Vishay Intertechnology (VSH) Valuation Check After Silicon Carbide Power Module Rollout

Vishay Intertechnology, Inc. VSH | 0.00 |

Vishay Intertechnology (VSH) has rolled out a series of new silicon carbide MOSFET power modules and Trench MOS Barrier Schottky rectifier modules, targeting higher efficiency in automotive, energy, industrial, and telecom power systems.

The recent product launches have arrived alongside a sharp shift in sentiment, with Vishay Intertechnology’s 30 day share price return of 35.19% and 1 year total shareholder return of 30.51% contrasting with a weaker 3 year total shareholder return decline of 8.02%.

If these new silicon carbide and rectifier modules have caught your attention, it could be a good moment to widen your search across high growth tech and AI stocks as you look for other potential ideas in the sector.

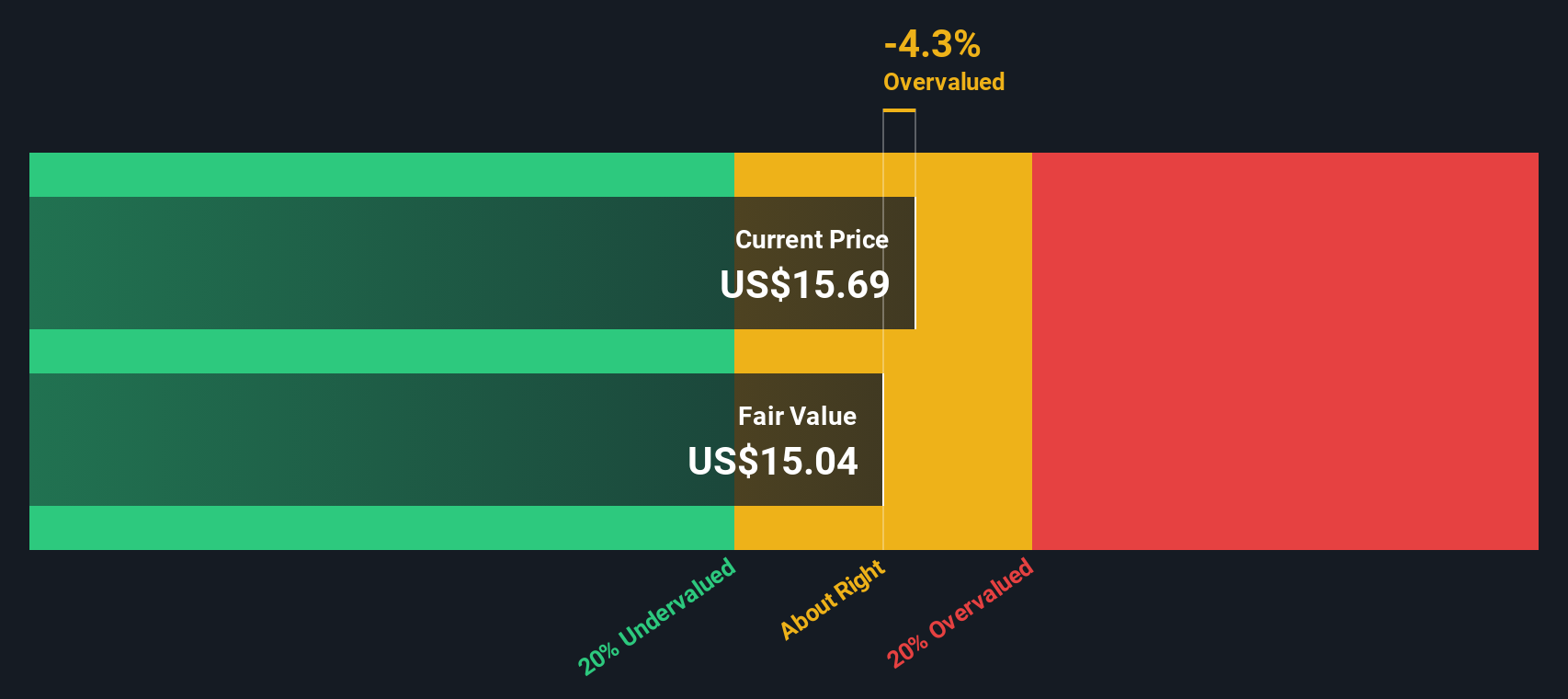

With Vishay shares up 35.2% over 30 days and trading above the US$15 analyst price target at US$20.67, investors may question whether there is still value available or whether the market is already pricing in future growth.

Most Popular Narrative: 37.8% Overvalued

With Vishay Intertechnology last closing at $20.67 against a most-followed fair value estimate of $15, the current share price sits well above that narrative anchor, putting extra attention on the assumptions behind it.

Ongoing innovation and commercialization in advanced technologies (e.g., silicon carbide MOSFETs and diodes) and deeper cross-selling initiatives are leading to an expanding bill-of-materials footprint with key customers in automotive, industrial, and AI, likely boosting average selling prices, product mix, and ultimately net margins.

Curious what kind of revenue path and margin lift are baked into that fair value, and how a lower future earnings multiple still supports it? The most followed narrative ties together top line growth, margin expansion and a specific discount rate to explain why $15 per share can be justified despite a richer starting point today.

Result: Fair Value of $15 (OVERVALUED)

However, there are still clear pressure points, including recent losses on roughly US$3.0b of revenue and ongoing heavy capex with negative free cash flow guidance that could challenge this upbeat script.

Another View: Sales Multiple Sends a Different Signal

Our DCF model flags Vishay Intertechnology as overvalued, with the current $20.67 share price sitting above an estimated future cash flow value of $6.89. Yet on a simple P/S of 0.9x, the stock screens cheaper than peers at 2.9x and a fair ratio of 1x. This raises the question of whether the cash flow model overstates execution risk or the sales-based view is too generous about future margins.

Build Your Own Vishay Intertechnology Narrative

If you see the numbers differently or simply want to stress test the assumptions yourself, you can build and adjust your own Vishay story in just a few minutes: Do it your way.

A great starting point for your Vishay Intertechnology research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Vishay has you thinking more broadly about opportunities, do not stop here. Widen your search now so you do not miss your next strong idea.

- Spot emerging growth stories early by checking out these 3542 penny stocks with strong financials that already pair smaller market caps with more resilient financial profiles.

- Ride the AI momentum more thoughtfully by scanning these 24 AI penny stocks that are already filtered for this theme instead of scrolling through tickers one by one.

- Put value front and center by reviewing these 876 undervalued stocks based on cash flows where prices are compared directly with estimated cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.