Western Midstream Partners (WES) Prices $700 Million Notes, Is The Valuation Upside Already Priced In?

Western Midstream Partners, LP WES | 0.00 |

Western Midstream Partners (WES) has come into focus after its subsidiary priced a $700 million senior notes offering, as investors weigh what this means for the partnership’s leverage profile and upcoming capital spending.

Western Midstream Partners’ share price has eased over the past month, with a 30 day share price return of a 5.77% decline, even as the 1 year total shareholder return of 22% and 5 year total shareholder return of 198.63% point to stronger long term momentum.

If this financing move has you thinking about where else capital intensive themes could lead, it may be worth scanning opportunities in 34 power grid technology and infrastructure stocks

With Western Midstream Partners trading at $42.78, sitting at a small 6% discount to the average analyst price target and carrying an implied 35% intrinsic discount, investors have to ask: is this a genuine mispricing, or is the market already baking in future growth?

Most Popular Narrative: 4.4% Undervalued

On the most followed narrative, Western Midstream Partners screens as modestly undervalued, with a fair value of $44.73 against the recent $42.78 unit price. That gap rests on some clear operating assumptions.

Investment in major long term capacity expansions, such as the Pathfinder pipeline and North Loving II plant, are set to come online in 2027, adding significant processing and transport capability, and expected to materially increase revenues and cash flows in subsequent years.

Read the complete narrative. Read the complete narrative.

Want to see what underpins that valuation gap? The narrative leans on steady volume growth, richer margins, and a future earnings multiple that assumes the cash generation story holds together.

Result: Fair Value of $44.73 (UNDERVALUED)

However, the Western Midstream Partners valuation story still hinges on capital heavy projects paying off and on producers keeping volumes flowing through its systems.

Another Take On Western Midstream Partners' Valuation

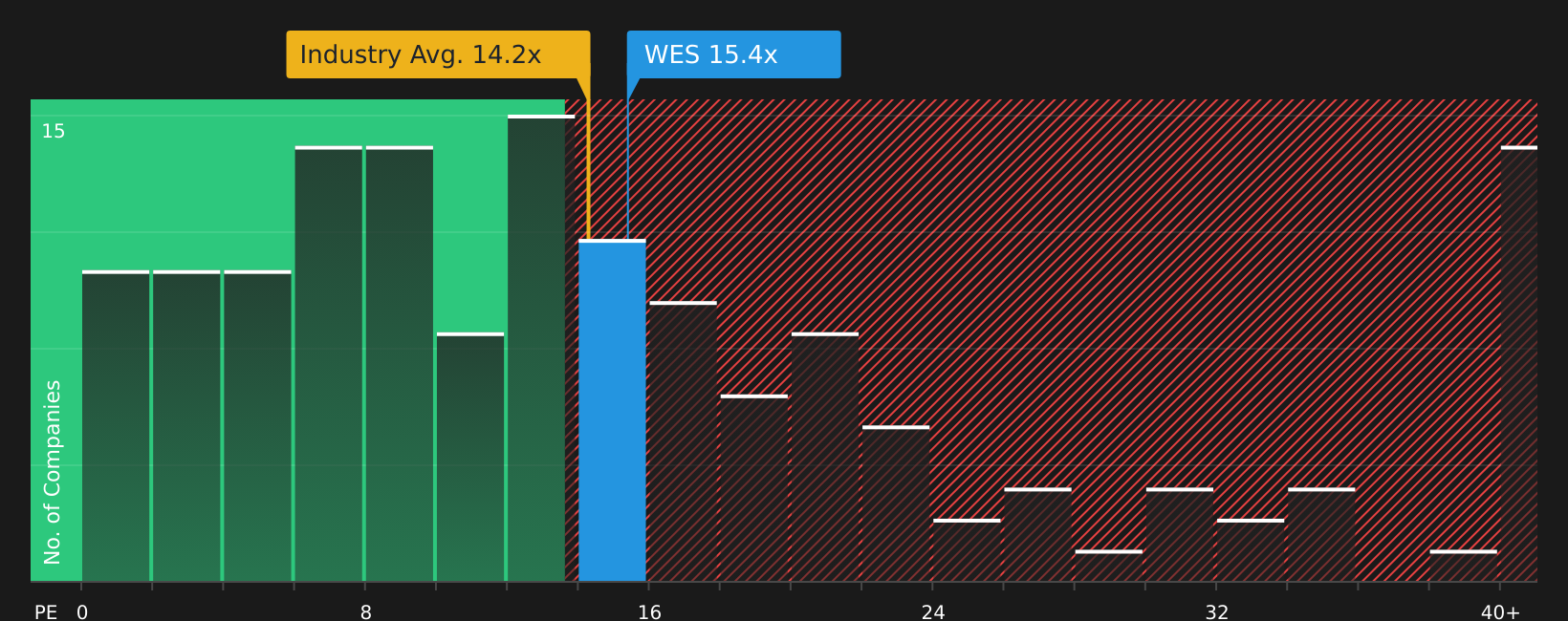

The earlier narrative leans on cash flow and growth assumptions to argue Western Midstream Partners is modestly undervalued, but the earnings multiple tells a tighter story. At a P/E of 14.1x, WES trades above the US Oil and Gas industry at 12.9x, yet below peers at 22.1x and a fair ratio of 21.3x. This points to meaningful re rating risk or headroom, depending on how earnings evolve.

Those gaps suggest the market is pricing Western Midstream Partners more cautiously than its peer set, even though the fair ratio implies room for the P/E to move higher over time. The question is whether this represents a margin of safety or a signal that expectations are already full.

Next Steps

With mixed sentiment around Western Midstream Partners in this article, now is a good time to look at the underlying data yourself and decide where you stand. To weigh both sides of the story, start with a clear view of the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Western Midstream Partners?

If Western Midstream Partners has sharpened your thinking, do not stop here. A wider watchlist can help you spot different types of opportunities and risks earlier.

- Spot potential mispricings early by reviewing companies flagged in 43 high quality undervalued stocks and compare their fundamentals before others pay attention.

- Strengthen your focus on resilience by checking out businesses in the 67 resilient stocks with low risk scores that score well on stability and risk measures.

- Get ahead of the crowd by scanning the screener containing 19 high quality undiscovered gems to see which underfollowed stocks align with your return and risk preferences.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.