What Seadrill (SDRL)'s Buyback Extension and Larger Credit Line Means For Shareholders

Seadrill Limited SDRL | 0.00 |

- On June 22, 2026, Seadrill Limited extended its share repurchase plan through December 31, 2026 and, a few days earlier, amended its senior secured revolving credit facility to increase borrowing capacity from US$225 million to US$300 million and push the maturity out to 2031.

- Together, the buyback extension and expanded, longer-dated credit line highlight management’s focus on preserving financial flexibility while still allocating capital to shareholders.

- We’ll now examine how the enlarged, longer-maturity credit facility reshapes Seadrill’s existing investment narrative and risk-reward profile.

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Seadrill Investment Narrative Recap

To own Seadrill today, you need to be comfortable with a company that is still unprofitable but leaning on a growing contract backlog and improved liquidity to bridge a choppy offshore market. The enlarged revolver and extended buyback do not change the key short term catalyst, which is execution on newly awarded contracts, nor the biggest near term risk, which remains softer utilization and day rate pressure weighing on margins and cash generation.

Among recent developments, the Q1 2026 update and raised 2026 revenue guidance to US$1.43 billion to US$1.48 billion is most relevant here, because it ties directly to how Seadrill plans to use its greater financial flexibility. The bigger, longer-dated revolver supports working capital and potential idle-time gaps as rigs roll into new contracts, which matters if competitive pressure or regional delays extend the period of weaker utilization that analysts have been warning about.

Yet beneath the improved liquidity, investors should be aware that...

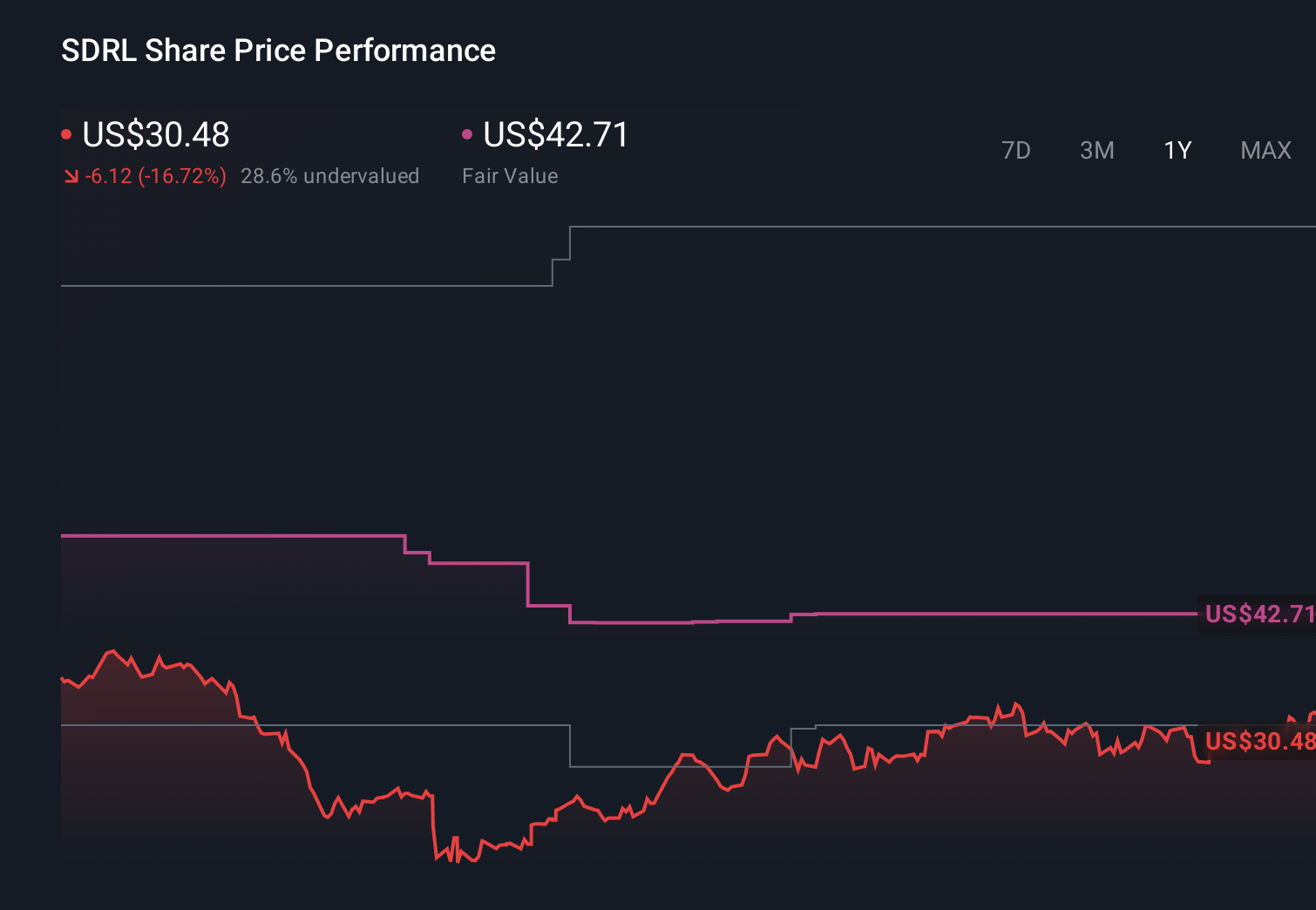

Seadrill's narrative projects $1.7 billion revenue and $194.6 million earnings by 2029. This requires 6.8% yearly revenue growth and a $271.6 million earnings increase from -$77.0 million today.

Uncover how Seadrill's forecasts yield a $51.71 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming only about 3.6% annual revenue growth and US$258.2 million of earnings by 2029, so if you are weighing the new credit facility and buyback extension, it is worth recognizing that their more pessimistic view of offshore demand and contract visibility could shift again once this fresh financing flexibility is fully reflected in updated models.

Explore 4 other fair value estimates on Seadrill - why the stock might be worth just $45.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.