What Do Recent Property Acquisitions Mean for LTC Properties’ Valuation in 2025?

LTC Properties, Inc. LTC | 39.29 | -1.63% |

- Ever wondered if LTC Properties is quietly offering more value than its recent share price lets on? Let’s dig beneath the surface and see what’s really on offer for investors.

- The stock’s been on a modest ride lately, up 1.1% over the last week but essentially flat compared to a year ago, despite a 4.6% gain since the start of the year.

- Recent headlines have zeroed in on LTC’s portfolio activity, including new property acquisitions and notable refinancings, which have caught investor interest. There’s a growing sense that these moves could shift the stock’s risk profile and open up further growth opportunities down the line.

- LTC Properties currently earns a 5 out of 6 valuation score, which is a strong sign that the company looks undervalued by most traditional checks. We’ll break down exactly how analysts got to that number next, but stick around because we’ll end with an approach that offers an even deeper take on what LTC is really worth.

Approach 1: LTC Properties Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model helps estimate a company's true worth by forecasting its future adjusted funds from operations, then discounting those projected cash flows back to today’s dollars. For LTC Properties, analysts start with current Free Cash Flow of $123.43 million and project steady growth based on recent operating performance and industry expectations.

According to available estimates, LTC’s Free Cash Flow is projected to reach $159.95 million by the end of 2027. Looking further out, the model extrapolates its annual Free Cash Flow out ten years, using inputs from both analysts and systematic growth estimates. For 2035, the DCF model estimates Free Cash Flow at $228.43 million, all figures reported in US dollars.

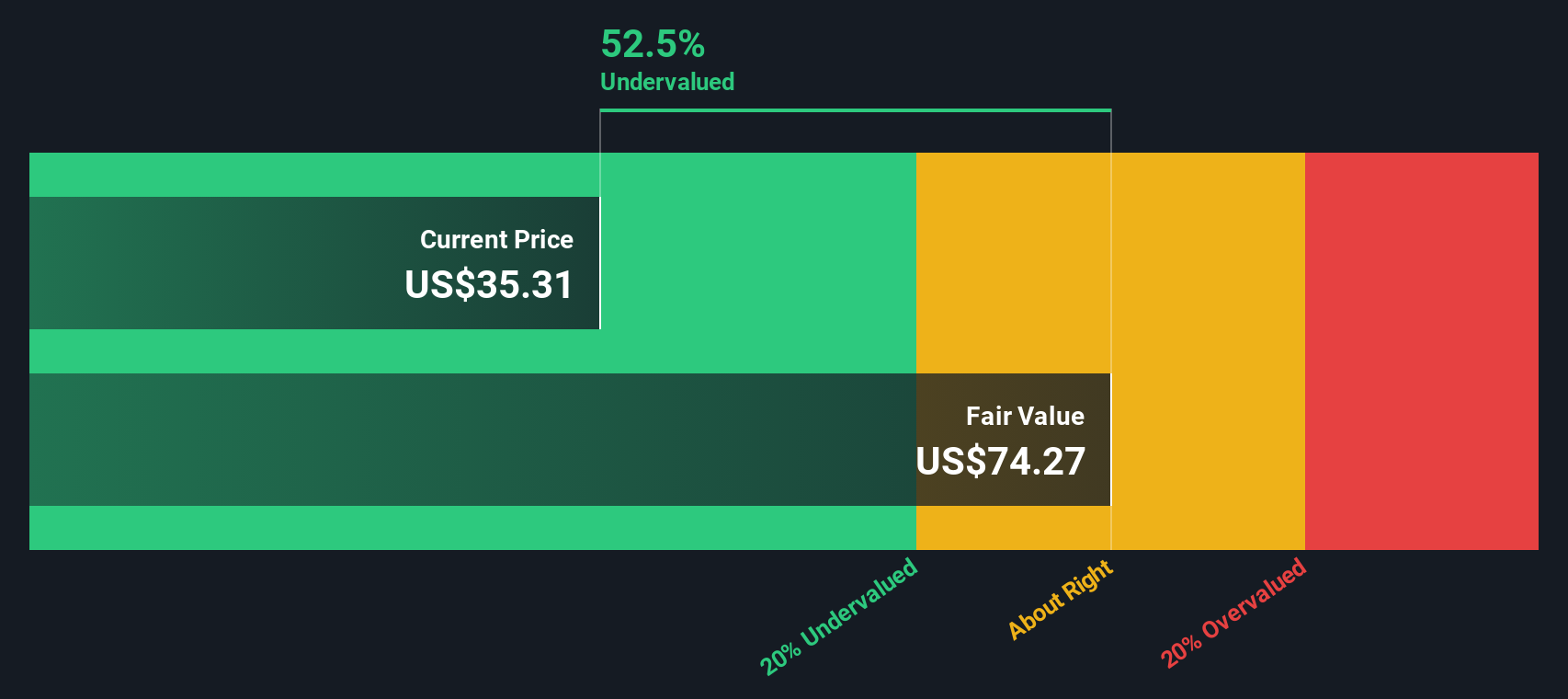

After discounting these future cash flows to reflect today’s risk and time value, the DCF analysis arrives at an estimated intrinsic value of $85.05 per share. With the current share price standing about 58.2% below this fair value, the model indicates the stock is significantly undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests LTC Properties is undervalued by 58.2%. Track this in your watchlist or portfolio, or discover 840 more undervalued stocks based on cash flows.

Approach 2: LTC Properties Price vs Earnings

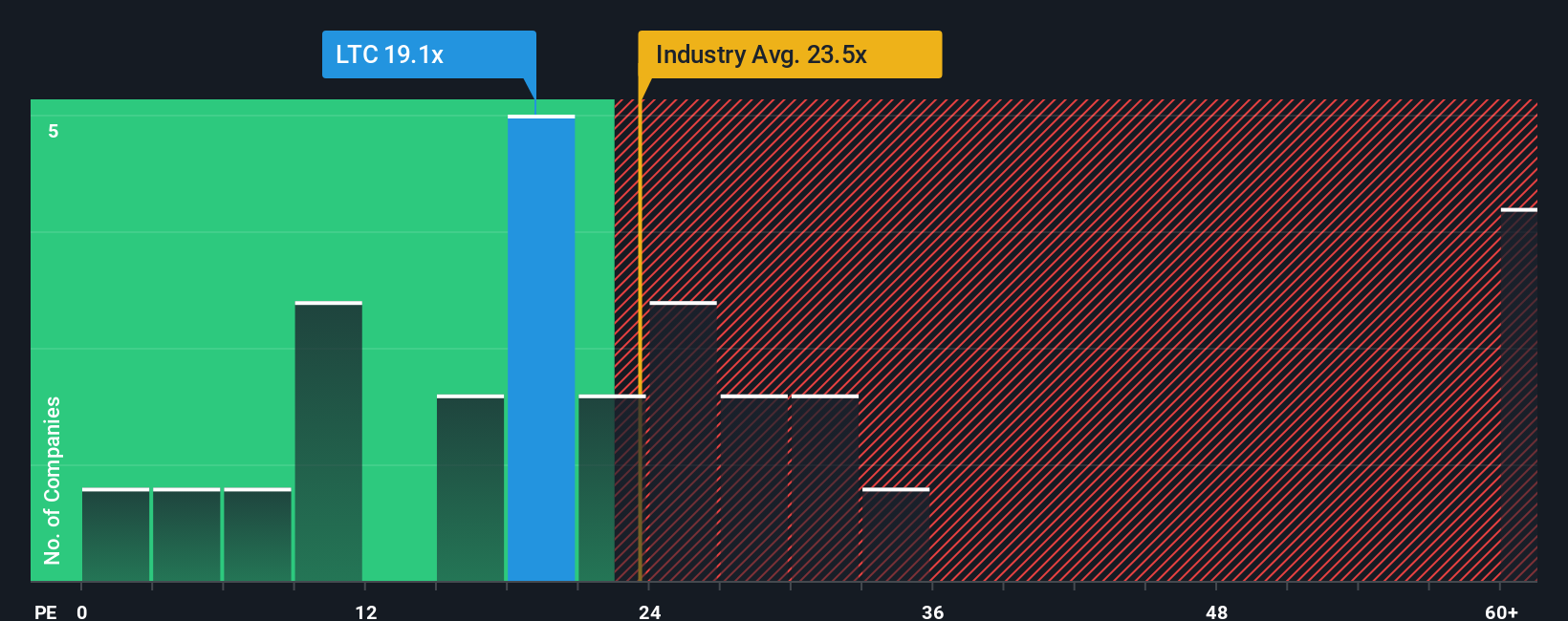

The Price-to-Earnings (PE) ratio is a reliable valuation tool for profitable companies like LTC Properties, since it reflects how much investors are willing to pay today for each dollar of future earnings. It is especially meaningful when comparing businesses in the same sector or with similar growth profiles.

What counts as a “normal” or “fair” PE ratio typically depends on a company’s prospects. Companies with better growth expectations or lower risk often command higher PE ratios, while slower growth or higher uncertainty push that number lower.

At present, LTC Properties is trading at a PE ratio of 19.9x. This is noticeably below the average for its Health Care REITs industry peers, which sits at 24.0x, and it is well under the peer group average of 26.6x. By these classic measures, LTC appears to be trading at a discount.

However, Simply Wall St’s proprietary “Fair Ratio” goes a step further. This benchmark considers not just peer and industry averages but also factors like LTC’s earnings growth, profit margins, market cap and underlying risks, providing a more context-driven estimate of what a justified PE should be. For LTC, the Fair Ratio is calculated at 34.0x, substantially above both its current PE and the usual benchmarks.

Given this difference, LTC Properties appears undervalued by this approach as well.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1411 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your LTC Properties Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a clear, simple story that brings together your views about a company's prospects and translates them into specific forecasts for future revenue, earnings, and margins, ultimately guiding you to what you believe is a fair value for the business.

This approach connects the facts about LTC Properties to your own perspective, helping you link the company's underlying story to a financial forecast, and then to a valuation estimate, all in one place. Narratives are easy to use and are built directly into Simply Wall St's Community page, where millions of investors share and compare their views.

With Narratives, you can quickly see if your fair value is higher or lower than the current share price, making it straightforward to decide when to buy or sell. Plus, your Narrative updates automatically as news breaks or earnings come in, so your investment thesis stays fresh and relevant.

For LTC Properties, one investor might see long-term stability from expanding modern senior housing and expect the stock to reach $43.0, while another might worry about rising debt costs and set a much more cautious target of $34.0. Each Narrative drives a different decision, all based on the same set of numbers.

Do you think there's more to the story for LTC Properties? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.