Why Mirum Pharmaceuticals (MIRM) Is Up 12.6% After Positive Phase 2b Volixibat Itch Data in PSC

Mirum Pharmaceuticals MIRM | 0.00 |

- Mirum Pharmaceuticals recently reported that its Phase 2b VISTAS trial of volixibat in primary sclerosing cholangitis met the primary endpoint, showing a statistically significant reduction in cholestatic pruritus versus placebo and a safety profile consistent with IBAT inhibition.

- The company is now preparing for a pre-New Drug Application meeting with the FDA in summer 2026 and aims to file an NDA in the second half of 2026, positioning volixibat as a potential first approved therapy for cholestatic itch in this rare liver disease.

- We’ll now examine how volixibat’s positive Phase 2b itch data in PSC may reshape Mirum’s investment narrative and future growth profile.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Mirum Pharmaceuticals Investment Narrative Recap

To own Mirum Pharmaceuticals, you need to believe its rare disease franchise can broaden beyond Livmarli into multiple bile-acid and liver indications, and that regulators will ultimately support these therapies. The positive VISTAS Phase 2b data for volixibat in PSC strengthens that multi-asset story and adds another potential near term filing, but the biggest near term swing factor still looks to be execution and regulatory risk across a growing, capital-intensive pipeline.

The most relevant recent announcement alongside VISTAS is the Phase 2b AZURE-1 readout for brelovitug in hepatitis delta virus, which also hit its primary endpoint with strong antiviral data. Together, brelovitug and volixibat illustrate how Mirum is trying to build a portfolio of late stage liver assets that could complement Livmarli and diversify revenue, while also adding more clinical, regulatory, and pricing risk if any of these programs stumble.

Yet behind this upside, investors should also be aware that Mirum’s heavy R&D spending relative to revenue could quickly become a problem if...

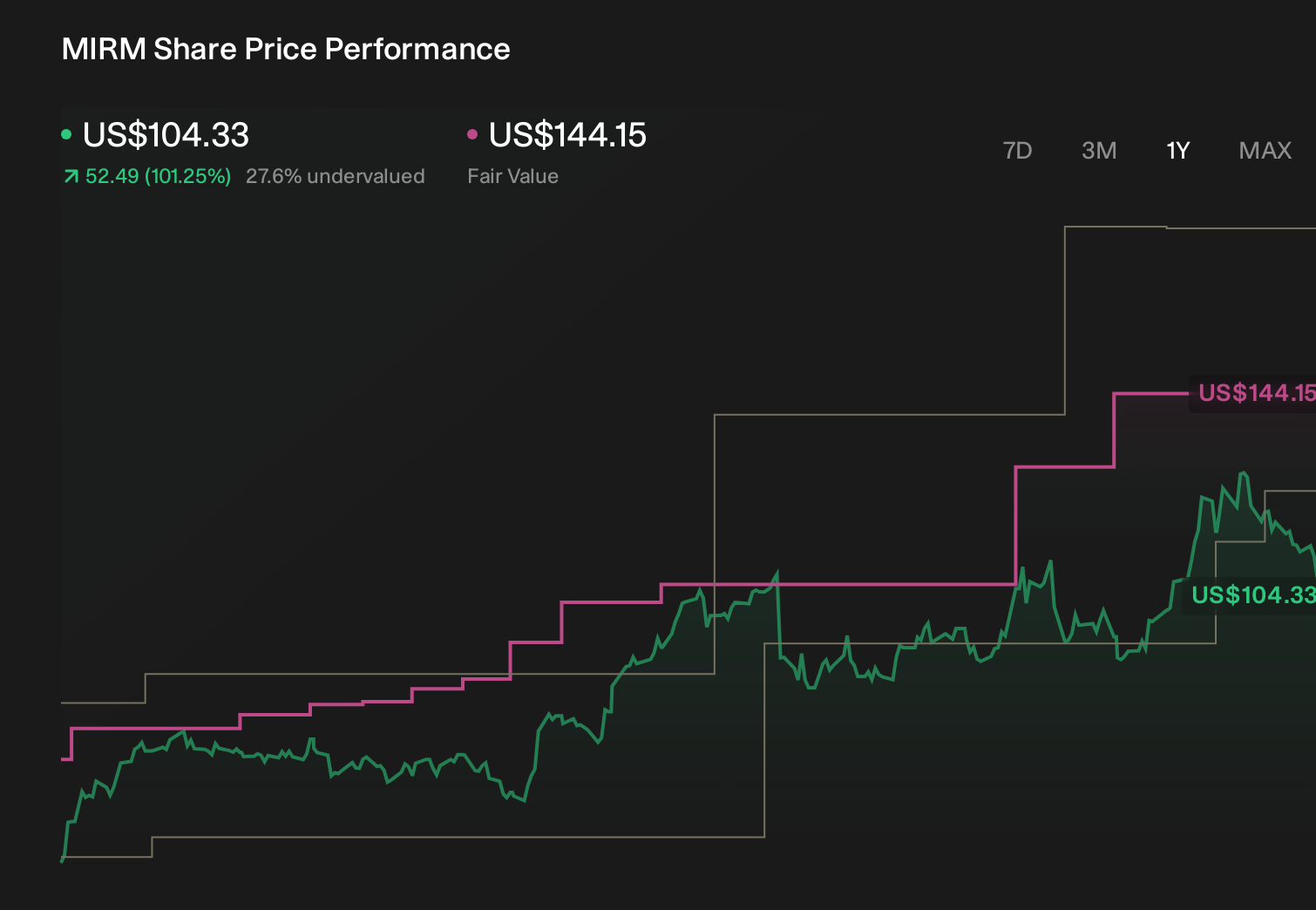

Mirum Pharmaceuticals' narrative projects $978.8 million revenue and $134.8 million earnings by 2029.

Uncover how Mirum Pharmaceuticals' forecasts yield a $129.73 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Before this volixibat news, the most optimistic analysts were already assuming Mirum could reach about US$1.2 billion of revenue and US$339 million of earnings by 2029, so if you buy into that faster patient and pricing expansion story you are accepting a far more optimistic view of trial success and market adoption than the baseline narrative, and this new PSC data may either reinforce or challenge those expectations once forecasts are updated.

Explore 3 other fair value estimates on Mirum Pharmaceuticals - why the stock might be worth 10% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Mirum Pharmaceuticals research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Mirum Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mirum Pharmaceuticals' overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.