Why Investors Shouldn't Be Surprised By Omnicell, Inc.'s (NASDAQ:OMCL) 26% Share Price Plunge

Omnicell, Inc. OMCL | 34.15 | +0.62% |

The Omnicell, Inc. (NASDAQ:OMCL) share price has softened a substantial 26% over the previous 30 days, handing back much of the gains the stock has made lately. Longer-term shareholders would now have taken a real hit with the stock declining 6.6% in the last year.

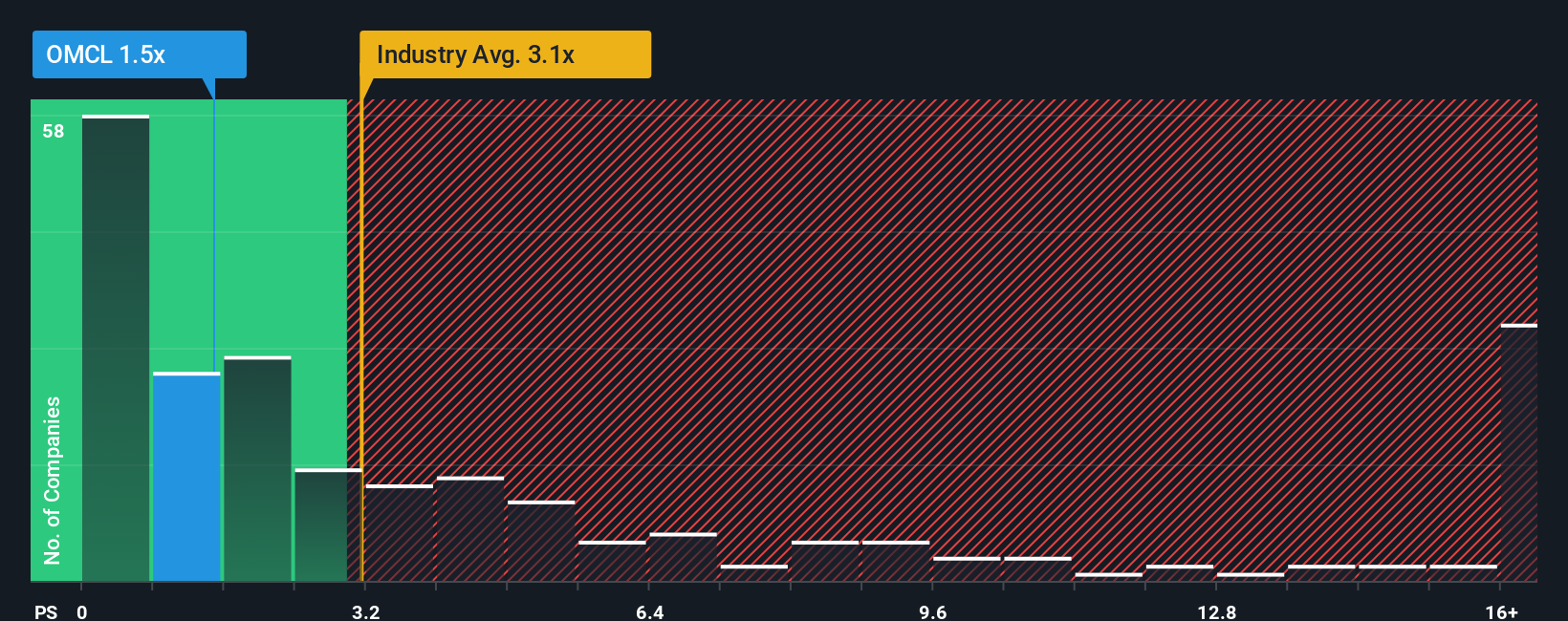

Although its price has dipped substantially, Omnicell may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 1.4x, considering almost half of all companies in the Medical Equipment industry in the United States have P/S ratios greater than 2.9x and even P/S higher than 9x aren't out of the ordinary. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

What Does Omnicell's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Omnicell has been relatively sluggish. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Omnicell.Do Revenue Forecasts Match The Low P/S Ratio?

Omnicell's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Retrospectively, the last year delivered a decent 6.5% gain to the company's revenues. However, this wasn't enough as the latest three year period has seen an unpleasant 8.6% overall drop in revenue. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 4.8% per annum over the next three years. With the industry predicted to deliver 124% growth per annum, the company is positioned for a weaker revenue result.

With this in consideration, its clear as to why Omnicell's P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What Does Omnicell's P/S Mean For Investors?

The southerly movements of Omnicell's shares means its P/S is now sitting at a pretty low level. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Omnicell's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. The company will need a change of fortune to justify the P/S rising higher in the future.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.