Will ArcBest's (ARCB) Texas Incorporation Amid Earnings Pressure Change Its Governance and Risk Narrative?

ArcBest Corporation ARCB | 0.00 |

- ArcBest recently gained shareholder approval to move its legal incorporation from Delaware to Texas, a change that will not alter its headquarters, operations, management, or workforce.

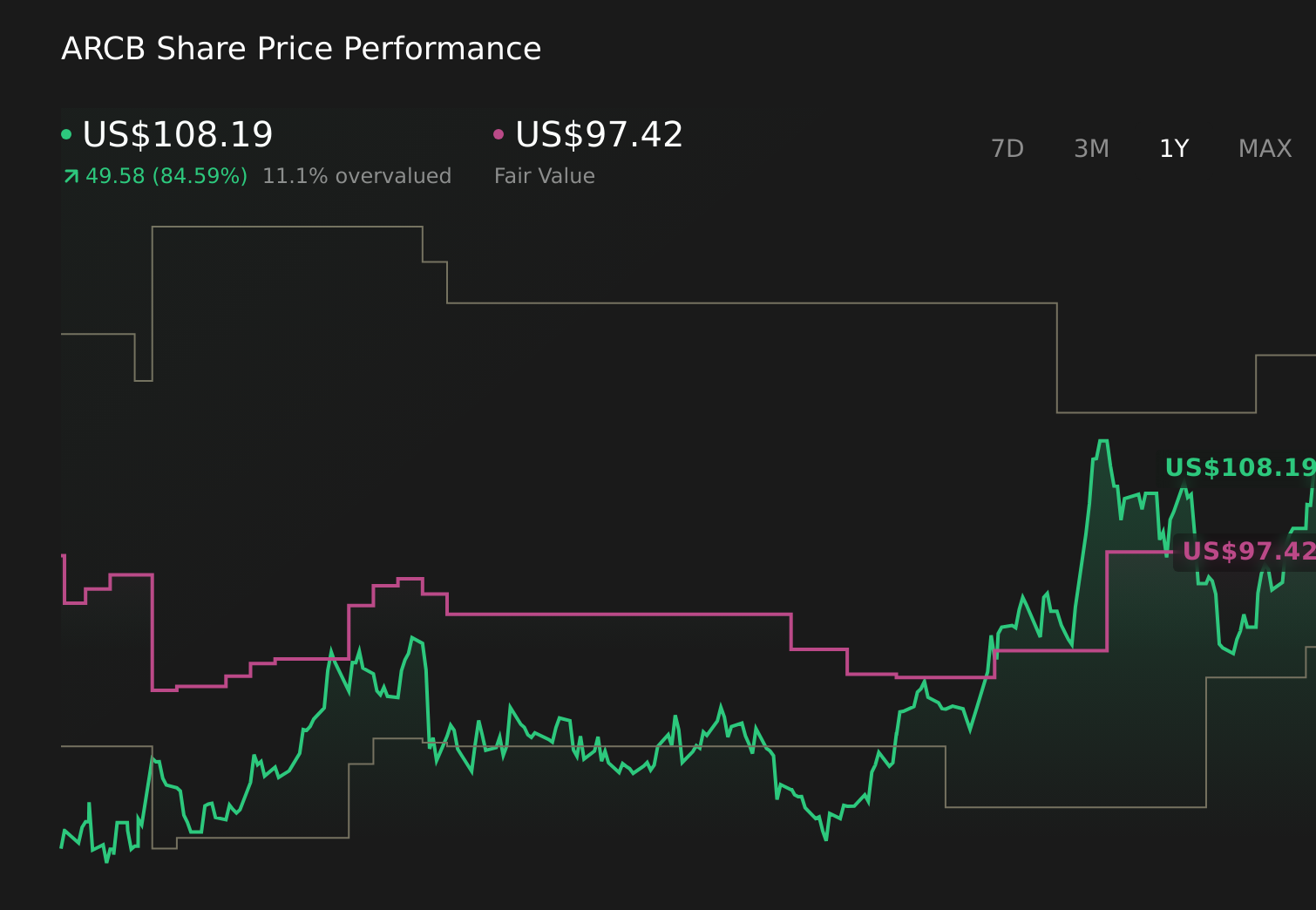

- This shift toward Texas law, which the board views as offering clearer and more predictable protections for directors and officers, comes as the company faces underwhelming unit sales, declining profitability, and a forward P/E ratio of 21.2x.

- Next, we’ll examine how ArcBest’s move to Texas incorporation, amid pressure on earnings and returns, could reshape its investment narrative.

Find 50 companies with promising cash flow potential yet trading below their fair value.

ArcBest Investment Narrative Recap

To own ArcBest, you need to believe its freight network and technology investments can overcome a soft freight cycle, margin pressure, and low returns on equity. The move from Delaware to Texas incorporation mainly affects legal protections for leadership and does not materially shift the near term earnings catalyst or the key risk of continued pricing and volume pressure in a competitive, capacity heavy market.

The most relevant recent announcement alongside the Texas move is ArcBest’s continued buybacks, with roughly 29.5% of shares repurchased since 2003 even as earnings weakened and Q1 2026 slipped to a small net loss. For me, that combination of ongoing capital returns and legal realignment frames how management is positioning the company’s equity story against a backdrop of soft profitability and a forward P/E of 21.2x.

Yet against these legal and capital allocation moves, investors should also be aware of the longer term threat from e-commerce players building their own logistics networks…

ArcBest's narrative projects $4.5 billion revenue and $147.2 million earnings by 2028. This requires 3.9% yearly revenue growth and a $11.1 million earnings decrease from $158.3 million today.

Uncover how ArcBest's forecasts yield a $97.42 fair value, a 21% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming ArcBest could lift earnings to about US$213.7 million by 2029, yet this new Texas incorporation decision and the risk of e-commerce giants bypassing third party carriers underline how much those upbeat expectations might need revisiting, so you should weigh these very different outlooks for yourself.

Explore 3 other fair value estimates on ArcBest - why the stock might be worth 40% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ArcBest research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ArcBest research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ArcBest's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.