Veralto (VLTO) Margin Improvement To 17.1% Reinforces Quality Earnings Narratives

Veralto Corporation VLTO | 92.32 92.32 | -0.08% 0.00% Pre |

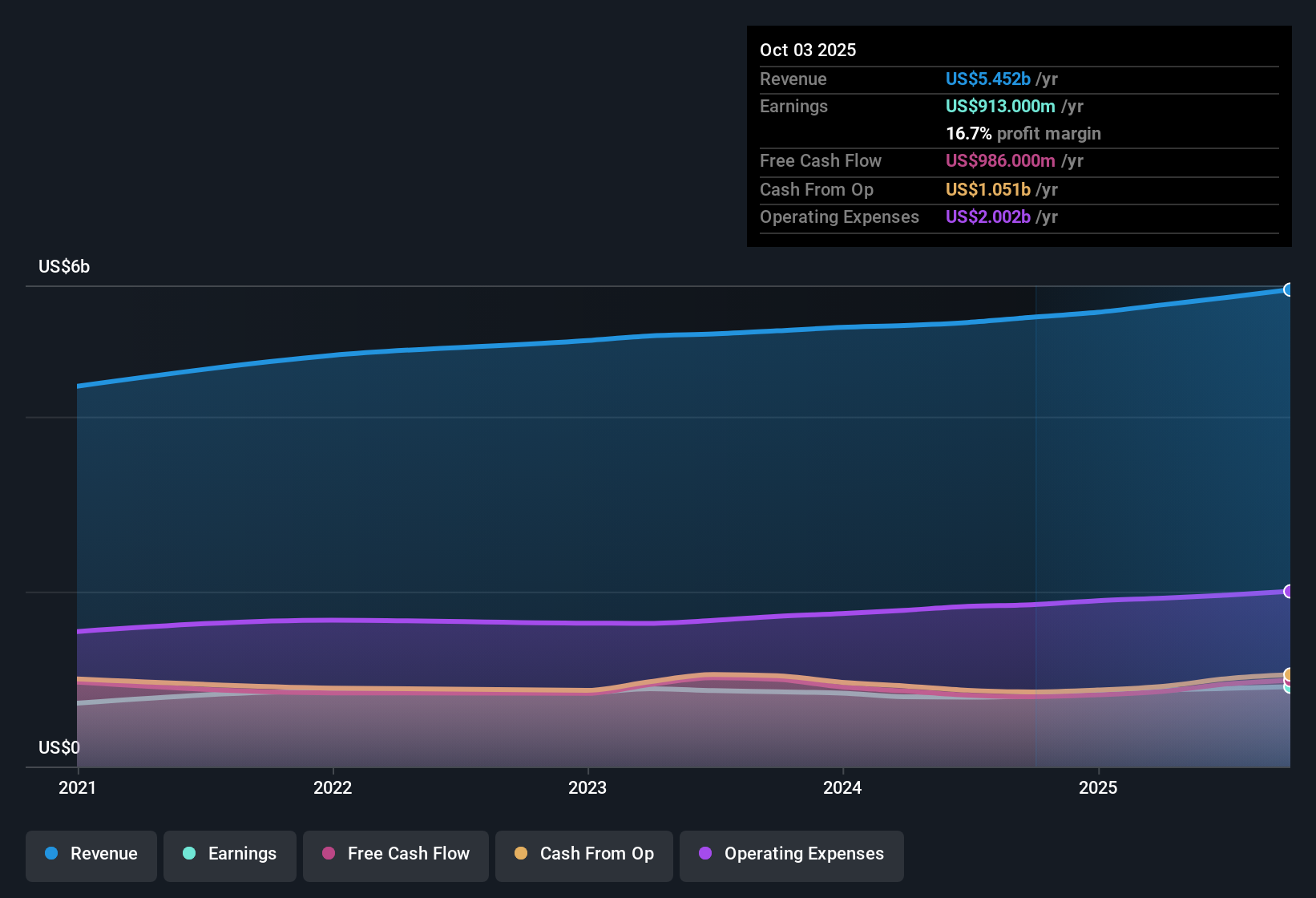

Veralto (VLTO) has wrapped up FY 2025 with fourth quarter revenue of US$1,396 million and basic EPS of US$1.02, capping a year in which trailing twelve month revenue reached US$5.5 billion and EPS came in at US$3.79, alongside reported earnings growth of 12.8% over the past year. Over the last six reported quarters, the company has seen revenue move from US$1,314 million in Q3 2024 to US$1,396 million in Q4 2025. Quarterly EPS ranged between US$0.89 and US$1.02 across that period, giving investors a clearer read on earnings power as margins improved from 16% to 17.1%.

See our full analysis for Veralto.With the latest numbers on the table, the next step is to see how this margin profile and earnings trend line up with the widely held narratives around Veralto and where those stories might need updating.

12.8% earnings growth backed by rising net income

- Across the last six quarters, net income moved from US$219 million in Q3 2024 to US$254 million in Q4 2025. This lines up with the 12.8% earnings growth reported over the past year and gives a clearer sense of how profit has built up behind that headline figure.

- Bullish views that Veralto can keep compounding earnings are partly supported by this trend. However, the forecast 7.3% annual earnings growth is below the 15.6% US market forecast, which means:

- The trailing twelve month net income of US$940 million and EPS of US$3.79 show the business already operating at a solid earnings base, but expectations point to a slower pace than the broader market from here.

- That mix of established profit and more moderate forward growth may appeal to investors who prioritize earnings stability, while those looking for higher growth might see the 7.3% rate as less aggressive than market averages.

Margins at 17.1% with steadier EPS run rate

- Veralto’s trailing net margin sits at 17.1% compared with 16% a year earlier. Over the last six quarters, quarterly EPS moved in a fairly tight band between US$0.89 and US$1.02, which together points to a more consistent profit level relative to revenue.

- Supporters who focus on quality of earnings can point to this margin profile, although it sits alongside only modest revenue growth from US$1,314 million in Q3 2024 to US$1,396 million in Q4 2025, which means:

- The trailing twelve month revenue of US$5.5b and net income of US$940 million indicate that a meaningful share of each sales dollar is reaching the bottom line as profit.

- At the same time, the forecast 5.6% annual revenue growth, which is below the cited 10.1% US market forecast, may lead some investors to question how much further margin improvement can contribute if top line growth stays relatively moderate.

P/E of 24.1x with price below DCF fair value

- Veralto trades on a P/E of 24.1x, which is below both the 26.3x industry average and the 49.2x peer average. At a share price of US$90.79 it also sits under the US$135.92 DCF fair value and a US$111.12 analyst target level cited in the data.

- What is interesting for bullish investors is that these valuation markers line up with recent profit growth, yet revenue and earnings forecasts are slower than the wider US market, which means:

- The shares are shown trading below both the DCF fair value and the analyst target despite the trailing 12.8% earnings growth and 17.1% net margin, which many would see as supportive of the optimistic case on price.

- However, the forecast 7.3% annual earnings growth and 5.6% revenue growth being below market benchmarks gives cautious investors a clear data point to question how much of that valuation gap might realistically close.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Veralto's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Veralto’s forecast 7.3% annual earnings growth and 5.6% revenue growth sit below the referenced US market forecasts, which may leave growth focused investors wanting more.

If that slower outlook feels limiting, use our CTA_SCREENER_LARGE_CAP_HIGH_GROWTH_POTENTIAL to quickly focus on larger companies that analysts expect to have stronger earnings expansion.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.