Why Alignment Healthcare (ALHC) Is Up 10.7% After Beating Revenue Estimates And Rapid Member Growth

Alignment Healthcare, Inc. ALHC | 0.00 |

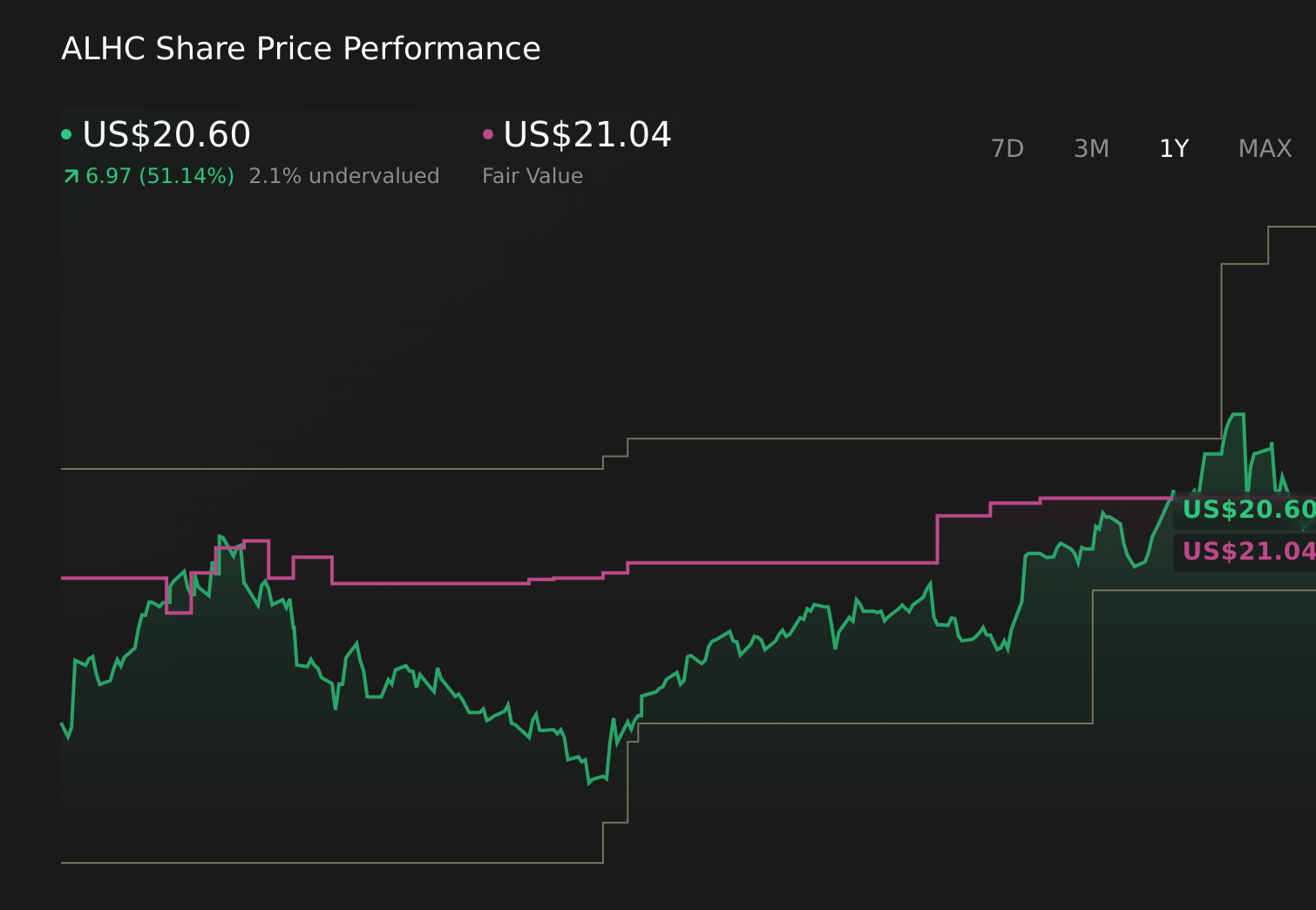

- In the past quarter, Alignment Healthcare reported revenue of US$1.24 billion, a 33.3% year-on-year increase that beat analyst expectations, while adding 48,500 new members to reach 284,800 in total.

- Despite issuing EBITDA guidance for the next quarter that fell short of forecasts, the company’s ability to outpace revenue and EPS estimates highlights operational discipline and momentum in growing its Medicare-focused membership base.

- Against this backdrop of stronger-than-expected revenue and earnings alongside rapid member growth, we’ll explore how these results influence Alignment Healthcare’s investment narrative.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

Alignment Healthcare Investment Narrative Recap

To own Alignment Healthcare, you need to believe its technology-enabled Medicare Advantage model can translate strong member and revenue growth into durable profitability, even as reimbursement rules and medical costs evolve. The latest quarter’s revenue beat and rapid membership gains support that thesis, but softer EBITDA guidance keeps execution risk front and center in the near term, particularly around managing medical costs and margins. Overall, these results affirm the core narrative more than they change the key risks.

Among recent developments, Alignment’s inclusion in multiple S&P indices stands out in this context. Index membership can deepen the shareholder base and support trading liquidity, which may matter if the company needs continued access to capital while it balances growth with margin discipline. Combined with the latest earnings beat and membership expansion, this reinforces the idea that Alignment is moving into a more institutional spotlight just as its execution and regulatory risks are becoming more important to monitor.

Yet beneath the strong revenue and membership headlines, investors should be aware that...

Alignment Healthcare's narrative projects $8.7 billion revenue and $197.2 million earnings by 2029.

Uncover how Alignment Healthcare's forecasts yield a $24.92 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming revenue of about US$8.2 billion and earnings near US$138 million by 2029, so if you lean toward that more cautious view, this quarter’s beats and guidance miss might prompt you to reassess how much weight you give to execution risk versus growth potential.

Explore 2 other fair value estimates on Alignment Healthcare - why the stock might be worth as much as 82% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Alignment Healthcare research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alignment Healthcare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alignment Healthcare's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 41 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.