What Citigroup (C)'s Long-Dated Bond Issuance and Restructuring Push Mean For Shareholders

Citigroup Inc. C | 0.00 |

- In late May 2026, Citigroup Inc. raised fresh funding through a series of senior unsecured medium-term note issues, including US$24,000,000 of callable zero-coupon notes due 2033 and multiple fixed-rate issues maturing between 2029 and 2056, all priced at par.

- These offerings, alongside management’s restructuring under CEO Jane Fraser and increased wealth management hiring in Asia, underline Citi’s emphasis on long-dated funding to support growth in higher-margin institutional and wealth businesses.

- Next, we’ll examine how Citi’s recent long-dated bond issuance, paired with its restructuring efforts, could influence the existing investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Citigroup Investment Narrative Recap

To own Citi, you need to believe its global network, restructuring under CEO Jane Fraser, and growing wealth and institutional businesses can translate into better efficiency and returns. The latest long-dated bond issuance modestly supports that thesis by locking in term funding, but it does not fundamentally change the main near term catalyst, which is execution on simplification and cost cuts, or the biggest risk, which remains elevated regulatory, transformation, and restructuring complexity.

Among recent announcements, Citi’s plan to hire about 100 private bankers and 400 specialists globally, with a strong focus on Asia, ties most directly into the investment story around higher margin growth. This hiring push matters alongside the May 2026 bond deals because both relate to funding and building out the wealth franchise, a key catalyst for shifting Citi’s earnings mix toward more fee income and potentially improving its return profile over time.

Yet, while this setup looks appealing, investors should also be aware that regulatory and transformation costs could still...

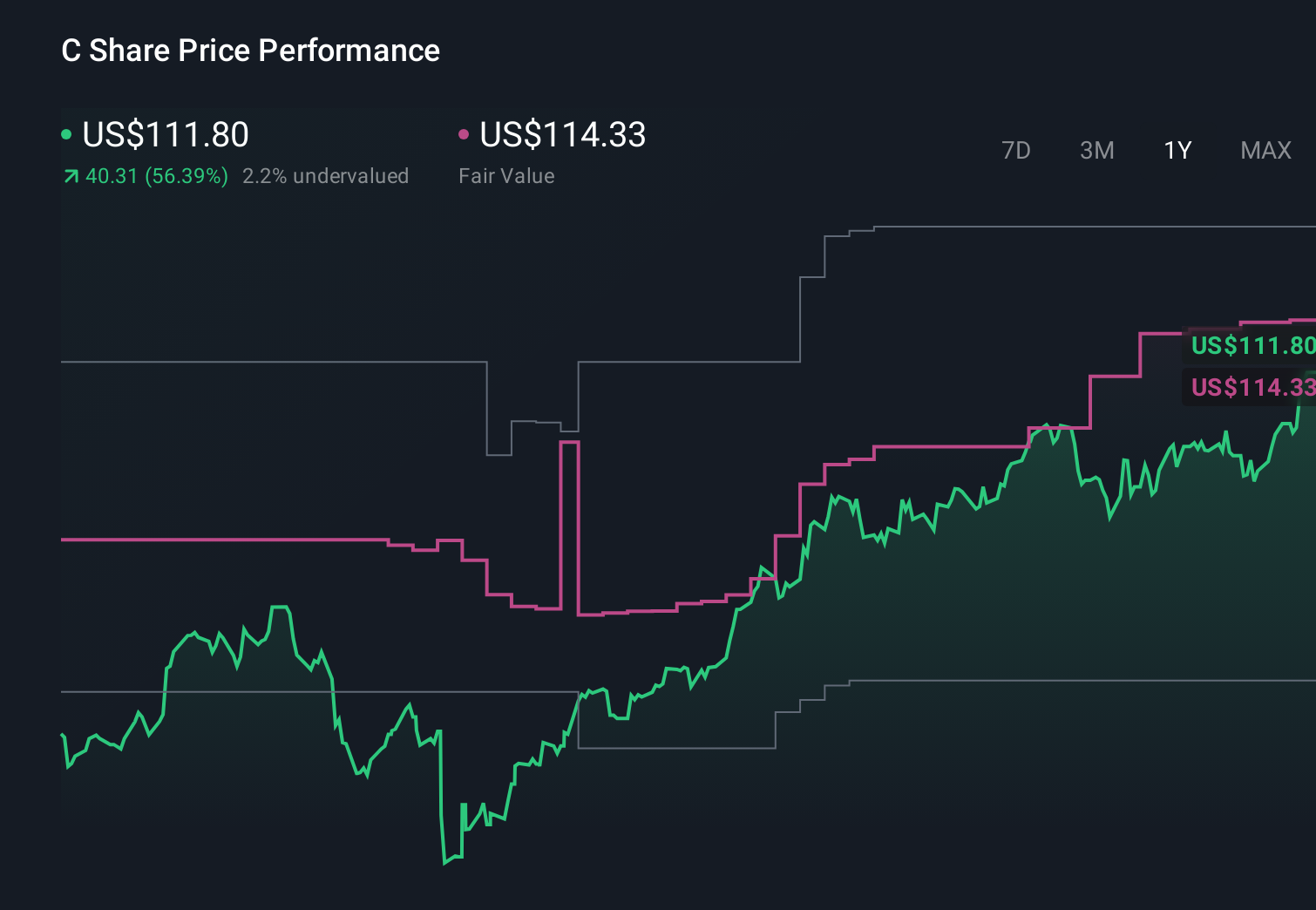

Citigroup’s narrative projects $102.4 billion revenue and $21.7 billion earnings by 2029. This requires 9.2% yearly revenue growth and a $7.0 billion earnings increase from $14.7 billion today.

Uncover how Citigroup's forecasts yield a $146.93 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Lowest case analysts were already cautious, assuming revenue of about US$96.2 billion and earnings of US$18.9 billion by 2029, so you should recognize how much more concerned they are about high ongoing transformation and technology expenses possibly weighing on profitability, especially when you set those expectations against Citi’s fresh long dated bond issuance and the broader catalyst of cost reduction that both narratives will likely need to reassess.

Explore 11 other fair value estimates on Citigroup - why the stock might be worth as much as 81% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Citigroup research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

No Opportunity In Citigroup?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.