Why FTAI Aviation (FTAI) Is Up 14.8% After Redeeming Costly Preferreds And Securitizing Engines

FTAI Aviation Ltd. FTAI | 0.00 |

- Recently, FTAI Aviation moved to redeem all of its high-yield 8.25% Series C preferred shares, completed a large US$612 million asset-backed securitization, and advanced its plan to convert jet engine cores into power sources for AI data centers.

- An unusual angle for investors is how the Iran peace deal may extend the service life of FTAI’s leased engines while also supporting economics for its emerging AI power turbine business.

- We’ll now explore how redeeming these high-cost preferred shares could reshape FTAI Aviation’s investment narrative and future capital allocation.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

FTAI Aviation Investment Narrative Recap

To own FTAI Aviation, you need to believe that demand for mid‑life engines, MRE programs and parts will stay robust enough to support its leveraged, vertically integrated model. The preferred share redemption and US$612 million securitization strengthen the balance sheet, which helps the near term catalyst of scaling engine programs and AI power turbines, but they do not remove key risks around engine concentration, supply chain execution and signs of insider caution at current valuation.

The move to redeem all 8.25% Series C preferred shares looks especially relevant here, because it reduces expensive dividend obligations and simplifies the capital stack just as FTAI leans into new growth areas like AI power turbines and Iran peace deal tailwinds. A lower preferred dividend burden can free more cash for engine leasing, MRE expansion and SCI partnerships, potentially sharpening how investors weigh the upside of these catalysts against concentration and leverage risks.

Yet in contrast, investors should be aware that recent insider selling and heavy reliance on legacy engine platforms could become more important if...

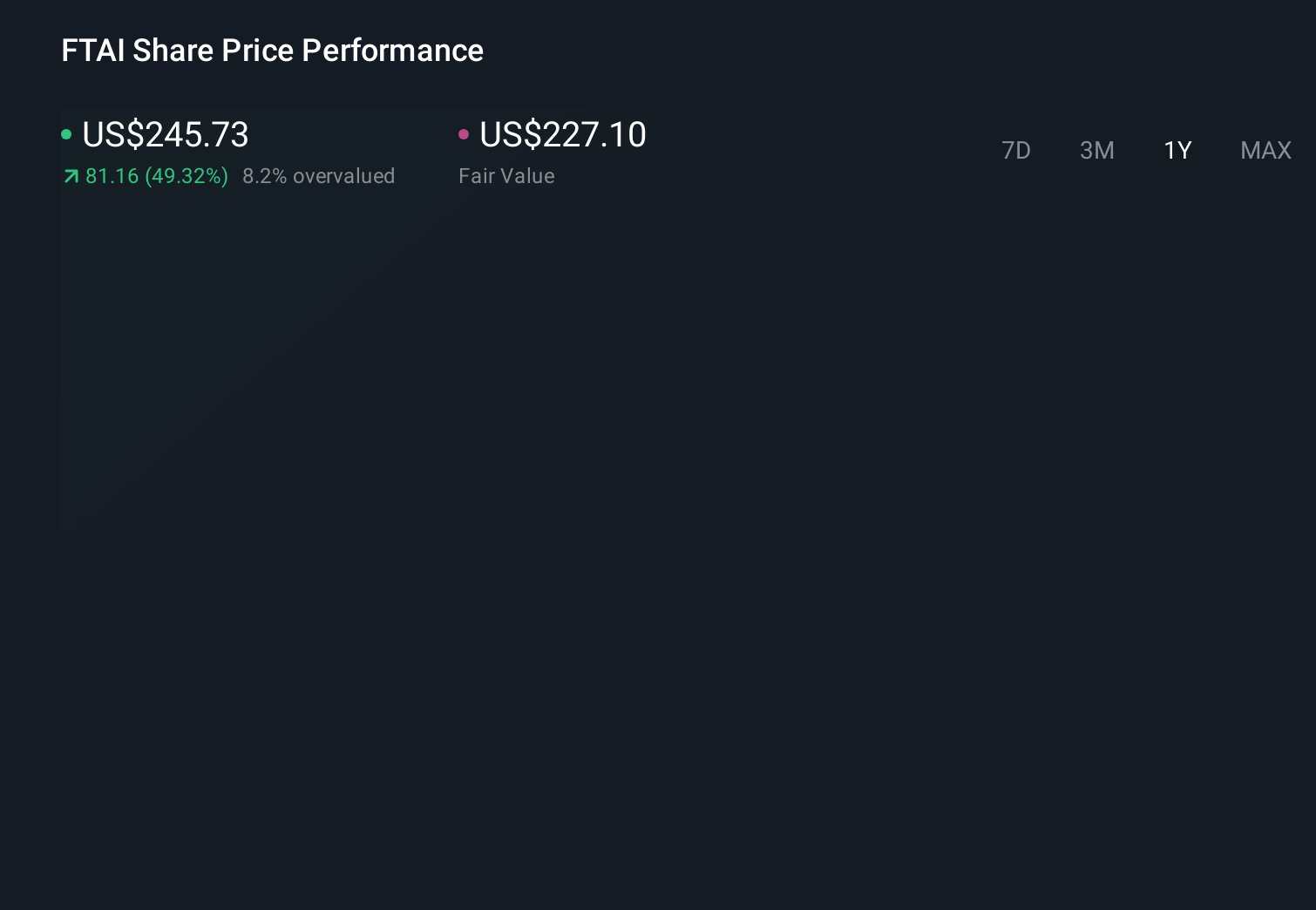

FTAI Aviation's narrative projects $6.6 billion revenue and $1.7 billion earnings by 2029. This requires 32.8% yearly revenue growth and about a $1.2 billion earnings increase from $521.7 million today.

Uncover how FTAI Aviation's forecasts yield a $350.60 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming FTAI could lift revenue to about US$8.8 billion and earnings to roughly US$2.5 billion by 2029, yet this bullish view sits alongside concerns that OEMs could squeeze aftermarket margins. With the latest capital structure moves and AI power ambitions now in play, you can expect those optimistic and cautious narratives to evolve, which is why it is worth comparing how differently people can read the same stock.

Explore 4 other fair value estimates on FTAI Aviation - why the stock might be worth just $299.10!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FTAI Aviation research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free FTAI Aviation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FTAI Aviation's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.