What Williams Companies (WMB)'s Q1 Beat and Dividend Hike Means For Shareholders

Williams Companies, Inc. WMB | 0.00 |

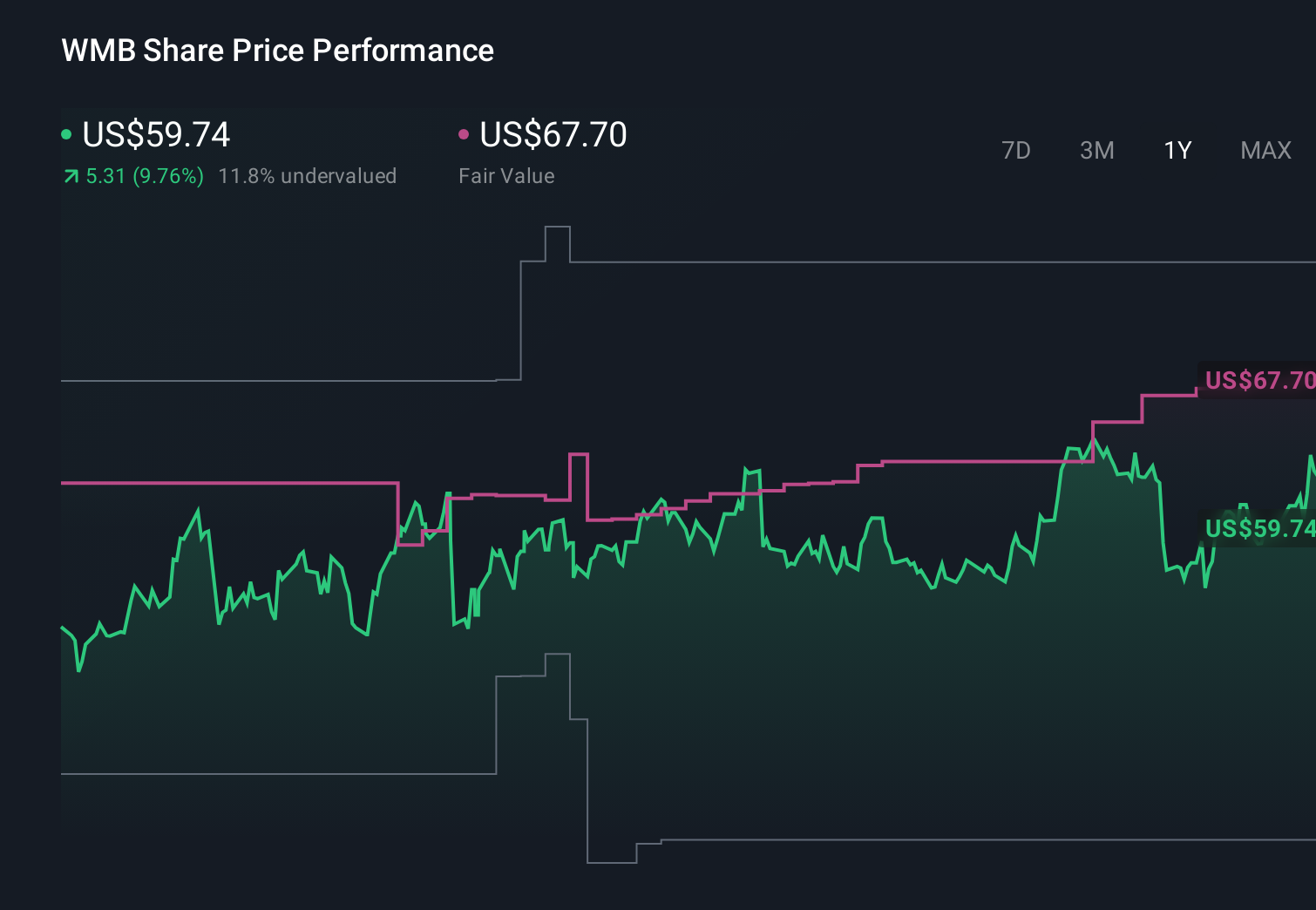

- In the past week, Williams Companies reported first-quarter 2026 results that exceeded expectations, reaffirmed its 2026 adjusted EBITDA outlook, and raised its annualized dividend by 5%, supported by stronger volumes, higher rates, and pipeline expansions across key segments, particularly Transmission, Power & Gulf.

- Analyst commentary highlighting continued growth in Williams’ core pipeline network and the resilience of its dividend policy underscores how recent operating gains may be reinforcing perceptions of the company’s cash flow stability.

- With this stronger-than-expected quarter underscoring segment expansion and volume growth, we’ll now examine how these developments affect Williams’ investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Williams Companies Investment Narrative Recap

To own Williams today, you need to believe in the durability of U.S. natural gas infrastructure and the value of its core Transco and Gulf Coast pipelines, even as decarbonization and policy risks build over time. The latest earnings beat and reaffirmed 2026 EBITDA outlook support the near term volume and project ramp story, while the 5% dividend increase highlights income appeal. The biggest near term swing factor still appears to be execution and permitting on major growth projects like NESE; this quarter’s news does not materially change that risk profile.

The most relevant recent announcement here is Williams’ 5% dividend increase to an annualized US$2.10 per share, coming alongside Q1 2026 adjusted EPS growth of 22% and a 13% rise in adjusted EBITDA. In the context of Transmission, Power & Gulf driven gains and ongoing capacity additions tied to LNG and power demand, the higher payout reinforces the idea that management sees current cash flows as supportive of its capital plan and income commitments, even as long term energy transition risks remain.

Yet behind the higher dividend and solid quarter, investors should also be aware of how faster decarbonization or tougher ESG driven financing could eventually pressure Williams’...

Williams Companies’ narrative projects $16.3 billion revenue and $3.9 billion earnings by 2029. This requires 11.3% yearly revenue growth and roughly a $1.3 billion earnings increase from $2.6 billion today.

Uncover how Williams Companies' forecasts yield a $80.07 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already saw a very different upside story here, with revenue potentially reaching about US$18.1 billion and earnings US$4.4 billion by 2029, assuming higher margins and strong data center and LNG pull, which contrasts sharply with the more cautious consensus and may look different again as markets digest this latest earnings surprise.

Explore 5 other fair value estimates on Williams Companies - why the stock might be worth 6% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 32 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.