Why Walker & Dunlop (WD) Is Up 8.9% After Strong Q1 2026 Results And Dividend Affirmation

Walker & Dunlop, Inc. WD | 0.00 |

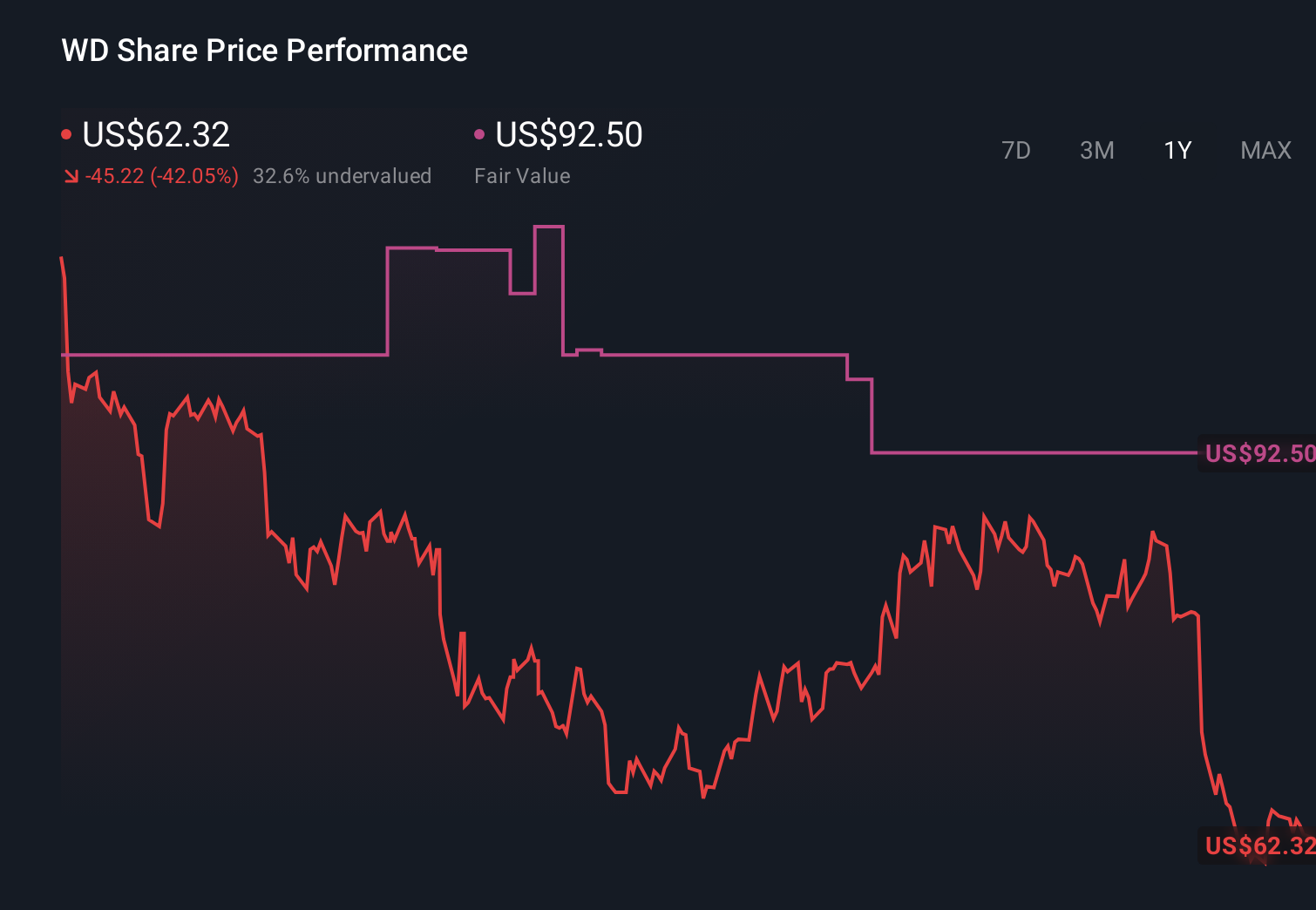

- Walker & Dunlop, Inc. has reported past first-quarter 2026 results, with revenue rising to US$301.33 million and net income to US$15.87 million, alongside affirming a quarterly dividend of US$0.68 per share payable on June 4, 2026.

- Beneath these headline figures, the company highlighted very large growth in transaction volumes and agency lending, supported by complex refinancing deals and higher productivity per banker that helped increase its share of the GSE lending market.

- We’ll now examine how Walker & Dunlop’s stronger first-quarter profitability and agency lending growth may influence its existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you need to believe in its role as a capital provider and adviser across commercial real estate cycles, with agency lending as a key pillar. The strong first quarter rebound in revenue and earnings supports the near term catalyst of higher refinancing and GSE-driven volumes, but it does not remove the biggest risk that volumes and margins could still be constrained if high interest rates and fee pressure persist.

The most relevant recent announcement is the first quarter 2026 earnings release, which showed revenue increasing to US$301.33 million and net income to US$15.87 million, helped by a 94% jump in transaction volume and 109% growth in agency lending. That mix, including complex workforce housing refinancings, ties directly to the short term catalyst of gaining share in GSE lending while highlighting the ongoing risk that larger, lower fee transactions can weaken overall margin expansion even when activity is strong.

Yet investors should be aware that reliance on GSE volumes and fee margins may become a bigger issue if...

Walker & Dunlop's narrative projects $1.6 billion revenue and $203.8 million earnings by 2029. This requires 12.3% yearly revenue growth and a $148.1 million earnings increase from $55.7 million today.

Uncover how Walker & Dunlop's forecasts yield a $68.00 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently see fair value for Walker & Dunlop between US$30.99 and US$68, showing a wide spread of views. When you set those opinions against the company’s reliance on GSE lending caps and fee margins, it underlines how critical it is to weigh several viewpoints before deciding how this business might perform through future credit cycles.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth 43% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.