Western Midstream Partners (WES) Valuation Check After Recent Steady Trading And Modest Undervaluation Estimate

Western Midstream Partners, LP WES | 0.00 |

Western Midstream Partners overview

Western Midstream Partners (WES) stock has drawn attention after recent trading left it near its latest close of US$43.50, prompting investors to reassess how its fundamentals align with current market pricing.

Recent trading has been relatively steady, with the share price slipping around 2% over the last day but posting a 7% 90 day share price return and a 25% 1 year total shareholder return, which points to momentum still holding up.

If you are comparing Western Midstream Partners with other opportunities in infrastructure and essential services, it can be useful to broaden the search to resilient operators across the grid and transmission space using the 34 power grid technology and infrastructure stocks

With Western Midstream Partners showing solid recent returns and trading close to some analyst estimates of fair value, the key question is whether the current price still leaves upside or if the market is already pricing in expectations for the business.

Most Popular Narrative: 3% Undervalued

Western Midstream Partners' most followed narrative pins fair value at about $44.73 per unit, only slightly above the recent $43.50 close. This puts the focus squarely on the underlying growth and cash flow story rather than a big valuation gap.

Investment in major long term capacity expansions, such as the Pathfinder pipeline and North Loving II plant, are set to come online in 2027, adding significant processing and transport capability, and expected to materially increase revenues and cash flows in subsequent years. Continued focus on cost optimization and operational efficiencies are helping contain OpEx even as volumes grow, providing the potential for margin expansion and higher net earnings as new projects ramp up.

Curious how this expansion plan translates into that fair value figure? The narrative leans heavily on compounding revenue, rising margins, and a future earnings multiple that has been carefully stepped down from prior assumptions. The real question is how those moving parts interact over the next few years, and how sensitive the outcome is to even small changes in growth or profitability.

Result: Fair Value of $44.73 (UNDERVALUED)

However, this hinges on capital heavy projects and producer activity holding up. Weaker volumes or project delays could quickly challenge the current fair value story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another way to look at WES

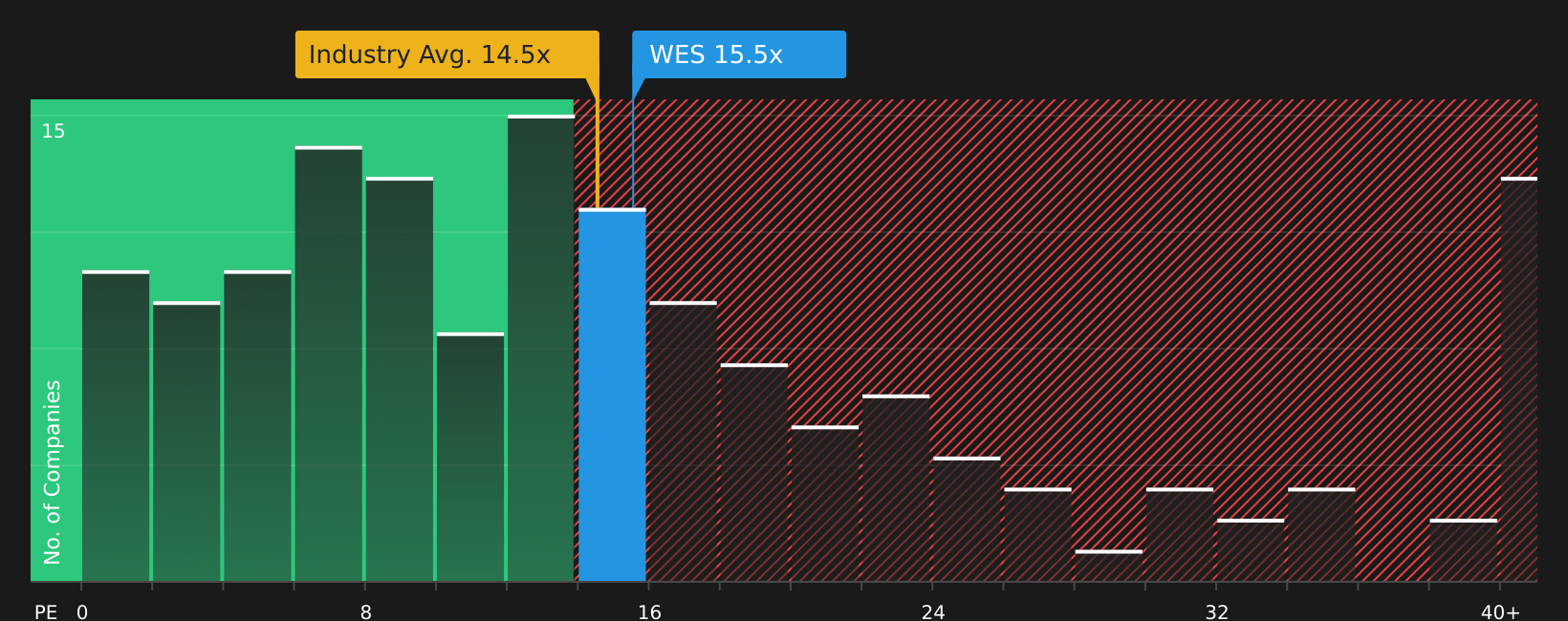

The analyst narrative points to a fair value of $44.73, only a touch above the current $43.50 price. Yet on earnings, WES trades on a P/E of 14.3x, while its fair ratio is 21.6x and peers average 22.3x. If the market edges closer to those levels, investors may see this valuation gap as either a potential cushion or a possible warning sign.

Next Steps

Given the mix of potential upside and clear risks discussed so far, it makes sense to look at the underlying data yourself and decide how comfortable you are with the trade off. To quickly see the key concerns alongside the potential bright spots, review the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If WES has your attention, do not stop here. Use these ready made stock lists to quickly surface other ideas that might better suit your goals.

- Spot underappreciated businesses with strong fundamentals by scanning the screener containing 21 high quality undiscovered gems before other investors catch on.

- Target resilient companies that prioritize financial strength by reviewing the solid balance sheet and fundamentals stocks screener (46 results) for ideas built on sturdier balance sheets.

- Focus on potential cash return and income stability by checking stocks in the 9 dividend fortresses that may fit a yield focused approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.