Will Leadership Succession and Special Dividends Change W. R. Berkley's (WRB) Capital Allocation Narrative?

W. R. Berkley Corporation WRB | 0.00 |

- W. R. Berkley Corporation recently extended the maturity of its revolving credit facility to June 9, 2031, increased its regular quarterly dividend to US$0.10 per share, declared a US$0.50 special dividend, and announced governance changes following the passing of founder and Executive Chairman William R. Berkley.

- The combination of a leadership transition to W. Robert Berkley, Jr. as Chairman and substantial capital returns highlights how the company is pairing succession continuity with a shareholder-focused balance sheet.

- We will now examine how the leadership transition to W. Robert Berkley, Jr. and enhanced capital returns affect W. R. Berkley’s investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

W. R. Berkley Investment Narrative Recap

To own W. R. Berkley, you need to be comfortable with a specialty commercial insurer whose story centers on disciplined underwriting, steady capital returns, and a largely U.S.-focused footprint. In the near term, the key catalyst is how effectively the company sustains underwriting quality and pricing discipline in competitive property and short tail lines, while the biggest risk remains margin pressure from rising loss costs and more aggressive rivals. The recent leadership change and capital actions do not materially alter these core drivers.

Among the latest announcements, the extension of W. R. Berkley’s revolving credit facility maturity to June 9, 2031 stands out in this context. A longer-dated facility can support flexibility around claims volatility, catastrophe events, and potential investment in higher-margin specialty opportunities. For investors watching near term underwriting catalysts and competitive risks, this added liquidity backstop sits alongside dividends and buybacks as part of the broader capital framework shaping the stock’s risk reward profile.

Yet despite this support, investors should be aware that growing competition and erosion of underwriting discipline could still...

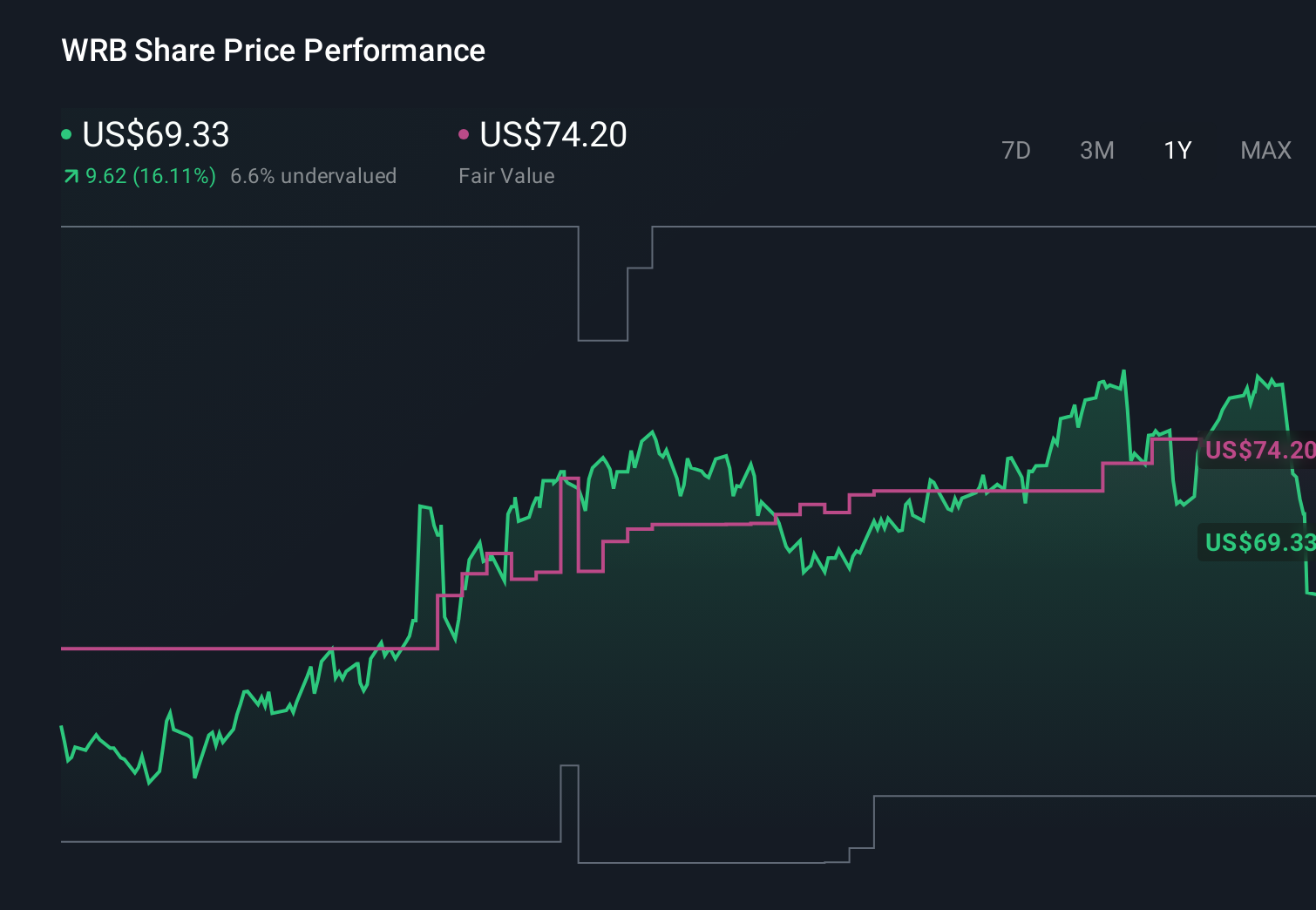

W. R. Berkley's narrative projects $14.3 billion revenue and $2.0 billion earnings by 2028. This requires a 0.0% yearly revenue decline and a $0.2 billion earnings increase from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $68.33 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming revenue would shrink about 2.3 percent a year and earnings stay around US$1.9 billion, so you should recognize that this news could either soften or reinforce that more pessimistic view depending on how you weigh the added balance sheet flexibility against those competitive and catastrophe risks.

Explore 3 other fair value estimates on W. R. Berkley - why the stock might be worth as much as 81% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.