Why Polaris (PII) Is Up 5.2% After Mixed Earnings And Expanded Youth ATV Safety Push

Polaris Inc. PII | 0.00 |

- Polaris Inc., in partnership with Minnesota 4-H, recently expanded its youth ATV safety efforts by launching the interactive ATV Adventure Academy: Trailblazers experience on 4-H’s CLOVER online platform, extending foundational safe-riding education to a broad audience beyond its existing programs that have already reached more than 800,000 youth.

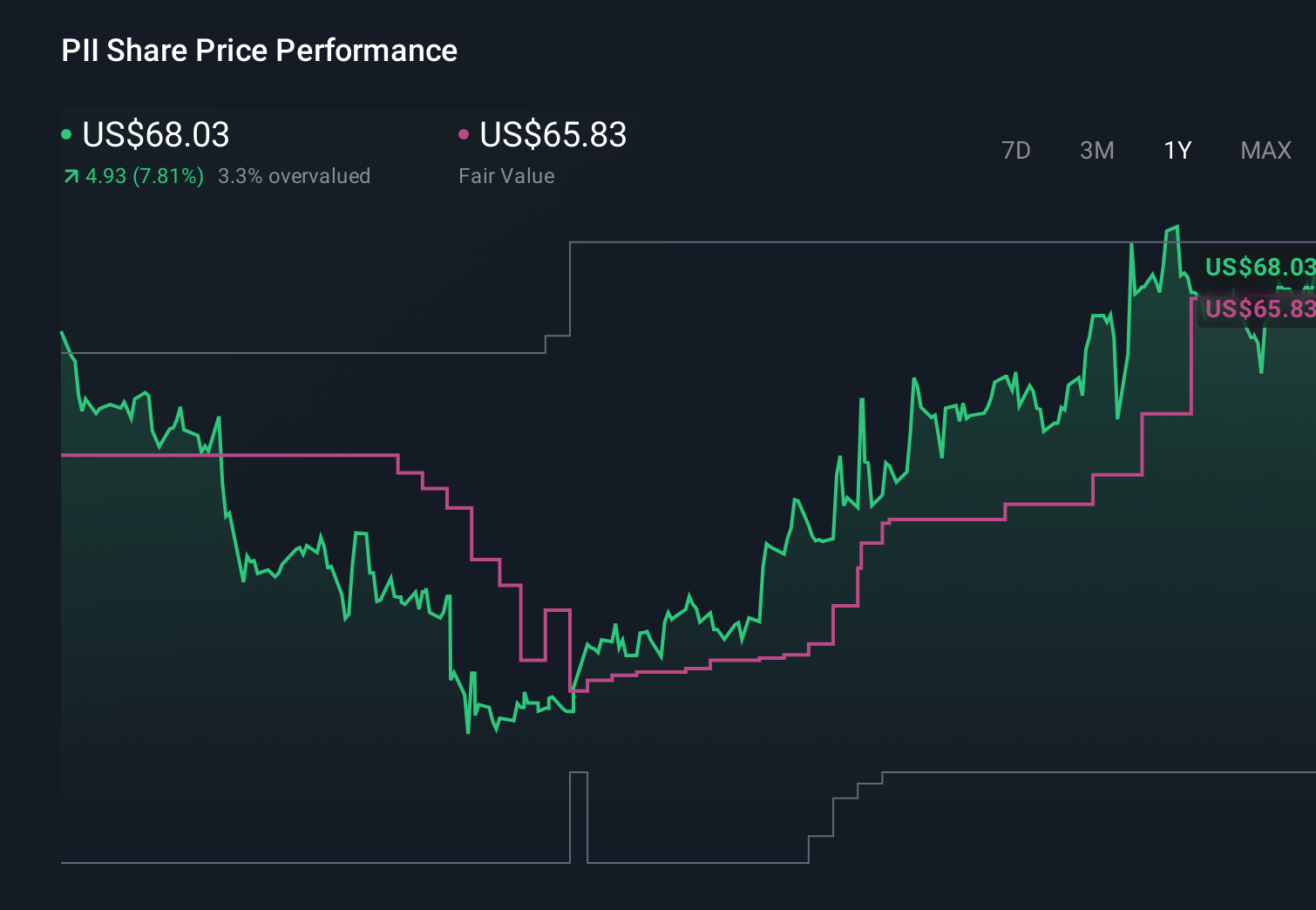

- This move reinforces Polaris’ emphasis on responsible riding and long-term brand building in off-road vehicles, even as its latest quarterly results showed revenues of US$1.94 billion, up year on year and ahead of analyst expectations, alongside full-year EPS guidance that did not meet consensus estimates.

- We’ll now explore how Polaris’ stronger-than-expected quarterly results but softer full-year EPS guidance affect its investment narrative and risk profile.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Polaris Investment Narrative Recap

To own Polaris today, you need to believe it can convert its strong brands, broad powersports lineup and cost-control efforts into a sustained return to profitability, despite recent losses and tariff and demand pressures. The latest quarter’s revenue beat to US$1.94 billion supports the near term case that Polaris can still grow sales, but the softer full year EPS guidance keeps margin recovery and earnings timing as the key catalyst and risk. This youth safety partnership is directionally positive for brand strength, but not a material driver of those financial swing factors.

The ATV Adventure Academy launch with Minnesota 4 H fits with Polaris’ broader push to reinforce responsible riding and long term customer relationships, especially among younger riders. Set against ongoing product refreshes such as the new RANGER and RZR Pro R models, it adds another piece to the longer term demand story, even as the more immediate catalysts for the stock remain execution on tariff mitigation, cost control and stabilizing retail demand.

Yet underneath the upbeat safety and brand story, one risk investors should be aware of is that...

Polaris' narrative projects $7.8 billion revenue and $425.0 million earnings by 2029.

Uncover how Polaris' forecasts yield a $68.00 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts see tariff relief and execution turning today’s loss into about US$411.4 million of earnings by 2029, which is a far more bullish story than the cautious consensus and could look different again once this latest Polaris news is fully reflected in forecasts.

Explore 3 other fair value estimates on Polaris - why the stock might be worth 30% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.