What Mastercard (MA) Joining Open USD Means For Its Valuation

Mastercard MA | 0.00 |

Mastercard (MA) has joined more than 140 partners to back Open USD, a US dollar pegged stablecoin designed to enable low cost, high throughput and accessible digital payments for cross border and commercial use.

Recent news around Open USD, VEON partnerships and the Africa Cybersecurity Center of Excellence has coincided with a sharp short term rebound in Mastercard. The 7 day share price return is 10.32% and the 1 month share price return is 12.92%, while the year to date share price return is still down 4.22% and the 1 year total shareholder return is also down 4.68%. This is set against a 3 year total shareholder return of 39.44% and a 5 year total shareholder return of 49.83%, which together suggest that recent momentum has picked up after a softer patch.

If Mastercard’s push into digital payments and stablecoins has your attention, this can be a useful moment to look at other stocks riding similar themes through our 20 cryptocurrency and blockchain stocks

With Mastercard now at $539.39 and trading on a premium valuation score of 2, yet sitting about 19% below the average analyst price target and with a large intrinsic discount flagged, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 28.1% Undervalued

According to the most followed narrative on Mastercard, a fair value of $750 sits well above the last close at $539.39, which frames the current rebound in a very different light.

This will not excite anyone chasing a big yield today. What it offers instead is a business that compounds safely, a payout growing at double-digit rates from a tiny base, and a price that does not currently reflect either of those things.

Curious what supports that $750 figure? The narrative leans on robust margins, steady earnings compounding and a future profit multiple usually reserved for market leaders. The exact mix might surprise you.

Result: Fair Value of $750 (UNDERVALUED)

However, Mastercard’s story could be challenged if regulation squeezes swipe fees more than expected or if stablecoin payment rails gain traction faster than its own solutions.

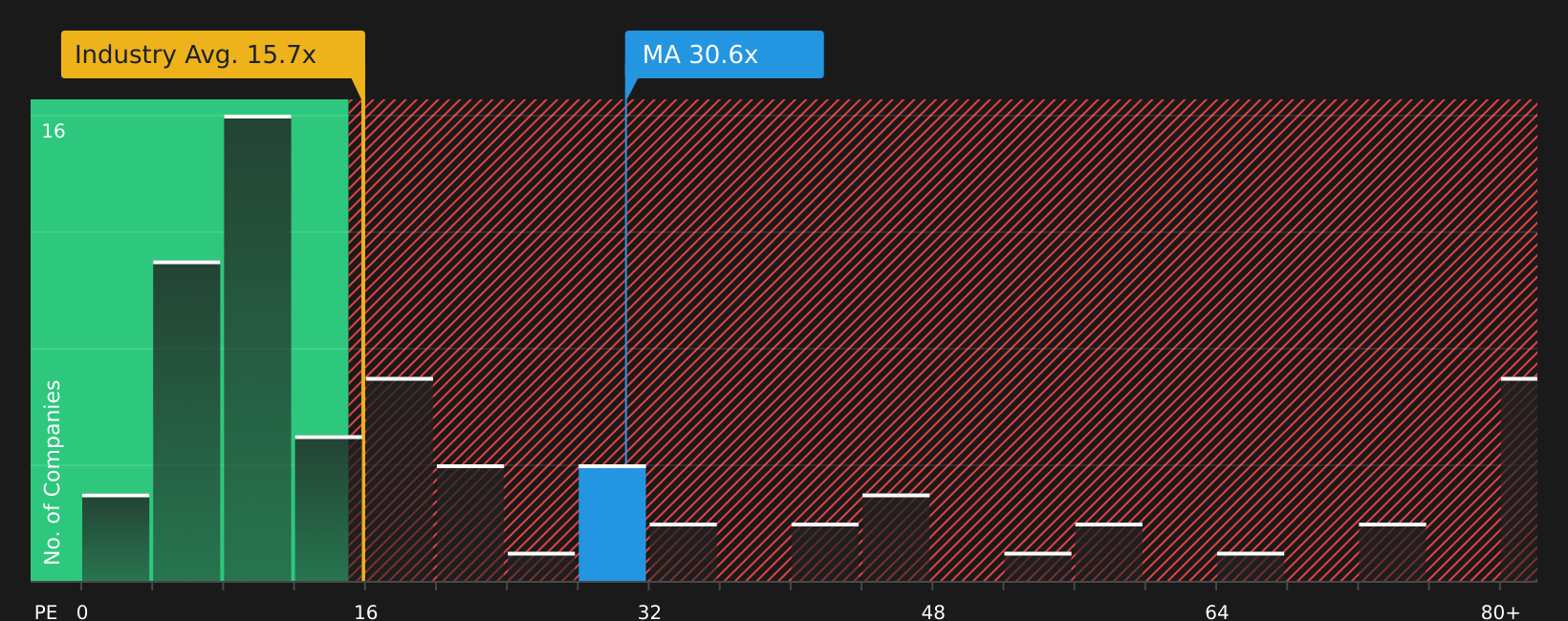

Another View: What Mastercard’s P/E Is Telling You

The DCF output suggests Mastercard could be trading well below its future cash flow value, yet the P/E ratio presents a tighter picture. At 30.6x earnings, Mastercard sits at almost double the US Diversified Financial industry at 15.7x and above peer averages at 26.6x, while the fair ratio is 20.9x. That gap points to potential valuation risk if expectations cool, so how comfortable are you paying a premium for this quality story?

For a closer look at how this earnings multiple compares with what the market could move towards, review the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed sentiment around Mastercard has you weighing both sides, consider moving quickly to review the underlying numbers and decide where you stand. You can start with the 3 key rewards and 1 important warning sign.

Looking for more Mastercard investment ideas?

If Mastercard’s setup has you thinking bigger, do not stop here. Use the Simply Wall St screener to spot other opportunities before the crowd does.

- Target reliable cash generators by scanning companies in the solid balance sheet and fundamentals stocks screener (46 results) that pair financial strength with underlying business resilience.

- Hunt for mispriced quality by reviewing the 43 high quality undervalued stocks that highlights stocks with strong fundamentals trading below their estimated worth.

- Spot under the radar potential by checking the screener containing 18 high quality undiscovered gems that focuses on quality companies many investors may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.