Why DorianG (LPG) Is Up 7.1% After Bigger Q3 Profit And Cash Returns To Shareholders

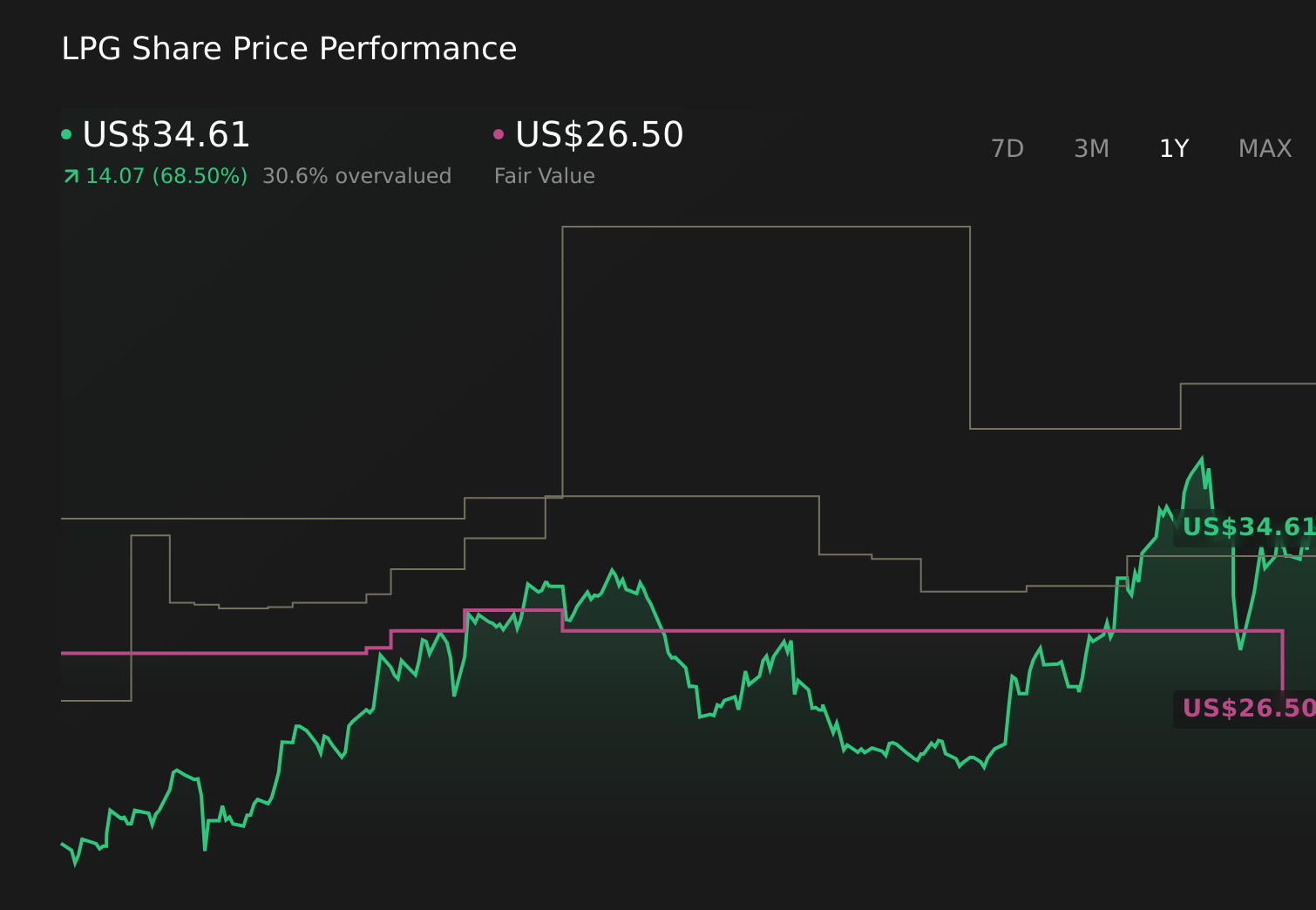

Dorian LPG Ltd. LPG | 34.62 | +2.97% |

- Dorian LPG Ltd. reported past third-quarter 2025 results showing revenue of US$119.96 million and net income of US$47.19 million, alongside completion of a US$9.70 million buyback program and the declaration of an irregular US$0.70 per-share dividend.

- Together, stronger earnings, ongoing share repurchases, and a sizeable irregular dividend highlight the company’s recent emphasis on returning cash to shareholders.

- We’ll now examine how this stronger quarterly profitability and capital return activity may influence DorianG’s existing investment narrative and outlook.

AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

DorianG Investment Narrative Recap

To own DorianG, you need to believe LPG shipping can keep generating solid cash flows despite volatile freight markets, regulatory costs, and shifting energy policies. The latest quarter’s stronger profitability, completion of the US$9.70 million buyback, and irregular dividend support the near term bull case that cash returns can remain attractive, but they do not fully offset key risks like rate volatility and potential oversupply in the VLGC market.

The most relevant recent announcement here is the irregular US$0.70 per share dividend, returning about US$29.9 million. Paired with the completed buyback program, it reinforces DorianG’s existing catalyst of using a strong balance sheet and free cash generation to return capital to shareholders while maintaining flexibility for fleet investment and environmental compliance, even as spot rate and regulatory risks remain in focus.

Yet against these strong cash returns, investors should also weigh the risk that prolonged spot rate weakness and overcapacity could quickly pressure earnings and dividend sustainability...

DorianG's narrative projects $370.1 million revenue and $90.4 million earnings by 2028. This requires 4.9% yearly revenue growth and about a $41.4 million earnings increase from $49.0 million today.

Uncover how DorianG's forecasts yield a $33.33 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some analysts were far more optimistic, expecting revenue to reach about US$387.3 million and earnings US$65.7 million, so this latest earnings and capital return news could meaningfully shift how you weigh that upbeat view against concerns about heavier regulatory costs and customer concentration risk.

Explore 2 other fair value estimates on DorianG - why the stock might be worth just $33.33!

Build Your Own DorianG Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your DorianG research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free DorianG research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DorianG's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find 55 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.