Will Digital Realty’s 2025 Partner of the Year Nod Reshape ePlus' (PLUS) AI-Enabler Narrative

ePlus inc. PLUS | 0.00 |

- ePlus Inc. was recently named Digital Realty’s Americas Partner of the Year for 2025, recognizing its role in advancing customers’ digital transformation and AI initiatives, including its AI Experience Center inside Digital Realty’s Innovation Lab in Ashburn, Virginia.

- This recognition highlights ePlus’s growing influence in AI-focused infrastructure and services, potentially reinforcing its positioning as an enabler of enterprise AI adoption.

- We’ll now examine how this Partner of the Year award, especially the AI Experience Center collaboration, may influence ePlus’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

ePlus Investment Narrative Recap

To own ePlus, you need to believe it can keep deepening its role as an AI and cloud infrastructure partner while managing margin and revenue volatility from large, project-based deals. The Digital Realty Americas Partner of the Year award, tied to its AI Experience Center, supports the AI adoption angle but does not materially change the near term risk that lumpy enterprise projects and mix-shift pressure could still weigh on profitability.

Among recent announcements, the launch of ePlus’s Private AI Infrastructure as a Service with Digital Realty and Lenovo feels most connected to this Partner of the Year recognition, since both spotlight ePlus as the “plumbing” provider behind enterprise AI. Together, they feed into the core catalyst of growing managed and recurring AI infrastructure services, which could gradually offset dependence on one-off, lower margin hardware heavy projects.

Yet behind the AI momentum, investors should be aware of how concentrated customer spending and project specific deals could...

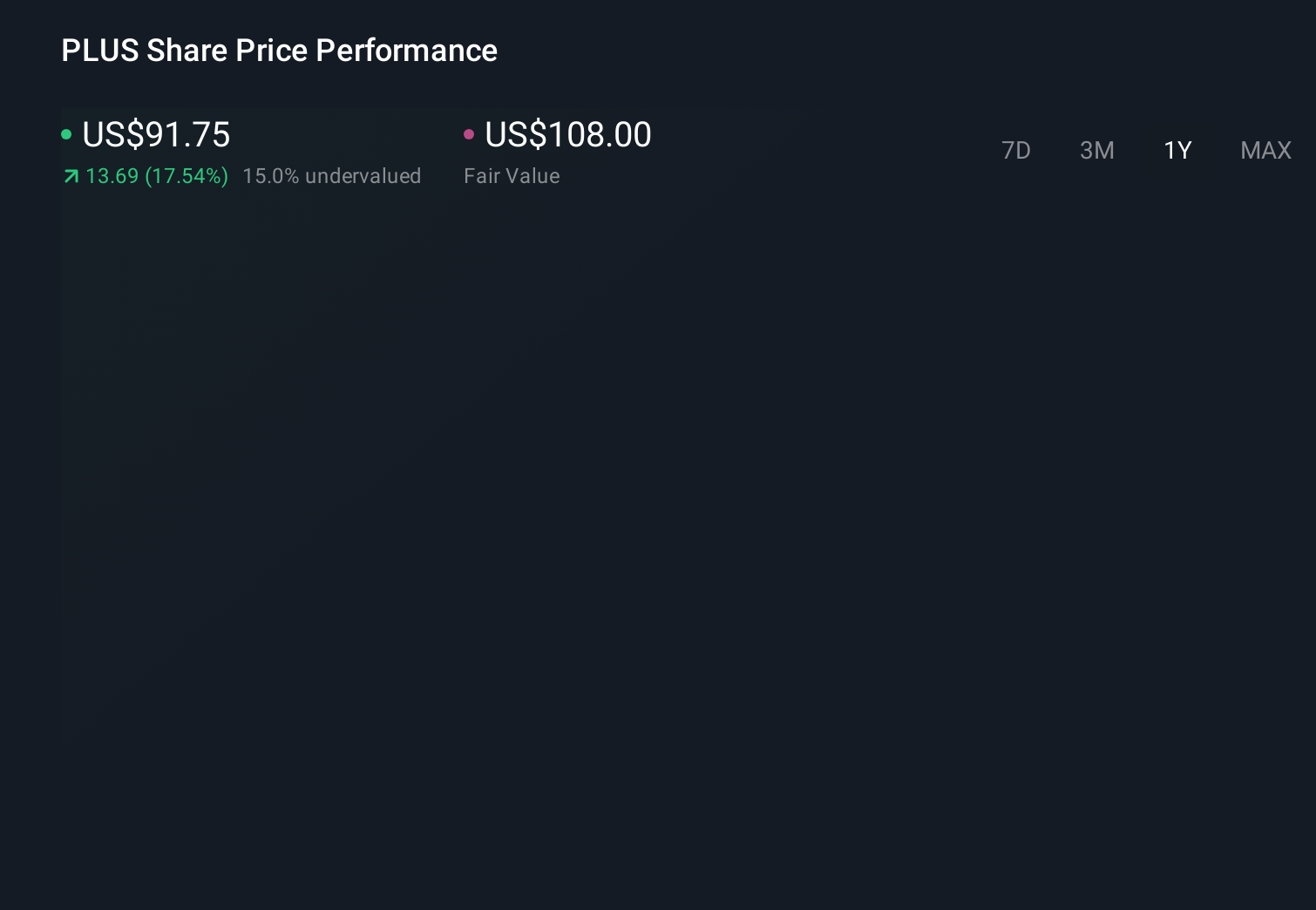

ePlus' narrative projects $2.8 billion revenue and $136.4 million earnings by 2029. This requires 5.0% yearly revenue growth and about a $12.3 million earnings increase from $124.1 million today.

Uncover how ePlus' forecasts yield a $111.00 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span from US$66.98 to US$111, underscoring how differently individual investors are viewing ePlus. Against that spread, the key question is whether AI related infrastructure demand and expanding managed services can meaningfully smooth the revenue lumpiness that still hangs over the story.

Explore 2 other fair value estimates on ePlus - why the stock might be worth 18% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ePlus research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

No Opportunity In ePlus?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.