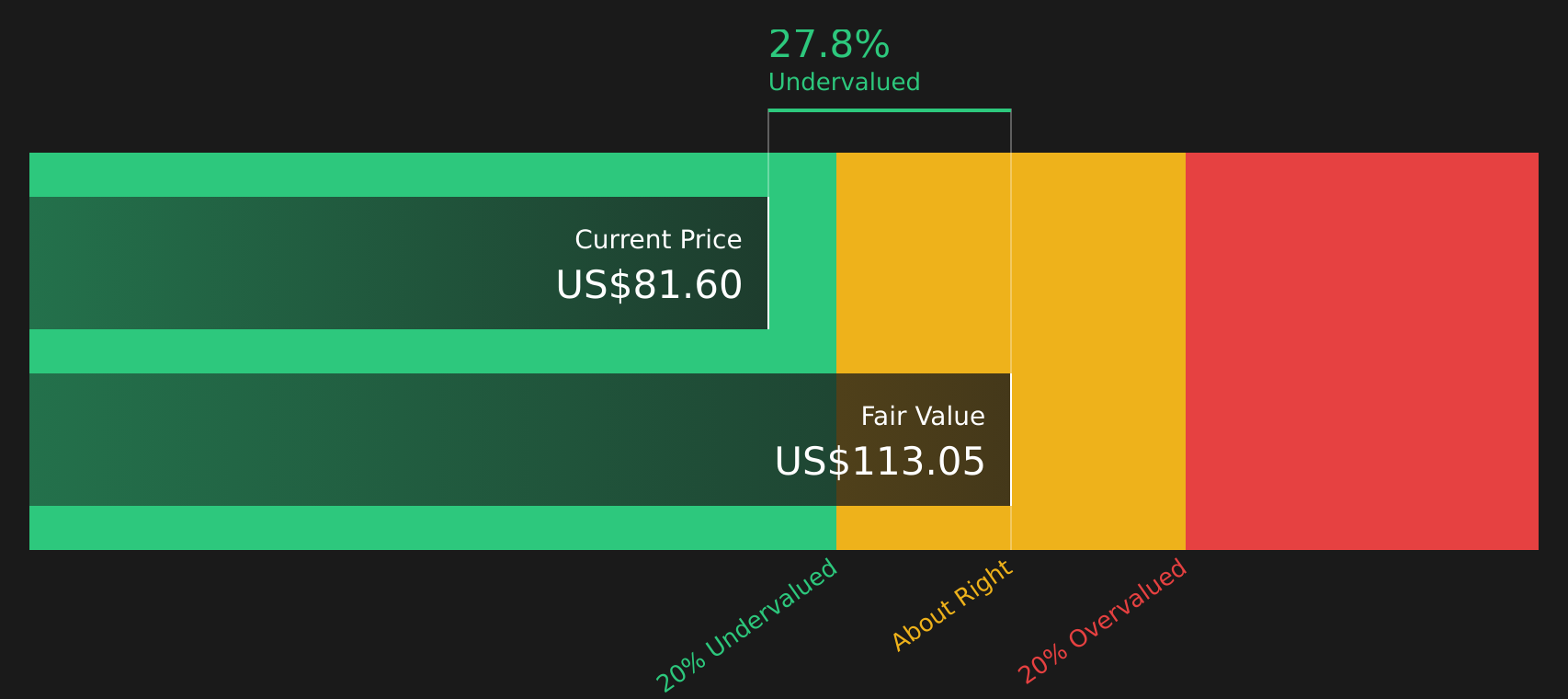

- Ventas shares last closed at US$81.60, with the stock down 2.7% over the past week and 7.6% over the past month, while still showing gains of 5.5% year to date and 33.7% over the past year, and a 102.1% return over three years and 66.7% over five years.

- Recent coverage of Ventas has centered on its position as a large health care REIT. Investors are paying close attention to how interest rate expectations and sector sentiment might be influencing capital flows into listed real estate. This backdrop helps explain why the stock can move meaningfully over shorter periods even when the underlying portfolio changes more gradually.

- On Simply Wall St's 6 point valuation framework, Ventas currently scores 3 out of 6. The rest of this article will walk through the main valuation approaches behind that score and then finish with a way to tie those numbers to a broader company narrative.

Approach 1: Ventas Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model for Ventas takes the company’s adjusted funds from operations, projects those cash flows into the future, then discounts them back to today’s dollars using a required return. The idea is to estimate what the stock could be worth if you owned all those future cash flows.

For Ventas, the latest twelve month free cash flow is about $1.62b. Using a 2 stage Free Cash Flow to Equity model based on adjusted funds from operations, analysts provide explicit forecasts for several years and Simply Wall St extrapolates further out, with projected free cash flow of $2.35b by 2030. Across the 2026 to 2035 period, discounted annual cash flows range from roughly $1.45b to $1.72b, reflecting the combined effect of projected growth and discounting.

When all those discounted cash flows are added together, the model produces an estimated intrinsic value for Ventas of $113.22 per share. Compared with the recent share price of $81.60, the DCF output suggests the stock is about 27.9% undervalued on this set of assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ventas is undervalued by 27.9%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Approach 2: Ventas Price vs Sales

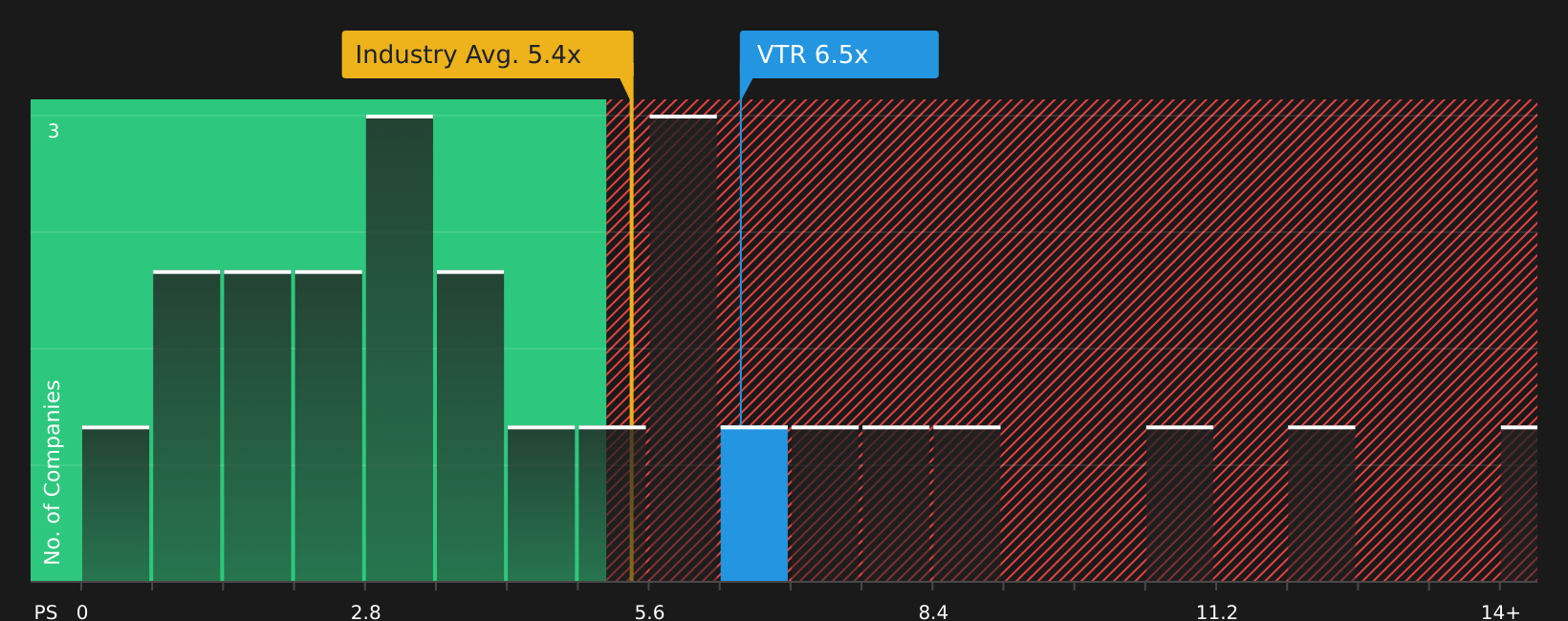

For a large health care REIT like Ventas, the P/S ratio is a useful cross check because it relates the stock price to revenue, which can be more stable than earnings for property companies affected by accounting charges.

In general, higher growth expectations and lower perceived risk can justify a higher “normal” or “fair” sales multiple, while slower expected growth or higher risk tend to support a lower one. Ventas currently trades on a P/S of 6.49x, compared with the Health Care REITs industry average of 6.61x and a peer average of 7.32x, so the stock sits slightly below those broad benchmarks.

Simply Wall St’s proprietary “Fair Ratio” for Ventas is 5.46x. This is the P/S level suggested after weighing factors such as earnings growth estimates, profit margins, industry, market cap and company specific risks. Because it is tailored to the company, this Fair Ratio can be more informative than a simple comparison with peers or the industry. On this basis, Ventas trading at 6.49x versus a Fair Ratio of 5.46x indicates that the stock appears overvalued on the P/S lens.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Ventas Narrative

Earlier it was mentioned that there is an even better way to understand what the current Ventas share price might be implying, and that is through Narratives. These are simple stories you set for the company that link your view on its future revenue, earnings and margins to a forecast. You can then turn that forecast into a fair value and compare it with today’s price to help you decide whether the stock looks attractive or stretched. You can also keep that view updated as fresh information like earnings or news arrives, all within the Narratives tool on Simply Wall St’s Community page. For example, one investor might build a more optimistic Ventas Narrative closer to the US$110 analyst target, while another might prefer a more cautious story nearer US$86, yet both are using the same framework to connect their outlook to the numbers.

Do you think there's more to the story for Ventas? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.