What Enterprise Products Partners (EPD)'s Analyst Reassessment and Barclays Stake Cut Means For Shareholders

Enterprise Products Partners L.P. EPD | 37.57 | +0.37% |

- In recent weeks, Enterprise Products Partners has drawn heightened investor attention as analysts reassess the midstream partnership amid mixed research ratings and institutional ownership shifts, including Barclays cutting its stake.

- At the same time, the partnership’s long record of annual distribution increases and volume-based fee model is underscoring its role as a relatively defensive income play within the energy infrastructure space.

- We’ll now examine how Barclays’ reduced holding and the broader analyst reassessment may influence Enterprise Products Partners’ existing investment narrative.

The future of work is here. Discover the 28 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe in the durability of its fee-based midstream model and its ability to keep funding distributions despite sector volatility and a high debt load. Recent analyst debates, a Zacks Rank of #3 (Hold), and Barclays’ reduced stake highlight near term sentiment shifts but do not materially change the central near term catalyst of new capacity ramping up, nor the key risk around balance sheet leverage and external shocks to producer activity.

The most relevant recent development is Enterprise’s 2.8% increase in its quarterly cash distribution to US$0.55 per unit, extending its multi decade streak of annual distribution growth. This move sits squarely at the intersection of its main catalyst, the monetization of new processing and export projects, and the main risk that higher payouts and elevated debt could constrain financial flexibility if credit conditions or producer volumes weaken.

However, investors should be aware that if debt costs rise or Permian activity slows, the cushion behind that growing payout could...

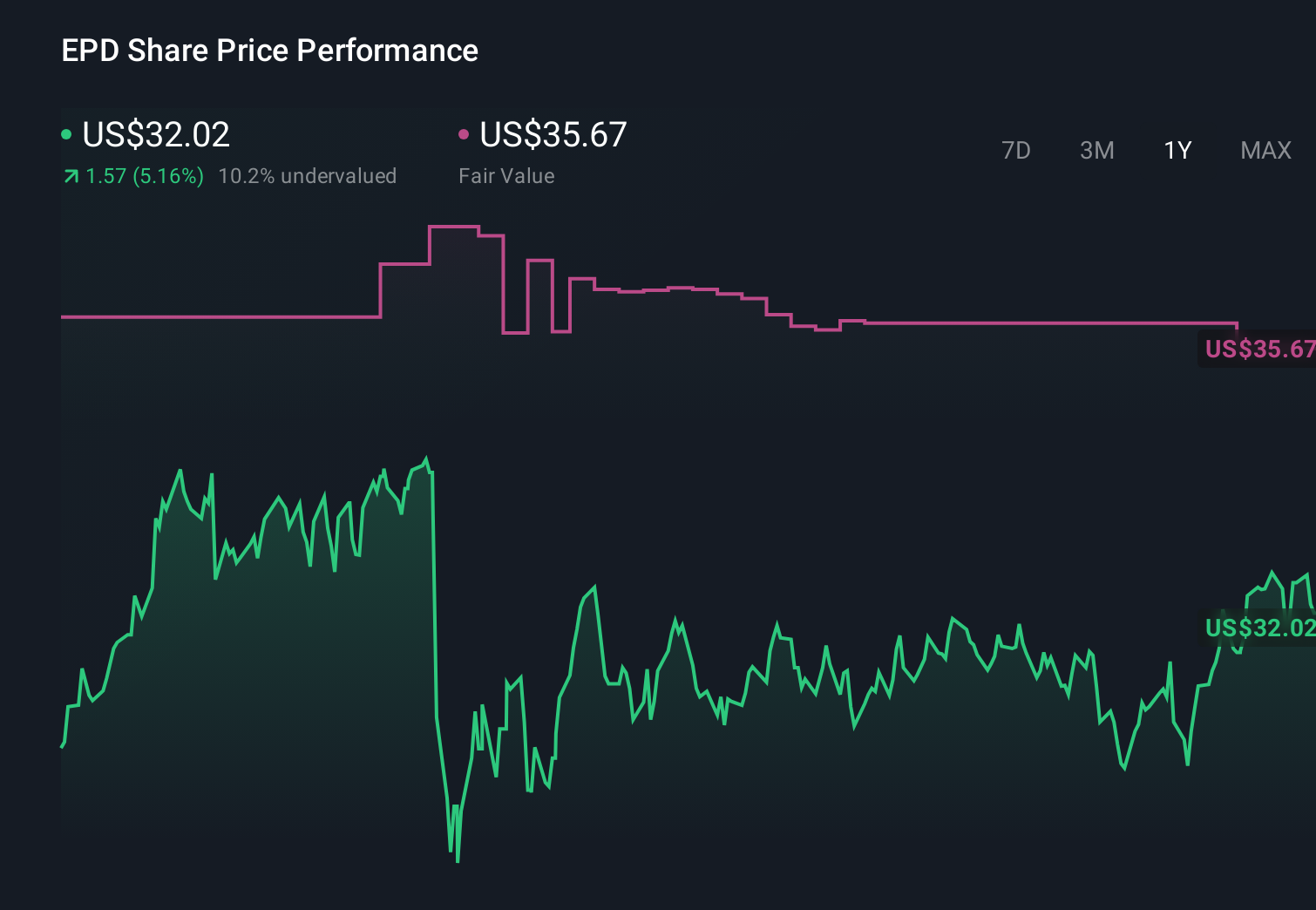

Enterprise Products Partners' narrative projects $53.5 billion revenue and $6.6 billion earnings by 2028. This assumes revenue will decline by 0.8% per year and implies an earnings increase of about $0.8 billion from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $36.65 fair value, in line with its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently place Enterprise’s fair value between US$34 and about US$86, reflecting a wide dispersion of views. Before weighing those against your own outlook, remember that Enterprise’s biggest near term swing factor is how effectively it converts new Permian and export capacity into stable, fee based cash flow.

Explore 8 other fair value estimates on Enterprise Products Partners - why the stock might be worth 9% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 50 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.