Weaker Outlook And AI Concerns Could Be A Game Changer For Gartner (IT)

Gartner, Inc. IT | 0.00 |

- In late February 2026, Gartner reported a weak quarter with a revenue drop in its Consulting segment, issued softer 2026 guidance, and subsequently faced multiple law firm investigations into its use of non-GAAP financial measures and earnings guidance practices.

- The news also intensified concerns that generative AI could erode demand for Gartner’s traditional research and advisory model, with critics arguing new AI tools may substitute some of the “middleman” insight Gartner has long provided to enterprise clients.

- We’ll now examine how Gartner’s weaker outlook and the scrutiny of its financial disclosures may influence the previously positive investment narrative.

AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Gartner Investment Narrative Recap

To own Gartner today, you have to believe its research, advisory, and emerging AI tools will remain essential despite cheaper digital and AI alternatives. The key near term catalyst is whether contract value can reaccelerate after weaker 2026 guidance, while the biggest risk is that generative AI and cost conscious clients increasingly bypass Gartner. The latest quarter, with a sharp Consulting revenue decline and tighter guidance, directly pressures both that catalyst and that risk.

One recent development that stands out against this backdrop is the series of law firm investigations into Gartner’s use of non GAAP financial measures and earnings guidance. For investors, this matters less for any legal outcome and more because it raises questions about how management presents growth, margins, and EPS in a period when the core business is already under pressure from AI disruption and softer 2026 expectations.

Yet, even as bullish analysts once expected earnings of about US$955.6 million by 2028, the combination of weak guidance and mounting AI competition means investors should now pay close attention to...

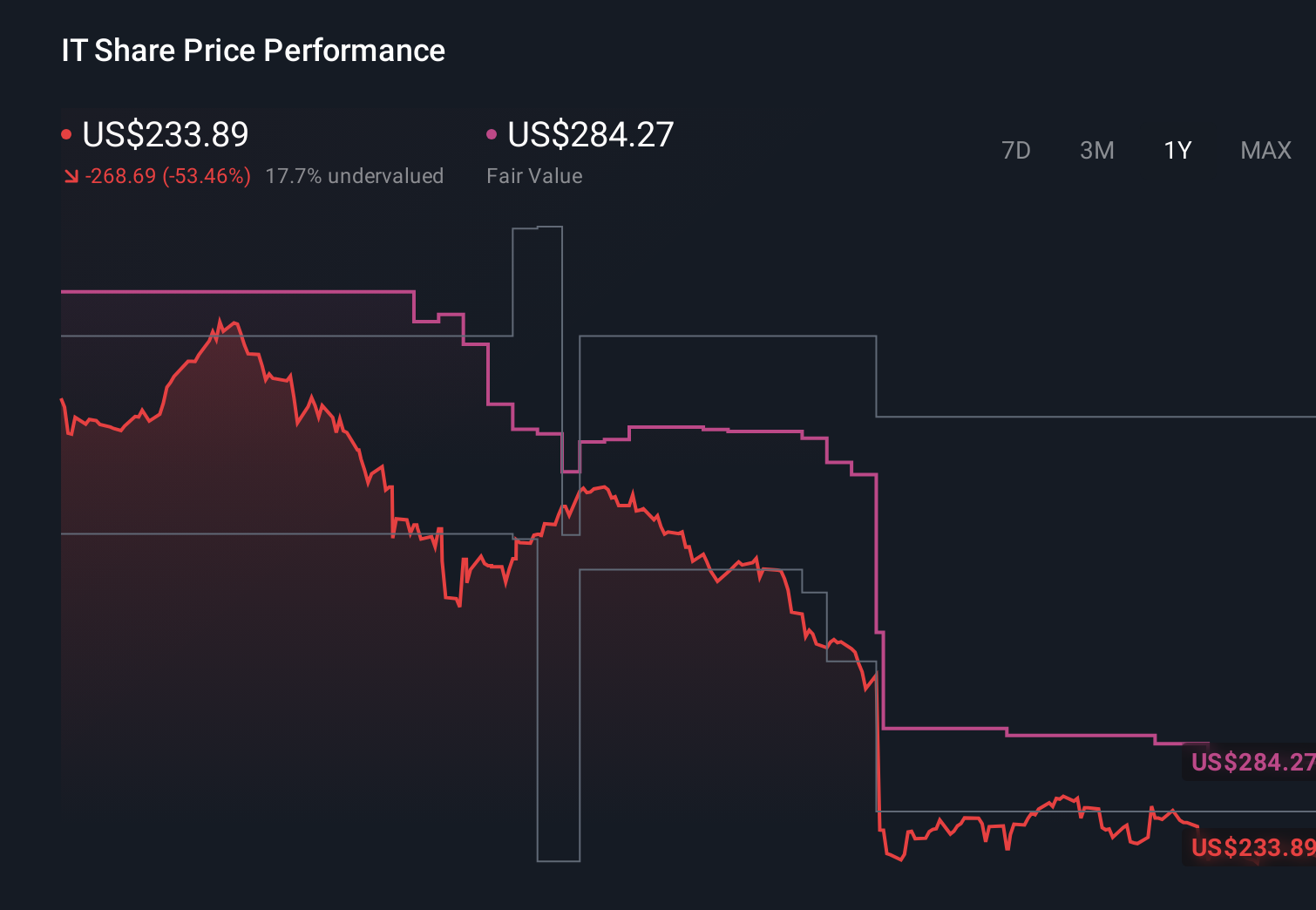

Gartner's narrative projects $7.4 billion revenue and $821.8 million earnings by 2028.

Uncover how Gartner's forecasts yield a $283.73 fair value, a 82% upside to its current price.

Exploring Other Perspectives

Before this earnings shock, the most optimistic analysts were assuming Gartner could still grow revenue to about US$7.7 billion by 2028, leaning on AI driven upsell and stronger pricing power, even as cheaper digital tools threatened retention and margins. Compared with the baseline view, that is a far more upbeat story, and this quarter’s miss and rising AI concerns may prompt you to reassess which narrative feels more realistic for your own expectations.

Explore 4 other fair value estimates on Gartner - why the stock might be worth just $190.46!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Gartner research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gartner research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gartner's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.