What Do Lower Earnings Say About Insight Enterprises' (NSIT) Strategy in the Competitive IT Sector?

Insight Enterprises, Inc. NSIT | 67.23 67.23 | +0.33% 0.00% Post |

- Insight Enterprises recently reported its second quarter and six-month results for 2025, showing that revenue decreased to US$2.09 billion and US$4.20 billion, and net income fell to US$46.93 million and US$54.45 million, respectively, compared to the same periods last year.

- This drop in both revenue and net income highlights ongoing challenges in the IT solutions sector, even as the company continues to focus on storage strategies and business growth.

- We'll examine how Insight Enterprises' recent earnings shortfall, marked by lower revenue and profit, could impact its investment narrative.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Insight Enterprises Investment Narrative Recap

To be a shareholder in Insight Enterprises, you need confidence in the company’s ability to monetize growing demand for AI-enabled IT transformation and capture resilient, higher-margin recurring revenue as clients modernize infrastructure. The recent Q2 earnings miss adds pressure in the near term, but it does not materially shift the most important short-term catalyst, enterprise investment in IT infrastructure, or the main risk, which remains ongoing hesitancy among large customers due to macro uncertainty and AI adoption caution.

Of recent company announcements, the "Future-Ready Storage Strategies for Business Growth" call stands out as directly relevant. This focus aligns with the company’s efforts to address evolving enterprise needs, particularly where modernized storage and infrastructure underpin the catalyst of accelerated hardware and services demand, even as near-term profit and revenue results reflect persistent industry headwinds.

But on the downside, investors should be aware that if enterprise IT spending fails to recover as expected, especially as clients remain cautious about future AI and infrastructure outlays, then...

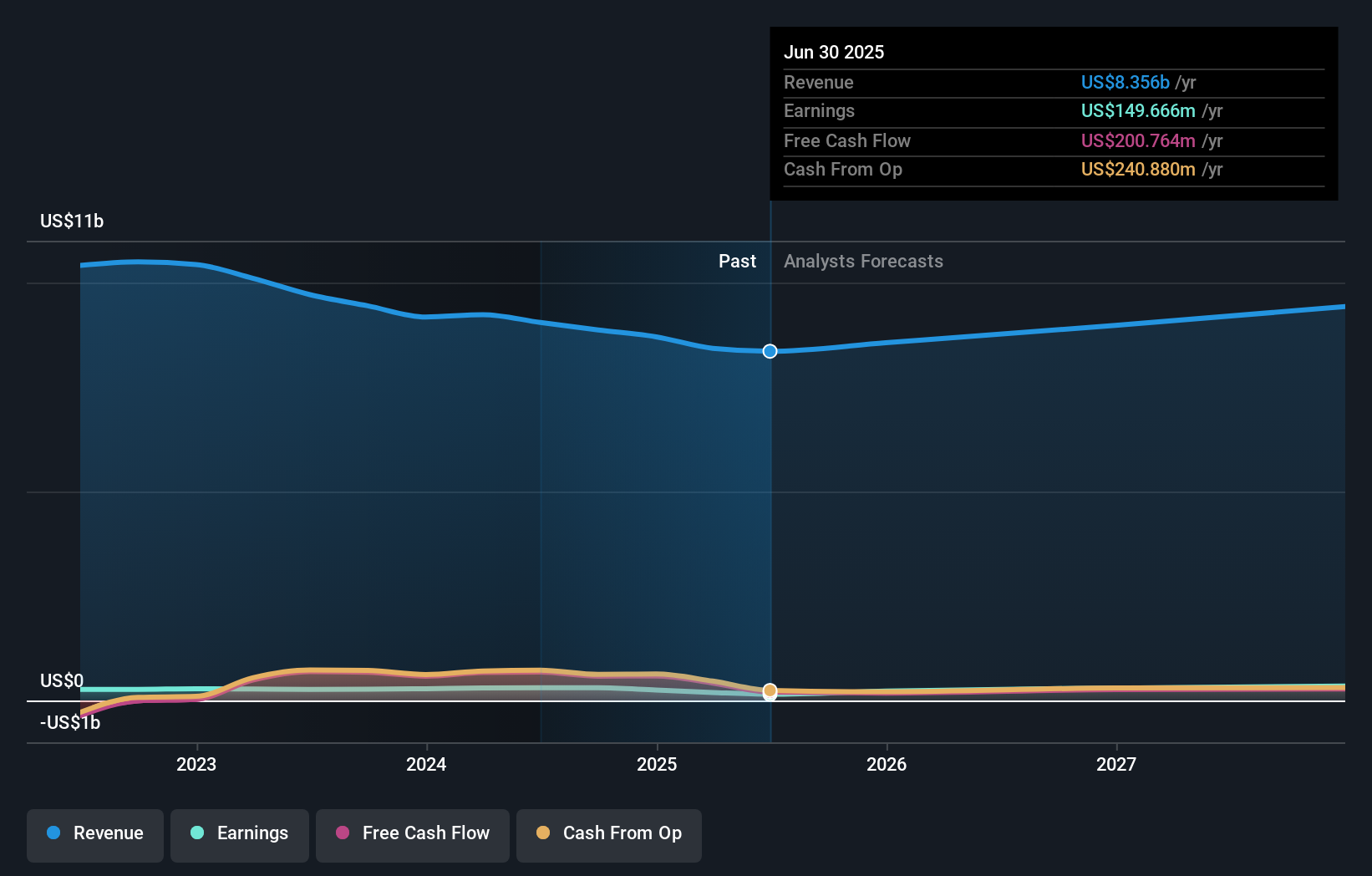

Insight Enterprises' outlook projects $9.6 billion in revenue and $420.5 million in earnings by 2028. This is based on 4.9% annual revenue growth and a $270.8 million earnings increase from current earnings of $149.7 million.

Uncover how Insight Enterprises' forecasts yield a $157.00 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community estimate Insight Enterprises’ fair value between US$118.88 and US$172.84 per share. While many focus on long-term AI-driven catalysts, the risk of delayed enterprise spending continues to shape sentiment across the market.

Explore 4 other fair value estimates on Insight Enterprises - why the stock might be worth just $118.88!

Build Your Own Insight Enterprises Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Insight Enterprises research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Insight Enterprises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Insight Enterprises' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.