What MasTec (MTZ)'s Strong Q1 Beat and Cautious Outlook Means For Shareholders

MasTec, Inc. MTZ | 0.00 |

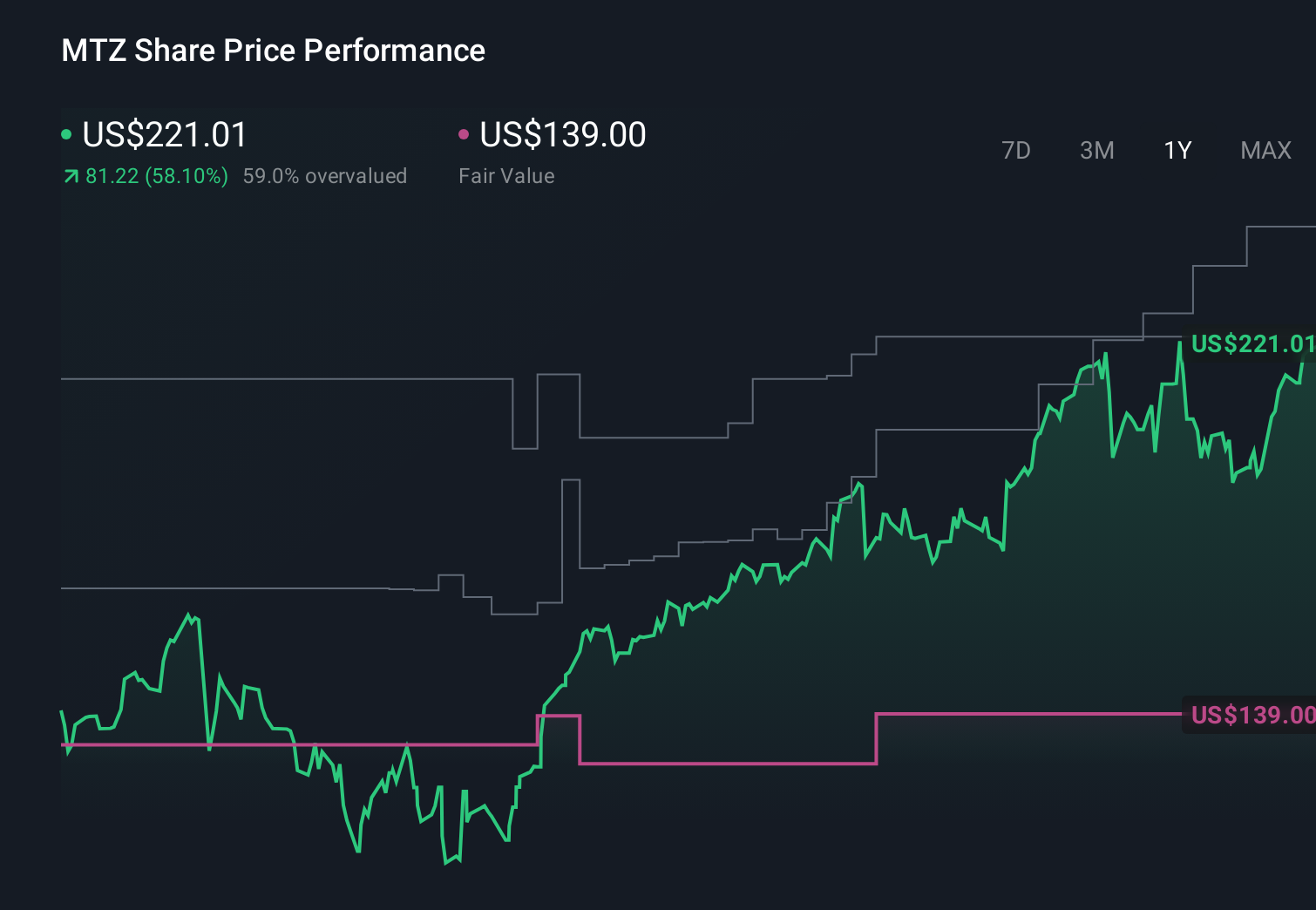

- MasTec recently reported strong Q1 results with double-digit growth in revenue and profitability that surpassed its own guidance and analyst expectations, even as it maintained a more cautious full-year outlook than many peers.

- Analysts have highlighted this contrast between robust current execution and weaker full-year guidance, alongside recent insider share sales, as a key tension shaping investor sentiment on MasTec’s infrastructure growth prospects.

- We’ll now examine how MasTec’s strong Q1 beat but comparatively weaker full-year outlook could influence the company’s investment narrative and risk-reward.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

MasTec Investment Narrative Recap

To own MasTec, you need to believe its infrastructure capabilities across telecom, energy, and utilities can translate current execution into durable earnings, despite project and regulatory risks. The latest Q1 beat reinforces that execution, but the comparatively cautious full year guidance is a reminder that near term results still hinge on timely project awards and backlog conversion. Insider selling of about US$4.0 million in shares is a secondary concern and does not materially change the core risk reward right now.

The most relevant recent announcement is MasTec’s Q1 2026 report, where revenue rose to US$3,828.8 million and net income to US$60.84 million, ahead of guidance. At the same time, management raised full year 2026 guidance only modestly to US$17,500 million in revenue and US$575 million in net income, which now sits at the heart of the tension between strong near term execution and questions about how quickly high fixed costs and project complexity will translate into higher, more stable margins.

Yet behind the strong quarter, investors should still be aware of how project delays could interact with MasTec’s higher fixed cost base and...

MasTec's narrative projects $20.3 billion revenue and $880.9 million earnings by 2029. This requires 12.5% yearly revenue growth and a roughly $482 million earnings increase from $399.0 million today.

Uncover how MasTec's forecasts yield a $348.72 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Before this Q1 beat, the most optimistic analysts were already banking on MasTec lifting revenue toward about US$25.5 billion and earnings to roughly US$1.3 billion by 2029, which is a far more aggressive backdrop than the consensus view and could be challenged or reinforced as new data center and grid projects, as well as fossil fuel related risks, play out in light of the latest guidance reset.

Explore 6 other fair value estimates on MasTec - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MasTec research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MasTec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MasTec's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.