What CNO Financial Group (CNO)'s Evercore Upgrade on Long-Term Care Strength Means For Shareholders

CNO Financial Group, Inc. CNO | 0.00 |

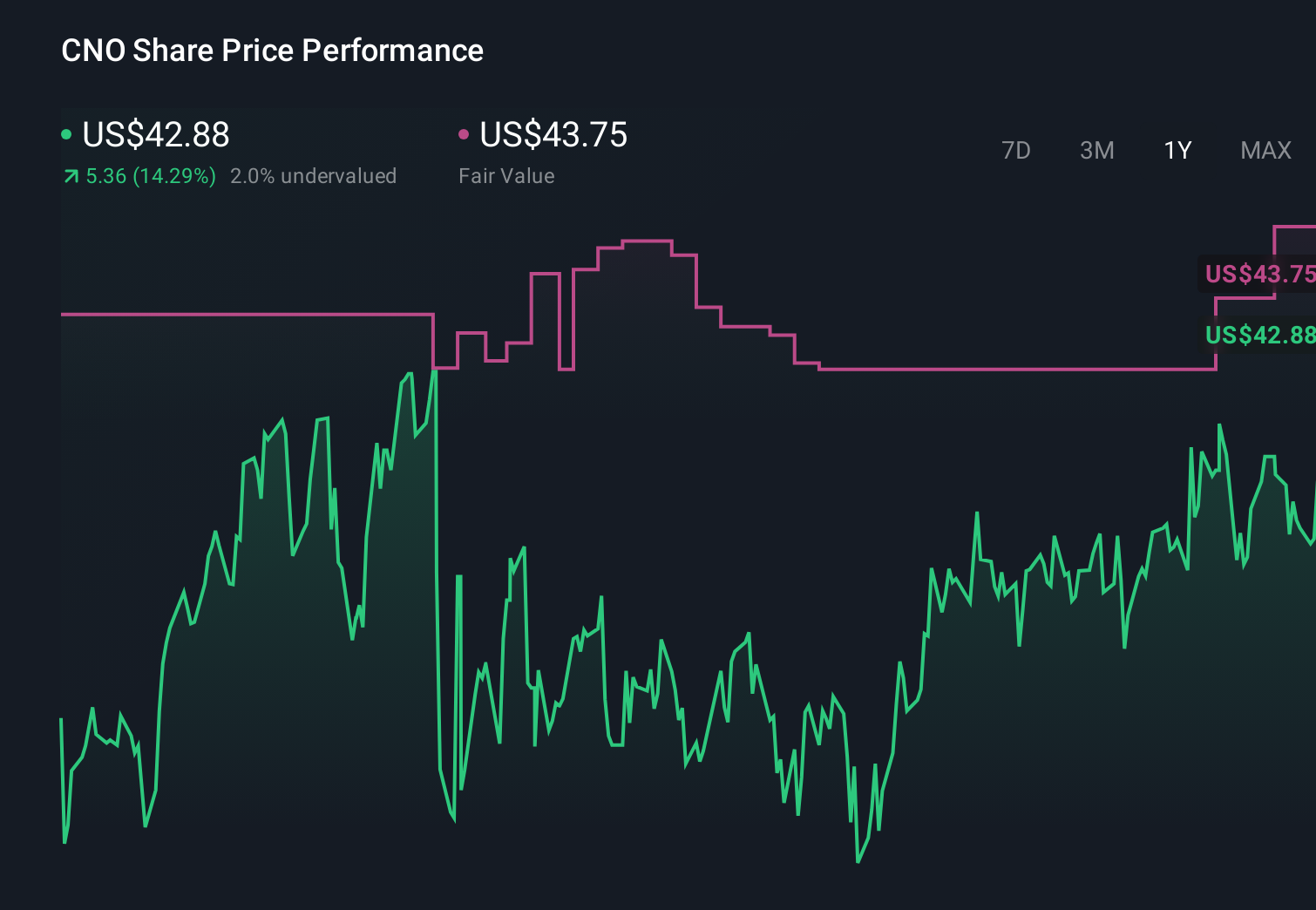

- In recent days, Evercore ISI upgraded CNO Financial Group to an In Line rating, pointing to stronger long-term care performance, favorable claims trends, and first-quarter 2026 results that exceeded earnings and revenue expectations.

- While the company has faced pressure from rising costs, modest premium growth, and declining book value per share, its pivot toward shorter-duration long-term care products with mostly one-year-or-less benefit periods is emerging as an important source of resilience.

- Now we’ll examine how Evercore’s upgrade, driven by improving long-term care claims experience, reshapes CNO Financial Group’s broader investment narrative.

Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

CNO Financial Group Investment Narrative Recap

To own CNO Financial Group, you need to be comfortable with a middle‑income retirement and health insurer that is working through cost pressure and modest premium growth while leaning on improving long‑term care performance. Evercore’s upgrade, tied to favorable long‑term care claims and shorter benefit periods, reinforces the main near term catalyst of better underwriting results, but it does not fully resolve the key risk around rising expenses and declining book value per share.

The recent first quarter 2026 results, which came in ahead of earnings and revenue expectations, are especially relevant here because they give fresh evidence on whether cost pressure and credit quality issues are being contained. Stronger reported profitability, alongside the shift toward shorter‑duration long term care products, feeds directly into the argument that improved long term care claims experience can offset some of the margin and capital headwinds investors have been watching.

Yet against the positive headlines, investors should be aware that rising day to day expenses and ongoing book value per share declines could still...

CNO Financial Group's narrative projects $4.4 billion revenue and $483.0 million earnings by 2029. This requires revenue to remain fairly flat over the next few years and an earnings increase of about $237.5 million from $245.5 million today.

Uncover how CNO Financial Group's forecasts yield a $48.25 fair value, a 3% upside to its current price.

Exploring Other Perspectives

One member of the Simply Wall St Community currently pegs CNO Financial Group’s fair value at US$48.25, underscoring how concentrated individual views can be. You can weigh this against the recent focus on improving long term care claims experience and consider how a shift in those trends could influence your own expectations for the business.

Explore another fair value estimate on CNO Financial Group - why the stock might be worth as much as $48.25!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CNO Financial Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CNO Financial Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNO Financial Group's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.