What Citigroup (C)'s $30 Billion Buyback and Dividend Hike Means For Shareholders

Citigroup Inc. C | 0.00 |

- In recent days, Citigroup Inc. has passed the Federal Reserve’s 2026 stress test, announced a 12% quarterly dividend increase, authorized a multi‑year US$30 billion share repurchase program, and was added to the Russell Top 50 Index, while also issuing several long‑dated senior unsecured fixed‑rate notes and making leadership appointments in its wealth and corporate banking businesses.

- Together, these capital return plans, index inclusion, funding activities, and leadership changes highlight management’s confidence in Citigroup’s capital strength, digital initiatives, and global growth priorities across institutional and wealth management franchises.

- Next, we’ll explore how Citigroup’s new US$30 billion multi‑year share repurchase program may influence its existing investment narrative and outlook.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Citigroup Investment Narrative Recap

To own Citigroup, you need to believe its global network, digital initiatives, and simplification efforts can translate into steadier earnings and better efficiency, while regulatory costs and restructuring remain manageable. The latest stress test pass, higher dividend, and new US$30,000 million buyback strengthen the near term capital return story, but they do not remove the key risk that ongoing transformation, compliance, and restructuring expenses could keep weighing on margins and returns versus peers.

Among the recent announcements, the US$30,000 million multi year share repurchase program stands out as most relevant. For investors focused on catalysts, sizeable buybacks can be an important part of the thesis when a bank is still working through operational clean up, because they can support earnings per share even as transformation and technology spending stays elevated. How effectively Citi balances these repurchases with regulatory and credit risk constraints is likely to be a focal point in the near term.

Yet, against these reassuring capital return headlines, investors should also be aware that...

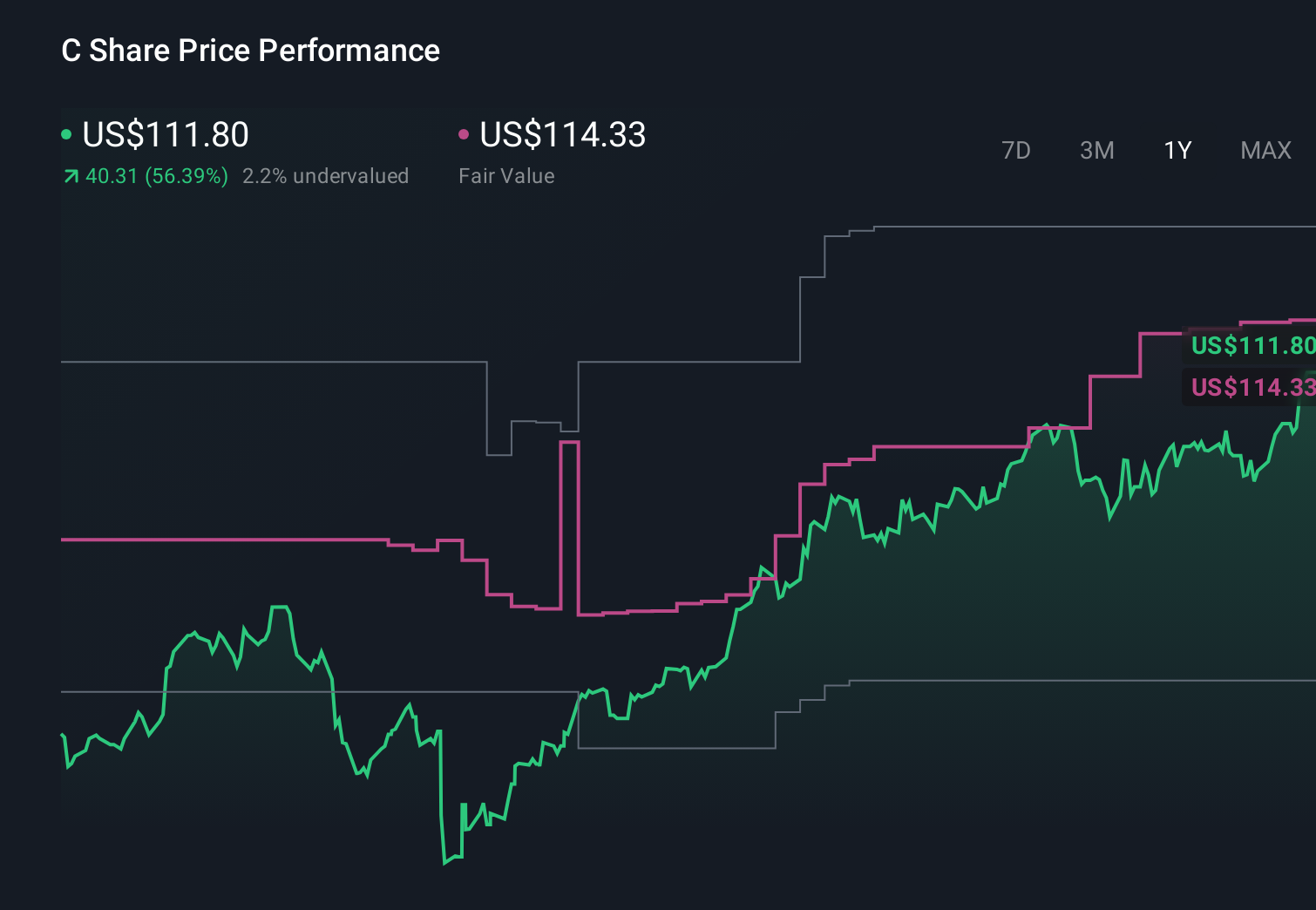

Citigroup's narrative projects $102.4 billion revenue and $21.7 billion earnings by 2029. This requires 9.2% yearly revenue growth and a $7.0 billion earnings increase from $14.7 billion today.

Uncover how Citigroup's forecasts yield a $146.93 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenues of about US$100,400 million and earnings of US$20,600 million by 2029, so you should treat the latest news as a reason to revisit whether you agree with their more pessimistic view or with a more optimistic catalyst like large buybacks improving earnings quality over time.

Explore 10 other fair value estimates on Citigroup - why the stock might be worth 11% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Citigroup research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.