What United Rentals (URI)'s Record High and Analyst Upgrade Means For Shareholders

United Rentals, Inc. URI | 0.00 |

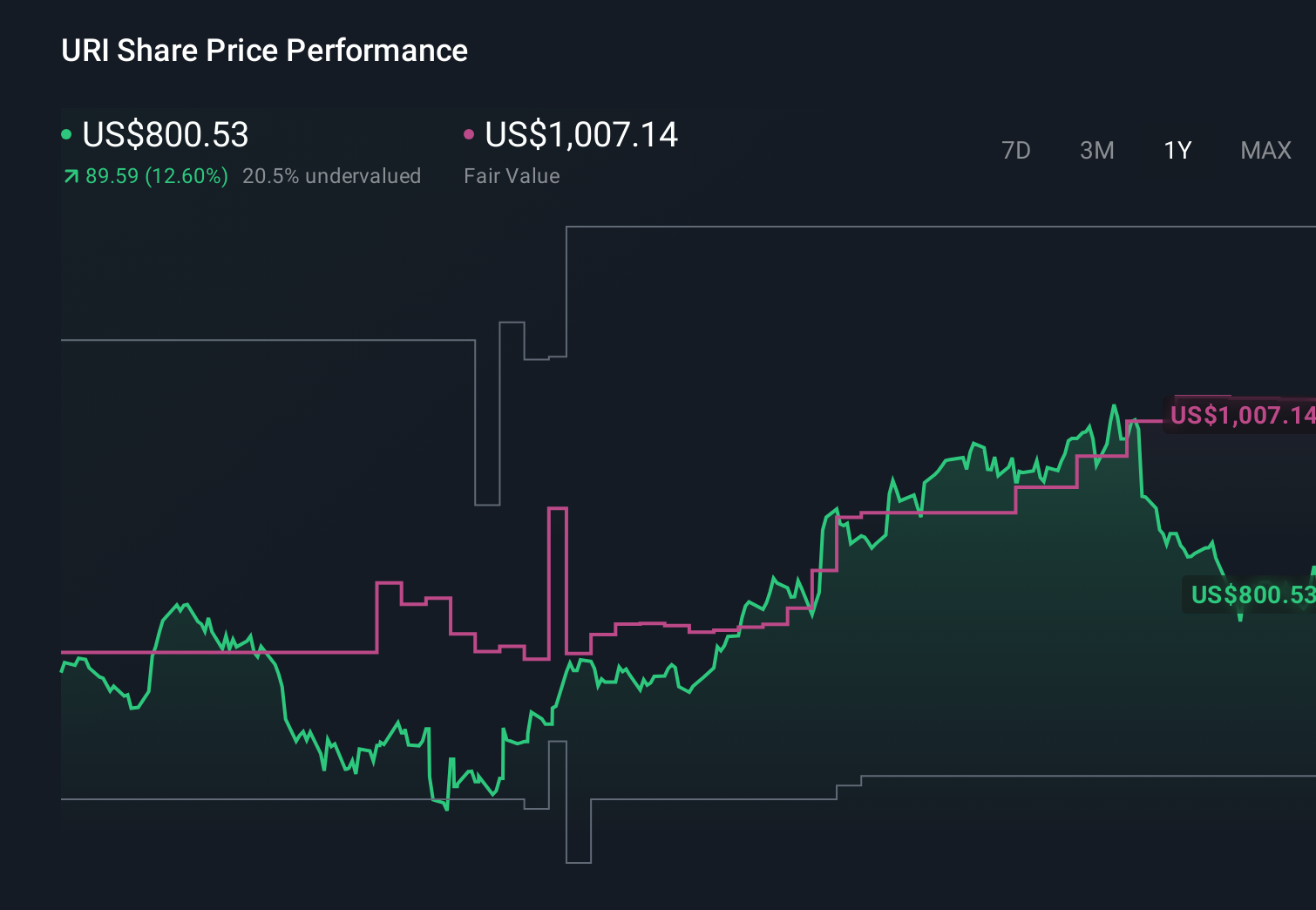

- Earlier this week, United Rentals was highlighted for hitting a record high and receiving an analyst upgrade based on rising earnings estimates and strong operational trends such as higher rental volumes and improved fleet productivity.

- The news underscores how improving earnings expectations and expanding specialty operations are increasingly shaping how investors view the company’s long-term earnings power and risk profile.

- We’ll now examine how the recent analyst upgrade, driven by upward earnings estimate revisions, may reshape United Rentals’ investment narrative.

The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

United Rentals Investment Narrative Recap

To own United Rentals, you have to believe that its scale, specialty rentals and “one stop shop” model can keep driving attractive returns despite heavy capital needs. The recent analyst upgrade and record high price reinforce the near term catalyst of improving earnings expectations, but they do not remove the key risk that large projects or specialty growth could slow just as elevated CapEx and debt commitments remain in place.

The most relevant recent development is management’s decision to expand and extend its share repurchase plan, authorizing up to US$5,000 million with no end date. In the context of stronger rental volumes, specialty expansion and rising earnings estimates, this kind of capital return can support per share earnings power, but it also increases the importance of sustaining free cash flow in a capital intensive, project driven business.

Yet behind the upbeat headlines, investors should also be aware of the risk that high debt and ongoing CapEx could become more painful if...

United Rentals' narrative projects $20.6 billion revenue and $3.6 billion earnings by 2029. This requires 8.0% yearly revenue growth and about a $1.1 billion earnings increase from $2.5 billion today.

Uncover how United Rentals' forecasts yield a $1084 fair value, a 3% downside to its current price.

Exploring Other Perspectives

While the upgrade highlights improving momentum, the most pessimistic analysts were already assuming only about 5.7% annual revenue growth to roughly US$19.4 billion and earnings of about US$3.2 billion by 2029, reminding you that views on URI’s debt load and margin pressure can differ sharply and may shift again as this new information is digested.

Explore 4 other fair value estimates on United Rentals - why the stock might be worth as much as $1084!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your United Rentals research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free United Rentals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Rentals' overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.