Vericel (VCEL) Stock Could Be 37.3% Undervalued After Earnings Beat And Fund Buying

Vericel Corporation VCEL | 0.00 |

Vericel (VCEL) has drawn fresh attention after institutional holders such as BlackRock and State Street lifted their positions, and the company reported quarterly earnings per share that came in above market expectations.

Vericel's share price has picked up momentum recently, with a 1-day share price return of 2.48%, 7-day return of 7.05%, and 90-day return of 23.57%. This comes even though the 1-year total shareholder return declined 4.57% and the 5-year total shareholder return fell 40.5%.

If Vericel's recent move has you rethinking growth ideas in healthcare, this could be a good moment to see what else is out there via our screener of 40 healthcare AI stocks

With institutional holders leaning in, earnings per share ahead of expectations and Vericel trading below the average analyst price target, is this a genuine mispricing or is the market already accounting for future growth?

Most Popular Narrative: 37.3% Undervalued

On the most followed narrative, Vericel's fair value of $64.00 sits well above the last close at $40.10, setting up a bullishly skewed story.

Planned MACI expansion outside the U.S., starting with a targeted U.K. launch and an addressable MACI Ankle market estimated at more than US$1b, introduces additional revenue streams that can scale on top of an already profitable base and support long term earnings growth.

Curious what underpins that $64.00 fair value for Vericel? The narrative leans on expectations for faster earnings growth, higher margins and a richer future earnings multiple. The exact mix of those assumptions may surprise you.

Result: Fair Value of $64.00 (UNDERVALUED)

However, the bullish Vericel case still hinges on MACI maintaining pricing and surgeon uptake, and on Burn Care contracts such as potential BARDA stockpiling materializing as hoped.

Another View on Vericel's Valuation

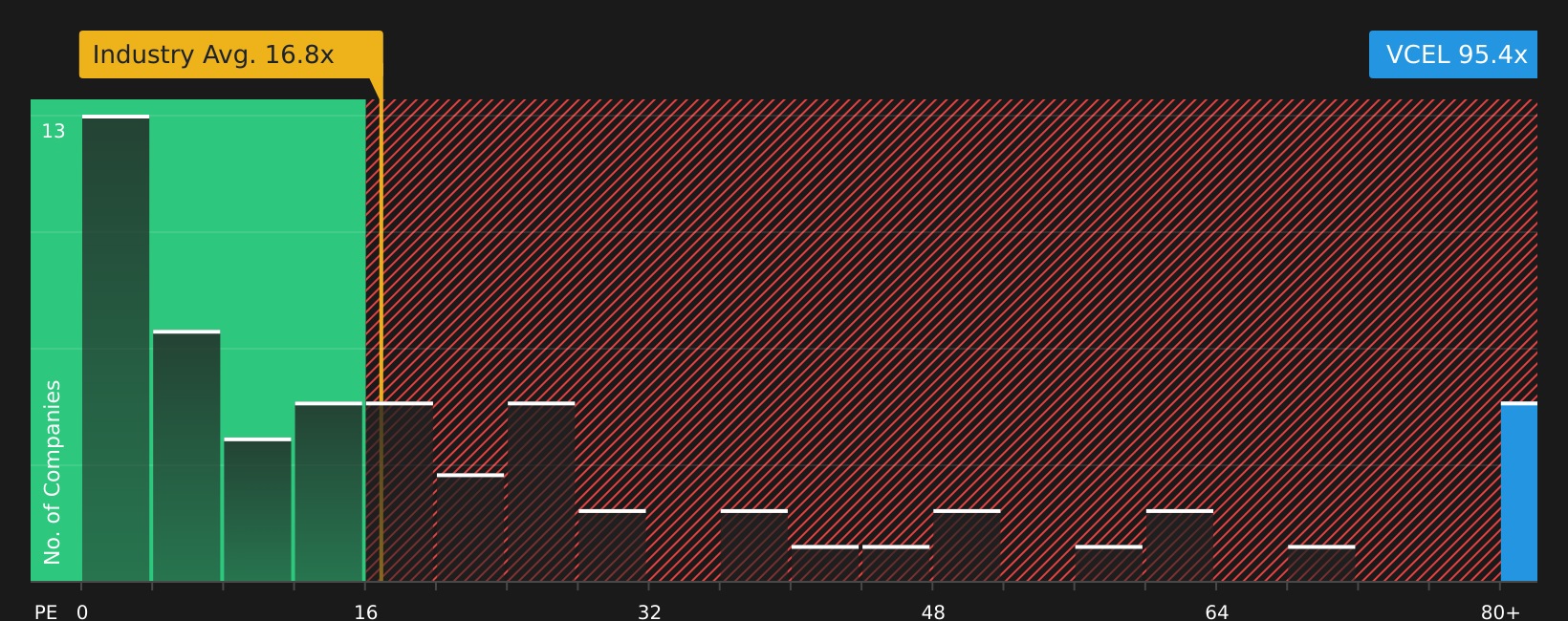

The bullish narrative frames Vericel as undervalued at a fair value of $64.00, but the current P/E of 95.4x tells a different story. That is far above both the peer average of 14.3x and a fair ratio of 27.5x. This points to meaningful valuation risk if sentiment cools.

If you lean on earnings multiples rather than narratives, this kind of gap can matter a lot for your risk tolerance, especially when the market has alternatives priced closer to their fair ratio. How comfortable are you paying such a premium for Vericel today?

Next Steps

Given the mixed signals around Vericel, the real question is how you weigh the upside story against the concerns on the table. Move quickly and review the data in detail to make up your own mind using the 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Vericel?

If Vericel has sharpened your focus on valuation, consider your next move carefully by lining up fresh stock ideas with solid fundamentals, income potential and controlled risk.

- Target potential bargains early by reviewing the screener containing 19 high quality undiscovered gems before other investors spot them.

- Strengthen your core holdings by scanning the solid balance sheet and fundamentals stocks screener (48 results) for companies with sturdier financial foundations.

- Dial back volatility pressure by focusing on the 65 resilient stocks with low risk scores and keeping your watchlist aligned with your risk comfort zone.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.