نحن نراقب عن كثب معدل استنزاف السيولة النقدية لشركة Pixelworks (NASDAQ:PXLW)

Pixelworks, Inc. PXLW | 0.00 |

يمكننا بسهولة فهم سبب انجذاب المستثمرين إلى الشركات غير الربحية. على سبيل المثال، رغم تكبّد أمازون خسائر لسنوات عديدة بعد إدراجها في البورصة، إلا أن من اشترى أسهمها واحتفظ بها منذ عام ١٩٩٩، لكان قد جنى ثروة طائلة. ولكن بينما يُخلّد التاريخ تلك النجاحات النادرة، غالبًا ما تُنسى الشركات الفاشلة؛ فمن يتذكر موقع Pets.com؟

نظراً لهذا الخطر، رأينا أن نلقي نظرة على ما إذا كان ينبغي على مساهمي شركة Pixelworks ( NASDAQ:PXLW ) القلق بشأن استنزافها للنقد. لأغراض هذه المقالة، سنعرّف استنزاف النقد بأنه مقدار النقد الذي تنفقه الشركة سنوياً لتمويل نموها (ويُسمى أيضاً التدفق النقدي الحر السلبي). سنبدأ بمقارنة استنزاف النقد باحتياطياتها النقدية لحساب مدة كفاية السيولة لديها.

متى قد تنفد أموال شركة Pixelworks؟

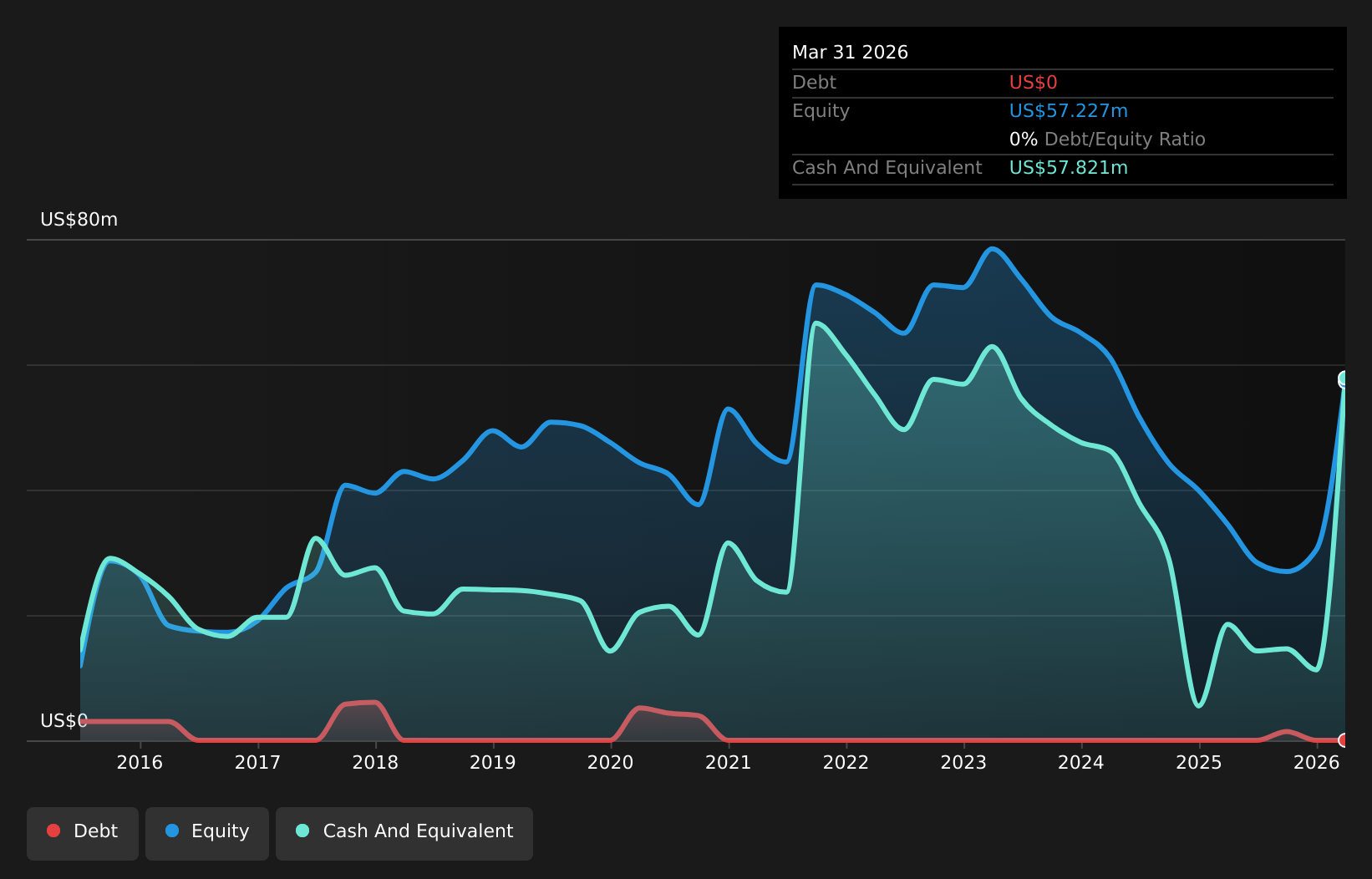

يُقصد بفترة كفاية السيولة النقدية للشركة المدة الزمنية اللازمة لاستنفاد احتياطياتها النقدية بالمعدل الحالي لاستهلاكها. في مارس 2026، كان لدى شركة Pixelworks سيولة نقدية بقيمة 58 مليون دولار أمريكي، وكانت خالية من الديون. خلال العام الماضي، بلغ استهلاكها النقدي 16 مليون دولار أمريكي. هذا يعني أن فترة كفاية السيولة النقدية لديها كانت حوالي 3.6 سنوات اعتبارًا من مارس 2026. تتيح هذه الفترة للشركة الوقت والمساحة اللازمين لتطوير أعمالها. يمكنك الاطلاع على كيفية تغير رصيدها النقدي بمرور الوقت في الصورة أدناه.

ما مدى نمو شركة Pixelworks؟

نرى أن نجاح شركة Pixelworks في خفض استنزافها النقدي بنسبة 45% خلال العام الماضي أمرٌ مُشجع. لكنّنا نشعر بالقلق إزاء الانخفاض الحاد في إيراداتها التشغيلية بنسبة 97% خلال الفترة نفسها. وبالنظر إلى هذين المؤشرين، يساورنا بعض القلق بشأن مسار تطور الشركة. مع ذلك، يبقى العامل الحاسم هو قدرة الشركة على تنمية أعمالها مستقبلاً. لذا، قد ترغب في إلقاء نظرة على معدل النمو المتوقع للشركة خلال السنوات القليلة المقبلة .

ما مدى صعوبة حصول شركة Pixelworks على المزيد من الأموال اللازمة للنمو؟

يبدو أن شركة Pixelworks في وضع جيد نسبيًا من حيث استنزاف السيولة، لكننا نعتقد أنه من المفيد النظر في مدى سهولة حصولها على تمويل إضافي إذا رغبت في ذلك. يُعد إصدار أسهم جديدة أو الاقتراض من أكثر الطرق شيوعًا للشركات المدرجة لجمع المزيد من الأموال لأعمالها. تلجأ العديد من الشركات إلى إصدار أسهم جديدة لتمويل نموها المستقبلي. يمكننا مقارنة استنزاف السيولة للشركة برأسمالها السوقي لنفهم عدد الأسهم الجديدة التي سيتعين على الشركة إصدارها لتمويل عملياتها لمدة عام واحد.

يُمثل استنزاف شركة Pixelworks للنقد، والبالغ 16 مليون دولار أمريكي، حوالي 37% من قيمتها السوقية البالغة 44 مليون دولار أمريكي. وهذا ليس مبلغًا زهيدًا، وإذا اضطرت الشركة لبيع ما يكفي من الأسهم لتمويل نمو عام آخر بالسعر الحالي للسهم، فمن المرجح أن نشهد تخفيفًا كبيرًا في قيمة الأسهم.

هل يُعدّ استنزاف أموال شركة Pixelworks مصدر قلق؟

على الرغم من أن انخفاض إيراداتها يُثير قلقنا بعض الشيء، إلا أننا نرى أن وضع السيولة النقدية لشركة Pixelworks واعدٌ نسبيًا. لا نعتقد أن استنزافها النقدي يُشكل مشكلةً كبيرة، ولكن بعد دراسة مجموعة العوامل المذكورة في هذا المقال، نرى أنه من الضروري أن يُراقب المساهمون كيفية تغيره بمرور الوقت.

بالتأكيد، قد تجد فرصة استثمارية رائعة بالبحث في أماكن أخرى. لذا، ألقِ نظرة على هذه القائمة المجانية للشركات التي يمتلك فيها المطلعون حصصًا كبيرة، وهذه القائمة لأسهم النمو (وفقًا لتوقعات المحللين).

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.