Vericel (VCEL) Could Be 33% Undervalued After Insider Sales Raised Fresh Questions

Vericel Corporation VCEL | 0.00 |

Vericel (VCEL) is in focus after several senior executives exercised stock options and sold shares in late June under pre-arranged Rule 10b5-1 trading plans, drawing attention to insider activity at the company.

Against this insider activity backdrop, Vericel’s share price has climbed to $46.98, with a 1-day share price return of 4.05% and a 30-day share price return of 31.63%. The 1-year total shareholder return of 12.55% and 5-year total shareholder return decline of 11.46% show stronger recent momentum compared with its longer run.

If you are weighing how Vericel fits alongside other opportunities in the healthcare space, it could be worth scanning 40 healthcare AI stocks. This screener can highlight additional stocks where AI intersects with medicine and biotech.

With Vericel’s share price near $47 after strong short term returns and a modest discount to the current analyst price target, the key question is whether the recent run still leaves upside or if the market already reflects future growth.

Most Popular Narrative: 32.9% Undervalued

Vericel’s most followed narrative points to a fair value of $70.00 per share compared with the last close at $46.98, which is a sizeable gap investors will want to understand.

Burn Care, with 17 territories now cross selling Epicel and NexoBrid, plus a potential BARDA stockpiling award, gives Vericel a second franchise with recurring and contract based revenue that can smooth cash generation and support free cash flow beyond the current US$52 million operating cash flow run rate.

Want to see what underpins that change from today’s earnings base to a much larger profit pool on a higher future multiple and richer margins? The core narrative focuses on faster earnings growth than revenue, expanding profitability, and a valuation framework that assumes investors will continue to value those future cash flows accordingly. Interested in how those elements combine into a $70.00 fair value and where the model is most sensitive?

Result: Fair Value of $70.00 (UNDERVALUED)

However, Vericel’s story also depends on MACI maintaining procedure growth, and on Burn Care contracts like BARDA awards avoiding delays or smaller than expected volumes.

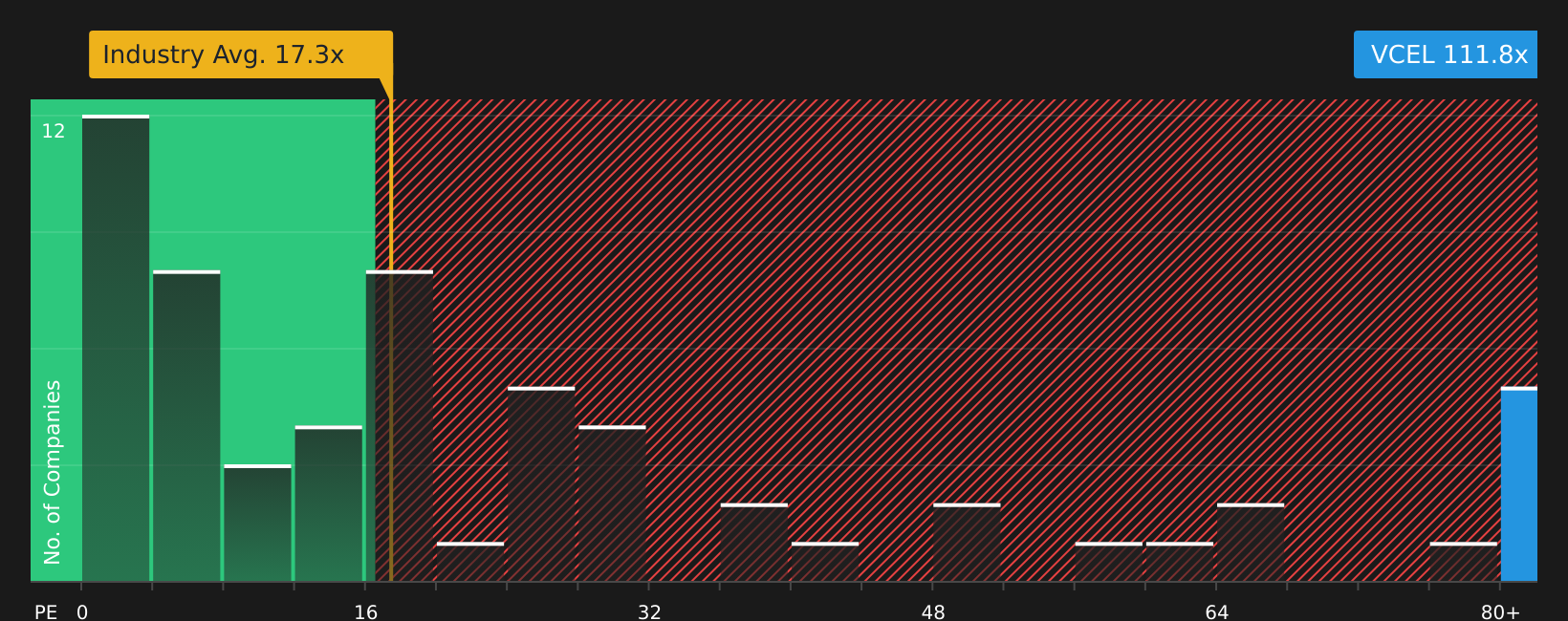

Another View: Vericel Looks Expensive On Earnings

That $70.00 narrative based fair value for Vericel sits awkwardly next to the current P/E of 111.8x, compared with 17.3x for the US Biotechs industry, 17x for peers, and a 29x fair ratio. That gap points to valuation risk investors should weigh carefully.

So if the stock already trades well above what the fair ratio implies, is the premium simply too far ahead of itself, or is the market correctly pricing in years of strong execution? See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and concern around Vericel seems finely balanced, consider reviewing the same data now and weighing the 2 key rewards and 1 important warning sign

Looking For More Investment Ideas Beyond Vericel?

If Vericel has sharpened your focus on opportunities, do not stop here; use the Simply Wall Street Screener to surface other stocks that might suit your portfolio.

- Target potential mispricing by scanning 44 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial profile.

- Prioritize resilience by reviewing 74 resilient stocks with low risk scores designed to highlight companies with steadier risk profiles for more defensive positioning.

- Spot underfollowed opportunities by checking the screener containing 18 high quality undiscovered gems that show strong fundamentals yet attract relatively little attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.