Waters (WAT) Stock Weighs Rich P/E Against DCF Value After Recent Gains

Waters Corporation WAT | 0.00 |

- If you are wondering whether Waters is priced fairly or if the stock leans more toward opportunity or caution, this article walks through the key valuation checks that may matter most to you.

- Waters recently closed at US$369.18, with returns of 3.4% over the last week, 7.8% over the last month, a decline of 3.3% year to date, and a 5.5% gain over the past year. This provides useful context before considering what the current price might imply.

- Recent coverage has described Waters as a mature life sciences tools company, with attention on how it is positioned in its core analytical instruments markets and how that positioning compares with investor expectations on quality and defensiveness. These themes help explain why the stock has seen mixed shorter term and longer term returns as investors weigh perceived resilience against price.

- On Simply Wall St's 6 point valuation checklist, Waters scores 2 out of 6. The next sections will break down what different valuation methods indicate about that score and, at the end, highlight a broader way to think about valuation that goes beyond a single number.

Waters scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

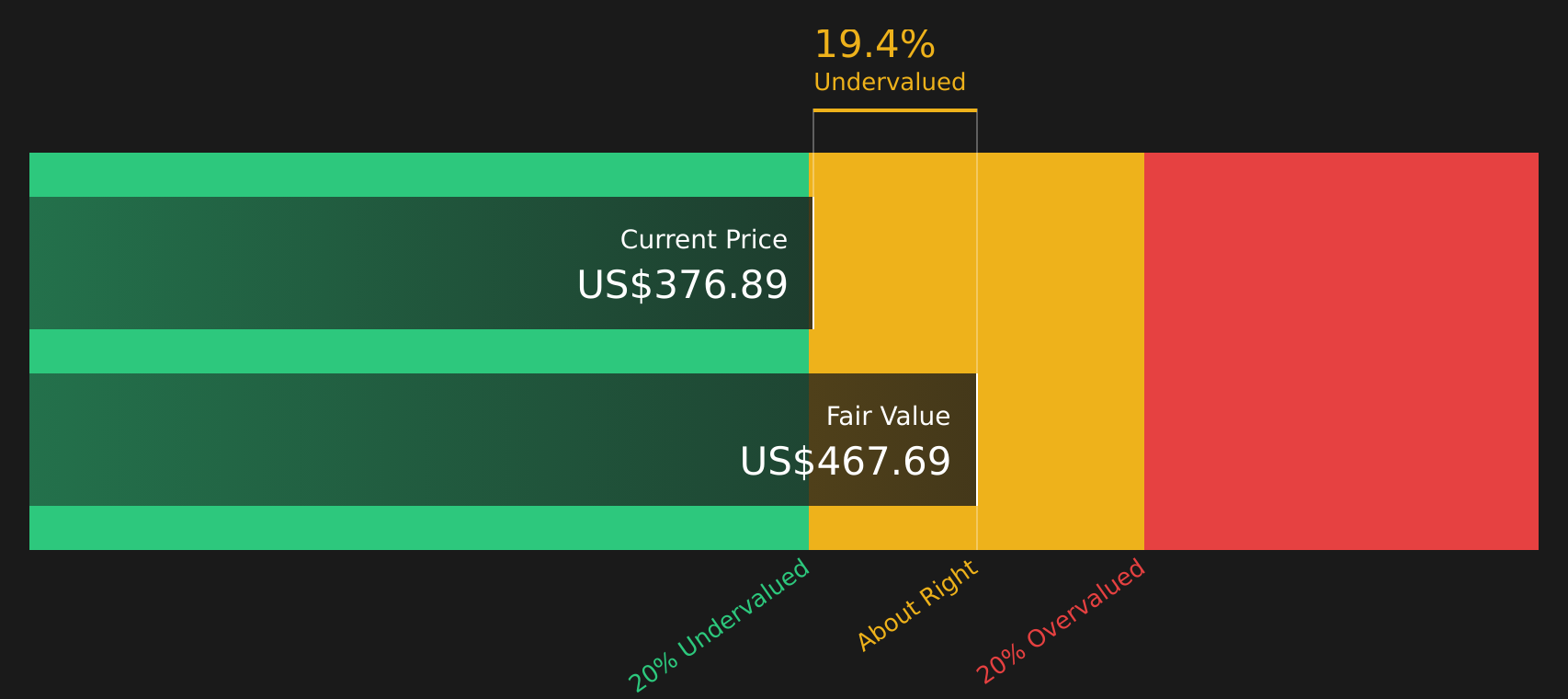

Approach 1: Waters Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what Waters stock could be worth by projecting future cash flows and discounting them back to today's dollars. It focuses on the cash the company is expected to generate for shareholders rather than reported earnings.

For Waters, Simply Wall St applies a 2 Stage Free Cash Flow to Equity model using current and projected Free Cash Flow in $. The latest twelve month Free Cash Flow is about $226.1 million. Analyst estimates and extrapolations point to Free Cash Flow reaching $1.90 billion by 2029, with a series of annual projections in between that are discounted back to reflect time and risk.

When all projected and extrapolated cash flows are added and discounted, the model arrives at an estimated intrinsic value of about $469.16 per share. Compared with the recent share price of $369.18, this implies the stock trades at roughly a 21.3% discount to that DCF estimate, which in this model suggests Waters is undervalued on this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Waters is undervalued by 21.3%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: Waters Price vs Earnings (P/E)

For profitable companies like Waters, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. A higher P/E usually reflects higher growth expectations or a perception of lower risk, while a lower P/E often points to more modest growth expectations or higher perceived risk.

Waters currently trades on a P/E of 80.62x. This is well above the Life Sciences industry average P/E of 34.47x and above the peer group average of 31.01x. On these simple comparisons, the stock carries a materially higher earnings multiple than many peers.

Simply Wall St also calculates a Fair Ratio for Waters of 30.30x. This proprietary metric estimates what a more appropriate P/E might be after considering factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it adjusts for these elements, the Fair Ratio aims to be more tailored than a basic peer or industry comparison.

Comparing Waters actual P/E of 80.62x with the Fair Ratio of 30.30x suggests the stock trades at a substantially higher multiple than this model implies.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Waters Narrative

Earlier it was mentioned that there is an even better way to think about valuation, and on Simply Wall St this comes through Narratives, where you set out your story for Waters, connect that story to specific forecasts for revenue, earnings and margins, and let the platform turn it into a Fair Value that you can compare with the current share price.

A Narrative is simply your structured view of a company, written in plain language and backed by numbers. Instead of only looking at a P/E or DCF output, you link Waters product launches, acquisitions and risks to concrete forecasts and see what price those assumptions support.

On the Simply Wall St Community page, Narratives are available as an easy tool used by millions of investors. They update automatically when new information such as earnings, product news or guidance is added, so your Fair Value view stays aligned with the latest data without extra effort.

For Waters, one investor Narrative might lean toward the higher Fair Value of about US$460.00 with stronger growth and margins, while another might sit closer to the lower Fair Value of about US$330.00 with more cautious assumptions. Comparing those Fair Values with the current price can help you decide where Waters fits in your own investment framework.

For Waters however we will make it really easy for you with previews of two leading Waters Narratives:

Fair Value: US$460.00

Implied discount to this Fair Value vs the recent price of US$369.18: about 19.7%.

Revenue growth assumption: 30.76%.

- Bullish analysts see rapid adoption of Waters newer instruments, consumables and workflow solutions, supported by acquisitions such as BD's Biosciences and Diagnostic Solutions segment. They see these factors feeding into higher revenue and margin potential than current consensus.

- The optimistic view expects profit margins to improve from 11.9% to 17.0% over three years, earnings to reach about US$1.4b by 2029, and the stock to trade on a future P/E of 49.0x, with an 8.2% discount rate used to bring those expectations back to today.

- Key risks include dependence on chromatography and mass spectrometry systems, slower progress in software and digital solutions relative to peers, pricing pressure on instruments, and exposure to funding cycles, supply chain issues and trade or geopolitical uncertainty.

Fair Value: US$330.00

Implied premium to this Fair Value vs the recent price of US$369.18: about 11.9%.

Revenue growth assumption: 34.13%.

- Bearish analysts focus on Waters reliance on mature product lines, customer budget constraints in pharma and research, and exposure to emerging market volatility. Together these factors could limit pricing power and keep revenue growth and margins in check.

- This more cautious view assumes revenue growth of 34.13% a year but with margin compression from 20.3% to 18.4% by 2029, earnings of about US$1.4b, and a future P/E of 35.5x, discounted at 7.91% to reach a Fair Value of US$330.00.

- Concerns include integration risk around the BD Biosciences and Diagnostic Solutions acquisition, possible margin pressure from lower margin assets and tariffs, ongoing weakness in certain divisions and the chance that current recurring revenue drivers and replacement cycles prove temporary.

These contrasting Waters Narratives show how the same company facts can support very different Fair Values. This is why it is useful to compare each set of assumptions with your own expectations rather than relying on a single headline number.

To see each view in full and stress test your own assumptions against both sides of the argument, start with these narrative previews, then read through the complete bull and bear write ups and decide which better matches how you see Waters over the next several years, or whether your view sits somewhere in between the two.

Do you think there's more to the story for Waters? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.